Promotion: Capital invested is at risk. Non-Independent Research / Marketing Communication. Attention is drawn to the disclaimers and risk warnings within this document.

Report written Clear Capital research

Clear Capital Markets Corporate Broking acts as Corporate Broker to Georgina Energy Plc

Capital Invested is at Risk. Non-Independent Research / Marketing Communication. Attention is drawn to the disclaimers and risk warnings at the end of this document

A re-entry–led helium and hydrogen portfolio approaching a lower-risk commercial inflection point

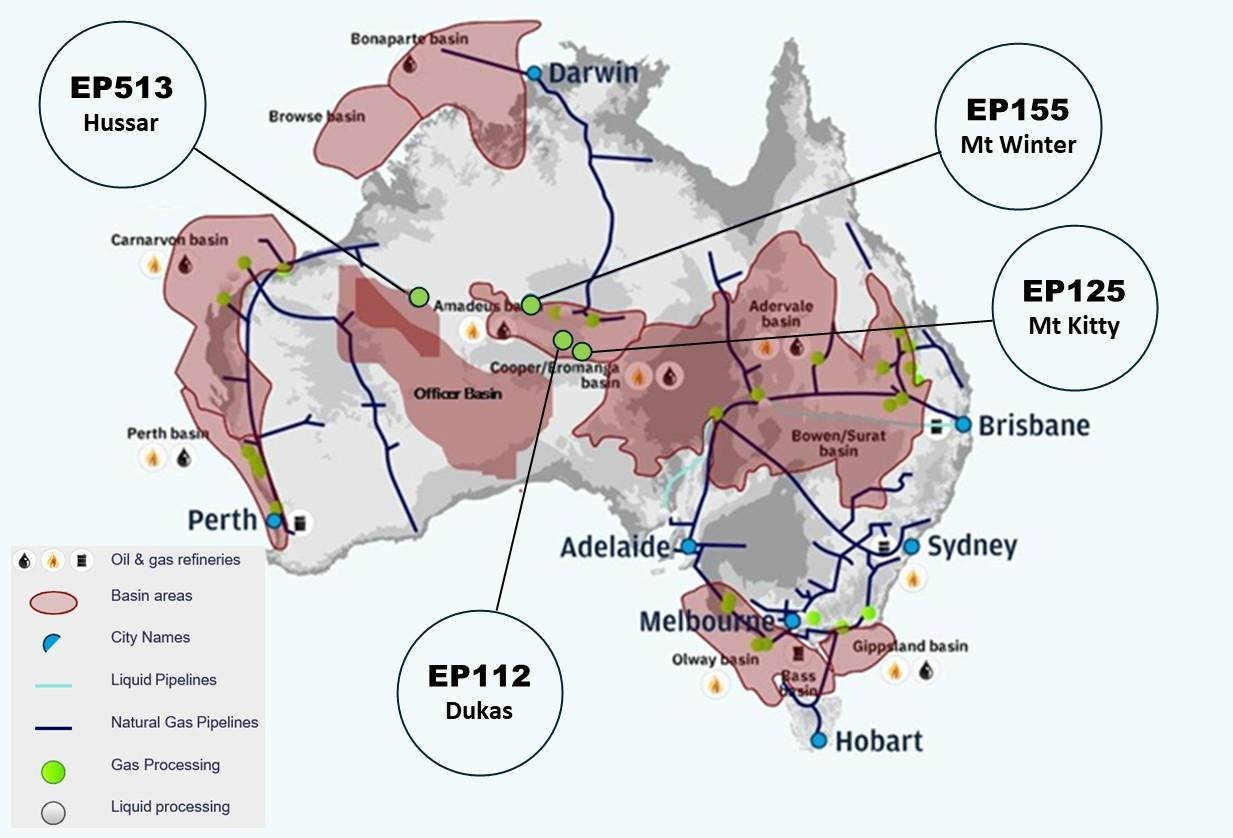

Georgina Energy plc is a UK-listed helium and hydrogen-focused energy company with a portfolio of onshore Australian assets targeting subsurface accumulations of helium, hydrogen and associated natural gas. Following the recent acquisition of interests in the Mt Kitty and Dukas projects, the Company has materially reshaped both the scale and risk profile of its asset base, transitioning from frontier exploration toward a re-entry and appraisal-led strategy. Near-term value is anchored by the Mt Kitty re-entry programme, with larger-scale upside at Dukas, which at over 1,000 km2/247,000 acres is probably the largest untested subsalt prospect in Australia, with Mt Winter and Hussar providing medium to longer-dated optionality. The Mt Winter project is in the same basin and targeting the same play (i.e. subsalt sandstones and fractured basement) as the Mt Kitty 1 and Magee 1 wells which successfully flowed gas to surface with phenomenally high levels of helium (up to 9%) and hydrogen (up to 11.5%) in the gas mix as well as up to 40% hydrocarbons.

This shift is central to the investment case. Unlike greenfield exploration, where the primary uncertainty is whether a working subsurface system exists at all, re-entry projects are built around previously drilled wells that have already demonstrated gas flows to surface. Across Georgina’s core assets, historical drilling has confirmed the presence of mobile gas, anomalously high helium concentrations relative to global norms, associated hydrogen and natural gas, and effective geological sealing.

As a result, future activity is less focused on binary discovery risk and increasingly centred on engineering execution, well design, lateral exposure, completion techniques and flow optimisation. In our view, this transition materially lowers overall project risk and represents an important inflection point in the Company’s evolution.

Key takeaway: The portfolio has transitioned from frontier exploration toward re-entry and appraisal, marking a clear step-change in maturity and risk profile.

Hussar funding breakthrough

In a significant milestone, Georgina announced on 28 January 2026 that Harlequin Energy Ltd has committed to funding the drilling of the Hussar-2 well through a structured US$25 million offtake funding facility. This facility is non-dilutive for Georgina shareholders and will cover the complete drilling programme and site infrastructure works required to test the Hussar prospect within EP513.

This transaction marks an important inflection point for the portfolio, as it de-risks a major drilling campaign without immediate shareholder dilution and validates the commercial attractiveness of Georgina's Officer Basin position. The funding structure contemplates offtake arrangements for helium, hydrogen and natural gas recovered from the Hussar-2 well, aligning GEX and Harlequin interests around successful exploration and appraisal outcomes.

Alongside the funding confirmation, Georgina reported updated prospective resource estimates by an independent Competent Person for Hussar (at 300 km2/74,000 acres one of the largest un-tested prospects in Australia at the targeted subsalt horizons) based on continued technical work and analogue calibration. The revised 2U (P50) estimates show a material upgrade across all gas species:

These revised figures, combined with secured non-dilutive drilling funding, position Hussar alongside Mt Kitty as a near-term value catalyst, albeit with different risk profiles: Mt Kitty offers lower geological risk via re-entry of a gas-proven well, while Hussar provides larger scale upside backed by third-party capital validation.

From geological uncertainty to engineering execution

Early-stage helium explorers are typically exposed to highly binary outcomes: either a helium-bearing system is present, or it is not. Georgina’s portfolio increasingly sits well beyond this phase. At assets such as Mt Kitty and Dukas, gas has already been flowed to surface, albeit from vertical wells that intersected only limited portions of the targeted reservoir or fractured basement.

The Company’s development concept is therefore focused on enhancing reservoir contact, for example through planned horizontal re-entry wells designed to intersect naturally-fractured systems more effectively. This fundamentally changes the risk profile of the projects. The key questions become how much gas can be produced and at what flow rate, rather than whether gas exists at all.

While execution risk remains real, it is typically more quantifiable, more manageable and less binary than frontier geological risk. We believe this distinction is under-appreciated by the market and not yet fully reflected in the Company’s valuation.

Key takeaway: With gas already flowed to surface at multiple assets, the dominant risk has shifted from geological discovery to engineering execution.

Operating landscape: de-risked subsurface, practical execution environment

Georgina’s core assets are located onshore within Australia’s Amadeus and Officer Basins, regions with a long history of subsurface gas shows and some of the highest recorded helium concentrations globally. Historical wells have demonstrated mobile gas systems with elevated helium and hydrogen content, supporting the technical basis for re-entry and appraisal-led development.

This subsurface potential is complemented by a practical operating environment. Assets benefit from established road access, proximity to regional service centres and legacy oil & gas infrastructure, and year-round accessibility using conventional drilling and completion equipment. These factors reduce logistical complexity, support cost control and allow iterative well design; a key advantage where execution, rather than discovery, is the primary risk.

From a fiscal perspective, Australia offers a stable and transparent petroleum regime, with standard corporate taxation and well-established onshore royalty frameworks. While government take is not unusually low by global standards, the absence of sudden fiscal shifts and the clarity of obligations ahead of production are generally viewed as supportive for project planning and investment, particularly relative to higher-risk jurisdictions.

Key takeaway: Georgina operates in a setting where geological upside is matched by logistical and fiscal predictability; increasing the likelihood that technical success translates into commercial outcomes.

Commercialisation and offtake pathways: multiple routes to monetisation

Beyond technical execution, Georgina has begun to establish credible commercial pathways that materially de-risk development and accelerate the transition from appraisal to revenue.

A key element is the extended non-exclusive Memorandum of Understanding with Halo Capital Investments Ltd, now running to August 2028 and explicitly expanded to include the recently acquired Central Petroleum assets. The MoU provides a framework under which Halo may secure offtake for helium, hydrogen and natural gas, while also assuming responsibility at its own cost for processing, separation, storage, transportation and export logistics, subject to final contract and proof of funds.

Importantly, the framework contemplates wellhead gas sales and the potential for pre-payment or development funding linked to offtake volumes, which could significantly reduce Georgina’s upfront capital requirements and shorten development timelines. This structure aligns with industry norms in industrial gas markets, where long-term bilateral contracts underpin project economics rather than spot pricing.

In parallel, the acquired re-entry assets sit within joint operating agreements involving Santos QNT Pty Ltd, a major regional operator with established infrastructure and execution capability. While Santos is not an offtake counterparty at this stage, its involvement at the asset level introduces additional optionality around operational alignment, infrastructure sharing or future commercial cooperation as projects mature.

Key takeaway: Georgina is not reliant on a single commercial outcome. Instead, it has multiple potential routes to monetisation, spanning offtake-led funding, partner-funded processing and operational alignment, which enhances flexibility and reduces capital risk.

We believe Georgina is at an attractive entry point because multiple strands of de-risking are now converging. The portfolio has moved beyond frontier exploration toward re-entry and appraisal, materially reducing geological uncertainty. Execution risk is increasingly defined by engineering and delivery rather than discovery.

At the same time, assets are located within a supportive operating environment, combining practical logistics and fiscal stability with high-value gas systems. This improves the probability that technical success can be converted into commercial outcomes.

Crucially, this technical progress is now being matched by early-stage commercial positioning. The extension of the Halo Capital Investments MoU to include newly acquired assets, together with the involvement of Santos at the asset level, indicates that commercial and strategic considerations are being advanced in parallel with appraisal activity, rather than deferred until late-stage development.

In a helium market characterised by structural supply constraints and limited substitutes, projects that combine proven gas presence, lower-risk execution and emerging offtake pathways are likely to command increasing strategic interest. As a result, we view the period ahead — before appraisal drilling, flow optimisation and potential offtake progression, as a natural valuation inflection point, where incremental milestones can unlock value progressively rather than through a single binary event.

Key takeaway: With technical risk reduced and commercial pathways emerging, Georgina is entering a phase where incremental progress has the potential to drive disproportionate valuation uplift.

Helium and hydrogen: co-products with distinct value drivers

Helium underpins the near and medium-term investment case. It is a critical industrial gas with no substitutes, used in MRI scanners, semiconductor manufacturing, fibre optics and aerospace applications. Demand is price inelastic, supply is structurally constrained, and helium is typically sold under long-term offtake contracts that support cash-flow visibility once in production.

Hydrogen provides co-billing rather than speculative overlay. Recorded subsurface hydrogen flows across multiple wells indicate a working system, and hydrogen may enhance project economics either as a saleable product or through blending with helium and natural gas streams. We view hydrogen as longer-dated upside that strengthens the strategic relevance of the portfolio without dominating the near-term valuation case.

Valuation approach and recommendation

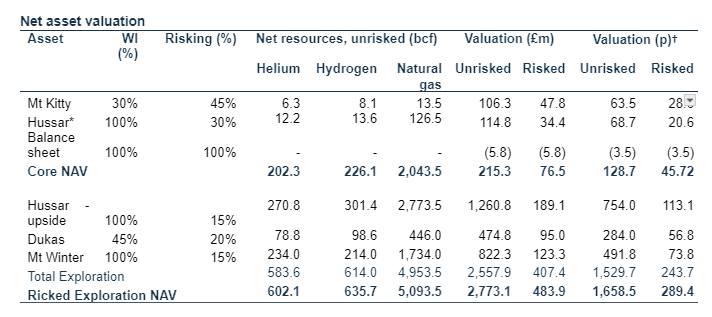

We initiate coverage with a BUY rating and target price of 46p per share (Core NAV: £76.5m risked), representing 5x current levels. This conservative framework deliberately excludes £407m of risked exploration NAV, anchoring value to Mt Kitty (£47.8m; 30% WI in proven 9% helium / 11.5% hydrogen system with near-term re-entry) and Hussar Phase 1 (£34.4m; 100% WI with secured Harlequin drilling funding). Helium pricing is conservatively assumed at $350/mcf - less than half the $700/mcf Hussar scoping study assumption and well below $900/mcf+ spot prices—embedding significant upside without requiring market tightness.

Multiple near-term catalysts support progressive re-rating: Mt Kitty success (Q1-Q2 2026) adds £16-21m through risk de-weighting; Hussar-2 results (H2 2026, funded) add £23m; helium price normalization to $500-700/mcf adds £37-87m with no execution risk. The excluded £407m exploration upside - comprising Hussar resource expansion (£189m risked; c96% of 2U resources remain beyond Phase 1), Dukas (£95m risked; potentially Australia's largest untested subsalt prospect) and Mt Winter (£123m risked) - provides substantial asymmetric upside if near-term drilling validates the subsalt play concept basin-wide. By anchoring the target to Core NAV only, we establish a narrowly defined value base requiring no exploration success beyond funded/demonstrated assets, while preserving over 20x the current share price in additional upside through progressive risk reduction and exploration conversion.

Overview

Georgina Energy plc is an LSE-listed energy company focused on the exploration and development of helium and hydrogen resources in Australia. The Company operates through its wholly owned Australian subsidiary and holds interests in a portfolio of onshore licences across the Amadeus and Officer Basins.

The Company’s strategy has evolved from basin-scale frontier exploration toward a portfolio-led approach, prioritising assets with existing well control, proven gas systems and clearer development pathways. Georgina’s objective is to progress its most advanced assets toward appraisal and potential development, while retaining longer-dated upside across its broader acreage position.

History to date

Georgina Energy plc’s current listed structure was established through a reverse takeover of Mining, Minerals & Metals plc, an LSE-listed investment company, which completed in July 2024. Following completion of the transaction, the enlarged group was renamed Georgina Energy plc and adopted a strategy focused on helium and hydrogen exploration and development in Australia.

Prior to the reverse takeover, the operating business - conducted through its Australian subsidiary Westmarket Oil & Gas Pty Ltd - had built a portfolio of onshore exploration assets across the Amadeus and Officer Basins. Westmarket’s early work focused on reviewing historical drilling data, seismic interpretation and gas flow results from legacy wells, which indicated the presence of mobile gas systems with anomalously high helium concentrations relative to global norms. This technical foundation underpinned the strategic decision to prioritise helium and hydrogen as primary value drivers, rather than conventional natural gas alone.

Following admission to LSE via the reverse takeover, the Company accelerated its transition from frontier exploration toward a portfolio-led, re-entry and appraisal-focused strategy. This included advancing technical studies across the Mt Winter and Hussar assets, commissioning independent resource assessments and pursuing opportunities to add more mature re-entry targets to the portfolio.

This led to the announcement in November 2025 of the conditional acquisition of interests in the Mt Kitty and Dukas projects from Central Petroleum. These assets bring prior drilling history, independently assessed contingent and prospective resources and a clearer pathway toward appraisal, materially increasing the maturity of the portfolio.

Capital structure

Georgina Energy is listed on the LSE and has historically funded its activities through equity raises and strategic transactions, as is typical for early-stage energy companies. The share register has evolved as the Company has progressed technical work and expanded its asset base.

The announced acquisition of the Central Petroleum assets introduces a strategic industry shareholder, expected to hold a meaningful minority stake following completion. We view this as a positive development, aligning Georgina with an experienced Australian operator and reinforcing the industrial logic of the transaction.

While further funding will be required to progress appraisal and development, management has indicated a preference for staged capital deployment, with potential to mitigate dilution through partnerships, asset-level funding and offtake-linked structures as projects mature.

Board and management

Georgina Energy is led by a board and management team with significant experience across upstream energy, project development and capital markets. The leadership team has overseen the Company’s strategic repositioning toward helium and hydrogen and has been instrumental in sourcing and executing the recent portfolio expansion.

Management’s stated priorities include:

The board provides a balance of technical, commercial and UK plc experience, which we view as particularly important as the Company transitions into a more execution-led phase. Recent activity suggests a growing emphasis on discipline, external validation and portfolio prioritisation, all of which are consistent with the Company’s stated objective of moving toward commercialisation.

Board and Management Biographies

Peter Bradley — Non-Executive Chairman

Peter Bradley is an experienced corporate lawyer with over 35 years advising on capital raising, mergers and acquisitions, and corporate transactions across private and public markets. He has worked extensively in Europe and Asia, both as a partner in City law firms and in senior in-house roles, providing strategic and transactional counsel to boards ranging from start-ups to large listed companies. Mr Bradley brings broad corporate governance and strategic oversight experience to the board.

Anthony Hamilton — Chief Executive Officer

Anthony Hamilton is a seasoned energy executive and accountant with more than 35 years of experience in investment advisory and natural resources. His background spans oil & gas, gold, diamonds, base metals and property development. Previously, Mr Hamilton served as CEO of an oil & gas company where he raised US$55m and oversaw production operations of 28mmcfd, covering both onshore and offshore assets. He also played a key role in developing Zimbabwe’s and North America’s first commercial diamond mines.

Mark Wallace — Executive Finance Director

Mark Wallace is a Chartered Accountant with a Bachelor of Economics and Accounting and over 25 years of experience in global financial markets. He has held senior roles at major investment banks and advisory firms including Standard Chartered Capital Markets, Cantor Fitzgerald, Credit Lyonnais and NatWest Capital Markets. Mr Wallace has deep expertise in structuring funding for development and operational assets across commodities, with strong knowledge of offtake markets and project financing.

John Heugh — Executive Technical Director

John Heugh holds a BSc (Hons) in geology from the University of New England and drilling engineering qualifications from the University of Texas, Austin. With more than 50 years in oil and gas exploration, he brings rare technical depth to Georgina’s leadership. Mr Heugh was a founding director of Central Petroleum Ltd — one of Australia’s largest acreage holders with extensive helium, hydrogen and hydrocarbon exploration experience — and has held senior roles in multiple energy ventures, raising in excess of US$500m for exploration and development.

Roy Pitchford — Non-Executive Director

Roy Pitchford is a resource sector executive with over 30 years’ experience. He was previously Non-Executive Chairman of MMM plc, which acquired Georgina Energy plc, and was formerly CEO of Vast Resources plc. His career includes senior leadership positions at AIM-quoted African Minerals Limited, African Platinum plc and Zimbabwe Platinum Mines Ltd (ASX-listed). Mr Pitchford is a qualified Chartered Accountant and brings significant executive and managerial expertise across resource development projects.

Sam Quinn — Company Secretary

Sam Quinn is a corporate lawyer with more than 15 years’ experience in the natural resources sector in both legal counsel and management roles. He is a principal of Silvertree Partners, a London-based corporate services provider specialising in the natural resources industry. Mr Quinn has significant experience in company administration, financing and investor relations for listed and private resource companies, and has previously served as Director of Corporate Finance and Legal Counsel for a London-based natural resources venture capital firm.

Bob Liddle OAM — Native Title & Indigenous Affairs Consultant

Bob Liddle OAM has over 50 years of experience in Indigenous affairs and corporate relationship building in Australia. He is one of the country’s most experienced practitioners in Indigenous engagement and has provided consultancy services to major energy and mining companies, including Santos, CRA, Western Mining Corporation, BHP Gold and Hexagon Energy. Mr Liddle was awarded the Order of Australia Medal in 2013 for his services to the oil and gas exploration and production industry.

Global helium market: structurally constrained supply

Helium is a strategic industrial gas with no practical substitutes and a highly concentrated global supply base. Unlike oil or natural gas, helium cannot be synthetically manufactured at scale and is typically produced as a by-product of conventional natural gas processing, meaning supply is largely incidental rather than demand-driven.

Independent industry forecasts indicate that global helium demand is expected to grow steadily over the coming decade. On a volumetric basis, estimates suggest demand of c6.4bcf in 2025, rising to c8.9bcf by 2031, implying a compound annual growth rate of around 5–6%. Longer-term projections indicate that demand could reach 12–13bcf by 2035, driven by structural growth in semiconductor manufacturing, advanced electronics, cryogenics and emerging technologies such as quantum computing.

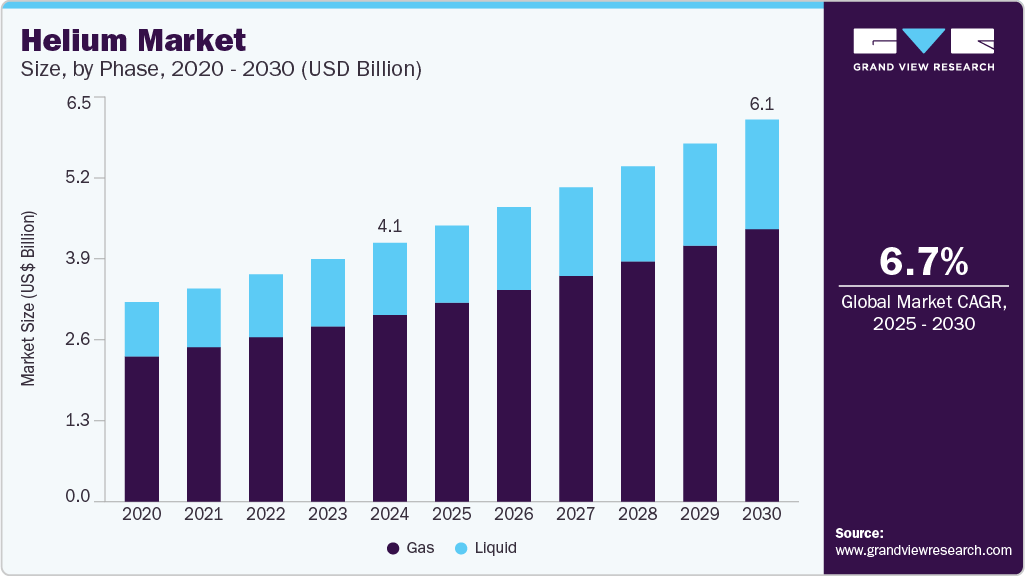

This volumetric growth is reflected in market value forecasts, with independent research projecting the global helium market expanding from cUS$4.1bn in 2024 to cUS$6.1bn by 2030, underscoring both rising demand and the strategic value of secure supply.

Global helium market size (USDbn) 2024–2030

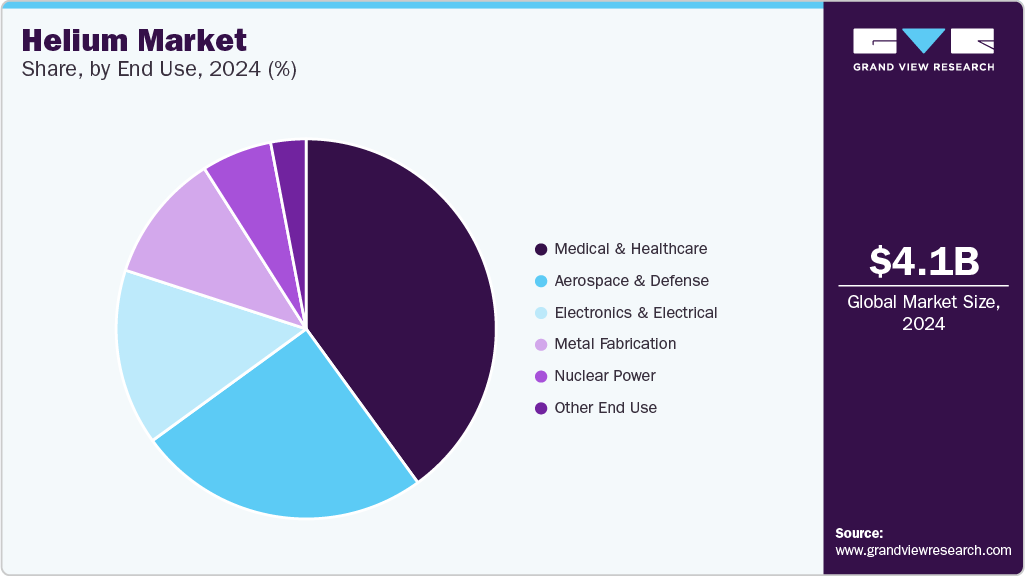

Global helium market by end use 2024

Importantly, this growth is occurring against a supply base that remains concentrated and largely dependent on by-product production from natural gas processing, limiting supply responsiveness and reinforcing the case for new, reliable sources of primary helium.

During Q3 2025 the price of bulk helium in the US was US$101,903/MT or US$478/mcf.

Over the past decade, the global helium market has been characterised by:

As a result, the market has experienced repeated supply shortages, with demand continuing to grow across critical end uses such as medical imaging (MRI), semiconductor manufacturing, fibre optics, aerospace and advanced research. Importantly, demand in these sectors is price inelastic — consumption is driven by necessity rather than discretionary spending.

In this context, new sources of reliable helium supply are increasingly valued, particularly those that can be brought online without reliance on large-scale LNG infrastructure or multi-year development timelines.

Why helium is different: no substitutes, limited flexibility

Helium’s investment characteristics differ materially from conventional hydrocarbons. It is chemically inert, non-renewable and irreplaceable in many of its applications. Unlike natural gas, demand destruction is limited even at elevated prices, and long-term supply contracts are common once production is established.

For producers, this results in:

For investors, this means that asset value is often driven less by spot pricing assumptions and more by confidence in deliverability and reliability of supply. Projects that can demonstrate consistent production, even at modest volumes, can therefore command attractive economics.

Primary vs by-product helium: relevance to Georgina

Most global helium is produced as a by-product of natural gas processing, typically at concentrations well below 0.3%. In contrast, Georgina’s assets target primary helium and hydrogen systems, where reported helium concentrations are materially higher.

This distinction is important, as higher helium concentrations can:

Combined with the Company’s focus on re-entry and appraisal rather than frontier discovery, this positions Georgina’s portfolio toward smaller-scale, potentially faster-cycle helium developments that are aligned with market needs for incremental supply.

Hydrogen: emerging co-product rather than core valuation driver

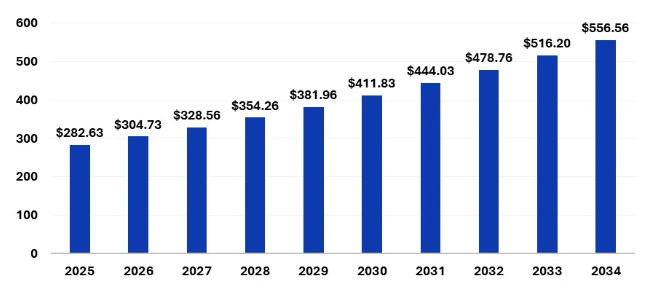

Hydrogen adds a complementary layer to GEX’s narrative. While global hydrogen markets remain at an earlier stage of development than helium, industrial demand is expanding and policy support is increasing across key jurisdictions. Independent forecasts project the global hydrogen market growing from approximately US$260bn in 2025 to over US$550bn by 2034, implying a compound

annual growth rate of around 7–8%, underpinned primarily by established industrial uses rather than speculative end markets.

Global hydrogen market size (USDbn) 2025–2034

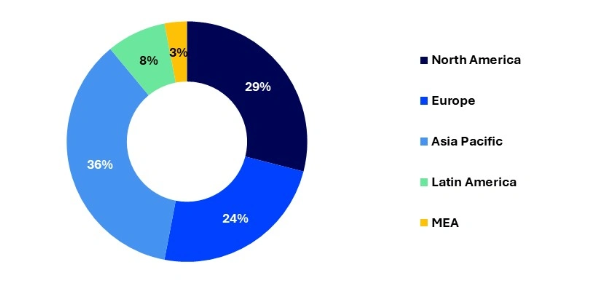

Global hydrogen market share by region 2024

Within Georgina’s portfolio, hydrogen is best viewed as a co-product with longer-dated optionality, rather than a primary valuation driver. Recorded subsurface hydrogen flows across multiple wells indicate a working system, and hydrogen may enhance project economics through blending or selective monetisation as markets mature.

This approach allows hydrogen to strengthen the strategic relevance of the portfolio without introducing undue reliance on evolving policy or pricing assumptions.

Market implications for valuation and timing

In a market characterised by structural helium scarcity, projects that combine:

are increasingly scarce. As a result, such projects are likely to attract disproportionate strategic interest relative to earlier-stage frontier exploration plays.

For Georgina, the combination of market dynamics and portfolio maturity supports the view that incremental technical progress — flow optimisation, appraisal success or offtake progression — could translate into meaningful valuation uplift as assets move closer to commercial reality.

Helium-3 potential

In addition to conventional helium (predominantly helium-4), naturally occurring helium systems can contain trace quantities of helium-3 (³He), a rare isotope generated through radiogenic and mantle-related processes and preserved in long-lived, well-sealed geological settings. Within Georgina Energy’s portfolio, assets targeting fractured basement and subsalt structural traps - including Mt Kitty, Hussar and Mt Winter - exhibit geological characteristics consistent with environments where helium-3 has been identified elsewhere globally.

Indeed, an article in the Australian Petroleum Producers Association (now the Australian Energy Producers) in 2018 reported the presence of 3He at levels up to 1,100 ppt in analysis of gas from Mt Kitty. This is 22% higher than the 900ppt reported by Gold Hydrogen (ASX: GHY) at its Ramsay Project in South Australia.

Helium-3 remains a niche and highly specialised market, with applications in advanced scientific research, cryogenics, neutron detection and longer-term fusion research. While not a driver of near-term project economics and not included in base-case valuation, helium-3 typically commands orders of magnitude higher unit values than conventional helium-4, meaning that even trace concentrations could represent longer-dated strategic optionality if confirmed.

Helium economics differ fundamentally from those of conventional natural gas. While both are gases produced from the subsurface, helium is a scarce, non-renewable industrial input with no viable substitutes in many end uses, whereas natural gas is an abundant energy commodity priced largely on volume and calorific value.

As a result, helium pricing is orders of magnitude higher than natural gas pricing on a per-unit basis. Whereas natural gas prices are typically measured in a few dollars per mcf, helium pricing is commonly quoted in hundreds of US dollars per mcf, reflecting its scarcity, specialised applications and the high cost of supply security.

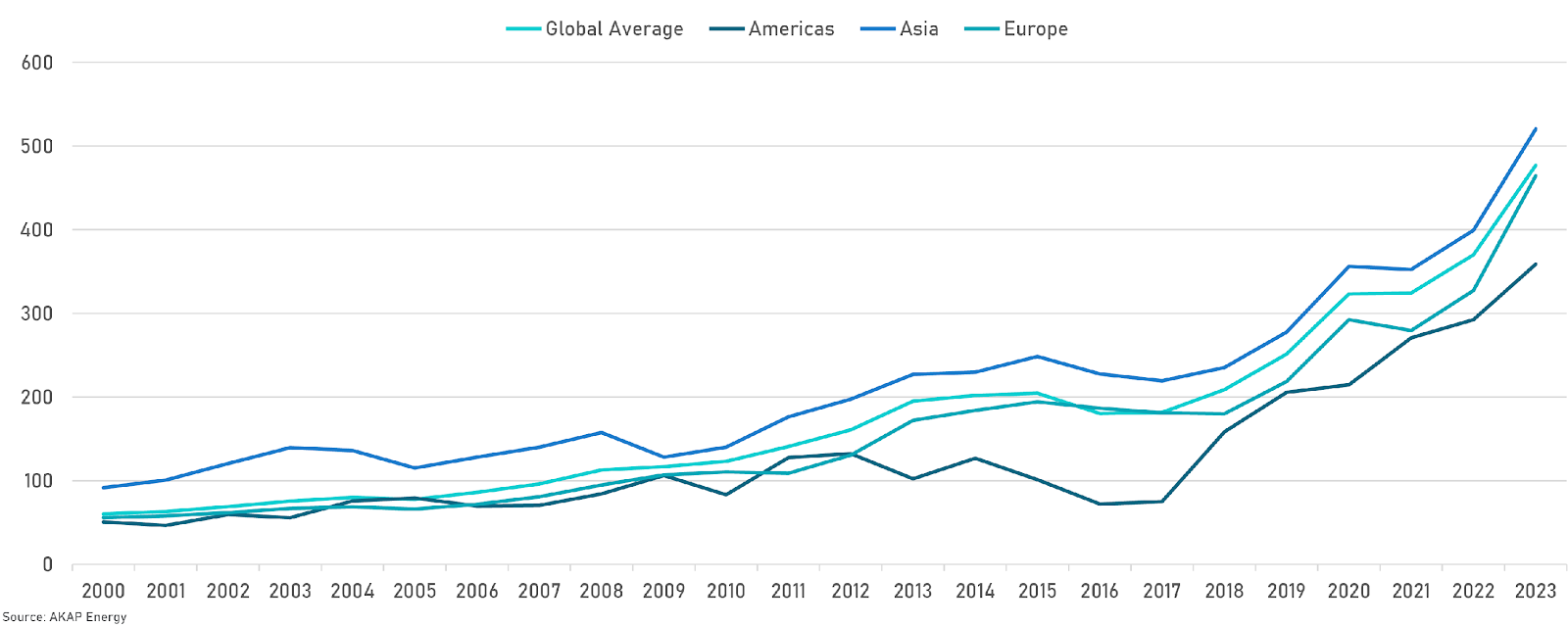

Global helium import prices by region (2000 – 2023)

Crucially, helium is not traded on transparent exchanges. Instead, pricing is typically determined through bilateral, long-term contracts, with outcomes influenced by purity, reliability of supply, delivery method and customer-specific requirements. During periods of supply tightness — which have recurred several times over the past decade — pricing has demonstrated significant upward sensitivity as buyers prioritise security of supply over headline cost.

This structural pricing dynamic has important implications for upstream projects. Unlike natural gas developments, where commercial viability often depends on achieving large throughput volumes, helium projects can be economically attractive at relatively modest flow rates, provided concentrations are sufficiently high and logistics are manageable.

For Georgina Energy, this distinction is central to the investment case. Assets such as Mt Kitty have demonstrated helium concentrations measured in percentage points, materially above levels typically associated with by-product helium in conventional gas fields. This supports a value framework based on high-value molecules rather than high-volume production, and helps explain why relatively small resource bases can still underpin meaningful commercial outcomes.

Hydrogen markets are structurally different again and remain at an earlier stage of development. While hydrogen pricing is currently more fragmented and policy-driven, its relevance within the portfolio is best viewed as complementary to helium, with potential to enhance project economics over time rather than drive near-term valuation.

Given the opaque and contract-based nature of helium markets, explicit pricing assumptions are addressed later in the report alongside valuation sensitivities. At this stage, the key takeaway is that helium operates in a fundamentally different pricing regime to natural gas, reshaping how scale, flow rates and commercial thresholds should be interpreted.

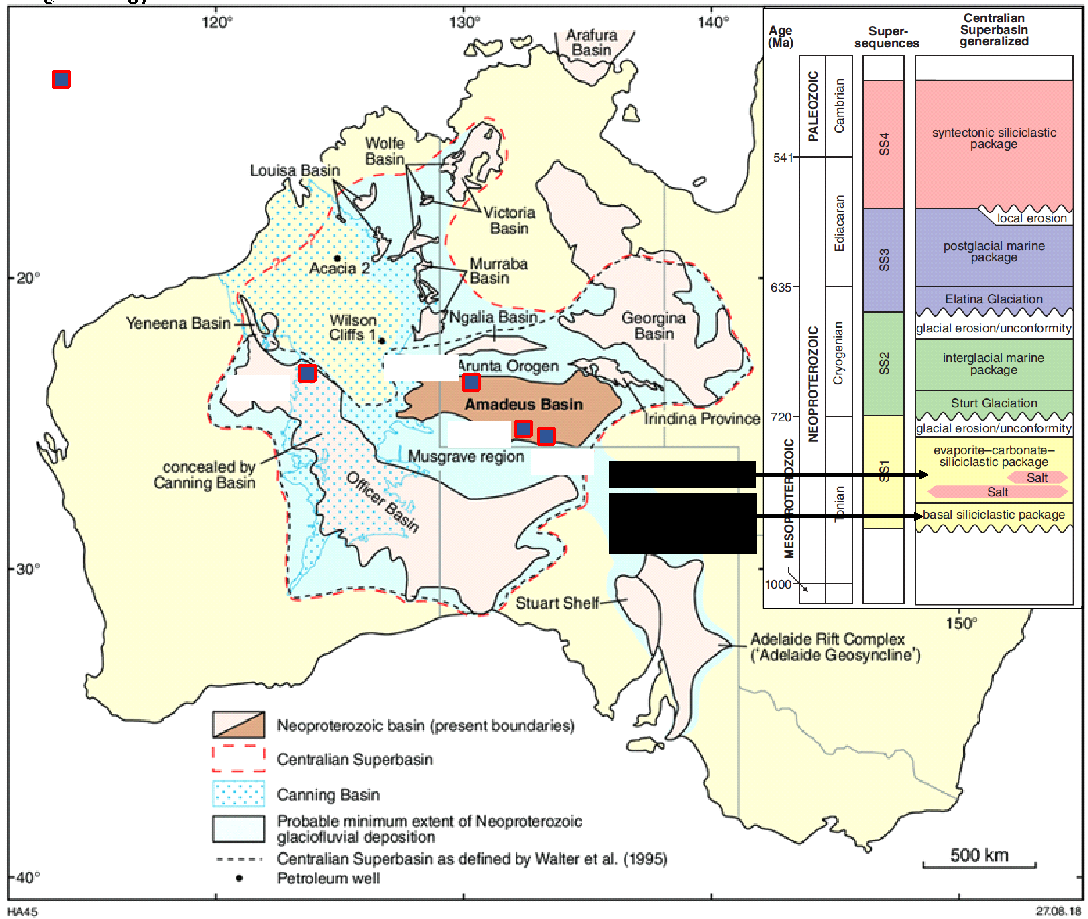

Basin overview

Georgina Energy’s asset base is concentrated across two large onshore sedimentary basins in central and western Australia: the Amadeus Basin and the Officer Basin. Both share a common origin in the Neoproterozoic Centralian Superbasin, with the two basins separating in the Cambrian and both having remarkably similar Precambrian sedimentary sequences and essentially similar prospectivity in the same play type for helium and hydrogen. Both basins are characterised by long geological histories, extensive seismic coverage and a legacy of hydrocarbon exploration, providing a substantial technical dataset relative to many frontier helium provinces.

Amadeus and Officer basins

Importantly for GEX, both basins host sub-salt geological systems capable of trapping helium, hydrogen and associated gases, with historical wells demonstrating anomalously high helium concentrations and confirmed gas mobility.

Geological framework

Amadeus Basin

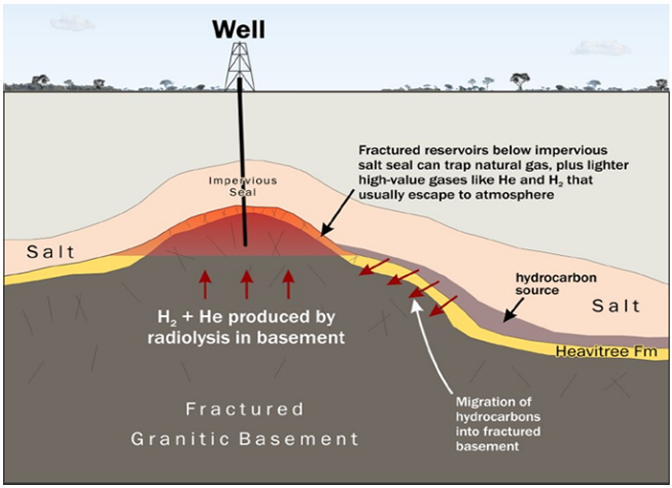

The Amadeus Basin is a Proterozoic–Palaeozoic intracratonic basin that has undergone multiple phases of deposition, deformation and uplift. Of particular relevance to GEX’s assets is the Neoproterozoic subsalt play, where thick evaporite sequences (including the Gillen Salt) act as regionally effective seals.

Key geological features include:

Historical drilling in the basin has recorded helium concentrations measured in percentage points, significantly above global averages for by-product helium, supporting the thesis that the basin hosts primary helium systems rather than incidental accumulations.

Illustrative subsalt helium and hydrogen play concept

Officer Basin

The Officer Basin shares several geological similarities with the Amadeus Basin, including Proterozoic sedimentation, thick evaporite development and structurally complex basement architecture. Like the Amadeus, it has been under-explored historically for non-hydrocarbon gases, despite multiple wells encountering gas shows.

Key attributes include:

While the Officer Basin remains less advanced than the Amadeus in terms of drilling density, its scale and geological architecture provide longer-dated upside within GEX’s broader portfolio.

Implications for helium and hydrogen

The geological characteristics of both basins are well aligned with the requirements for commercial helium and hydrogen accumulations, namely:

Crucially, the presence of salt-sealed subsurface systems reduces the risk of gas leakage and supports the preservation of helium over geological time, a key differentiator relative to basins lacking regional seals.

Operating environment

From an operational perspective, both basins benefit from:

These factors support a development model based on re-entry and staged appraisal, rather than capital-intensive frontier exploration. They also allow lessons learned at one asset to be transferred efficiently across the portfolio.

Portfolio summary

Georgina Energy’s portfolio comprises a focused set of onshore helium and hydrogen assets located across the Amadeus and Officer Basins in Australia. The portfolio is deliberately weighted toward re-entry and appraisal-led opportunities, where gas presence has already been demonstrated through historical drilling or robust independent volumetric assessment, materially reducing geological uncertainty relative to frontier exploration.

The near-term investment case is anchored by three advanced Amadeus Basin assets — Mt Kitty, Dukas and Mahler — acquired from Central Petroleum and supported by an independent

Competent Person’s Report completed in March 2025. These assets benefit from prior drilling, defined re-entry targets and independently assessed contingent and prospective resources.

In addition, Georgina retains material upside across its legacy portfolio, most notably at Mt Winter in the Amadeus Basin and Hussar in the Officer Basin. Both assets have published independent prospective resource estimates and provide longer-dated optionality within the same subsalt geological framework as a near-term execution catalyst rather than a longer-dated optionality play.

Summary of key assets and independently assessed resources (unrisked)

Portfolio interpretation and strategic relevance

The portfolio exhibits a clear tiering of maturity and risk. Mt Kitty stands out as the most advanced asset, with contingent resources underpinned by historical flow to surface and a defined re-entry strategy focused on improving reservoir contact through horizontal drilling. As such, Mt Kitty represents the clearest near-term appraisal and execution opportunity.

Dukas provides the largest volumetric upside within the Amadeus Basin, with independently assessed prospective resources at a scale that could support standalone development if appraisal success is achieved. Mahler offers a smaller but shallower complementary opportunity within the same basin framework.

Mt Winter and Hussar provide material scale upside within the portfolio, with both assets now benefiting from secured or advancing pathways toward near-term drilling. The Hussar funding announcement materially elevates the asset's strategic importance, positioning it alongside Mt Kitty

The scale of resources at Hussar - now estimated at 283bcf helium, 315bcf hydrogen and 2.9tcf hydrocarbons on a 2U basis - represents the single largest prospective resource concentration across the portfolio. Combined with non-dilutive drilling funding secured from Harlequin Energy,

Hussar has transitioned from exploration concept to a funded drilling programme, marking a clear step-change in portfolio maturity and de-risking trajectory.

Mt Winter and Hussar extend the portfolio beyond the near-term re-entry focus, offering large-scale prospective resource exposure across both the Amadeus and Officer Basins. These assets benefit from the same subsalt trapping model but remain earlier stage, providing longer-dated optionality that can be progressed selectively as capital and technical priorities permit.

Mt Winter, while remaining earlier stage in terms of drilling readiness, benefits from extensive technical work and large mapped closure, providing complementary Amadeus Basin scale exposure as the Company's execution focus broadens beyond Mt Kitty alone. Mt Winter and Mt Kitty are fundamentally the same subsalt play types in the same basin.

Near-term re-entry and appraisal opportunity with contingent resources

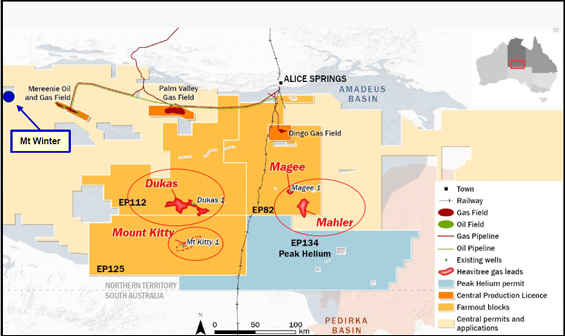

Mt Kitty is located in the southern Amadeus Basin within licence EP125 and represents Georgina Energy’s most advanced asset, forming the cornerstone of the Company’s near-term appraisal strategy. The asset hosts an existing suspended exploration well (Mt Kitty-1) drilled by Santos as part of earlier basin exploration activity, which encountered gas and flowed to surface, providing direct evidence of a working subsurface system.

Map of Central Petroleum acquisition assets relative to Mt Winter location

Mt Kitty was acquired as part of the Central Petroleum transaction and is supported by an independent Competent Person’s Report completed in March 2025, which classified the asset as hosting 2C contingent resources. The presence of a drilled well, tested gas flow and independently assessed resources differentiates Mt Kitty from the rest of the portfolio in terms of maturity and execution readiness.

The availability of historical drilling, test data and seismic interpretation allows the forward work programme to focus on re-entry and optimisation, rather than frontier exploration.

Geological setting

Mt Kitty is situated within a subsalt geological framework typical of the Amadeus Basin. The prospect is defined by a large, fault-bounded structural closure developed above fractured crystalline basement and overlain by regionally extensive evaporite sequences that provide an effective seal.

Seismic mapping undertaken by Central Petroleum delineates a closure of material areal extent, up to c600 km2/c150,000 acres with vertical relief sufficient to support the accumulation and long-term retention of helium, hydrogen and associated gases beneath salt.

Seismic mapping of Mt Kitty closure

Key geological elements include:

This setting is consistent with the subsalt play concept illustrated earlier in the report and underpins the rationale for targeting improved reservoir contact through re-entry.

Well history and proof of gas

The CPR notes that Mt Kitty-1 did not encounter the primary Heavitree Formation reservoir target on the crest of the anticlinal structure. Instead, gas flowed to surface from fractured granodiorite basement, where the well intersected a bald crestal anticline.

During testing, the well flowed gas to surface at approximately 0.5mmcfd, confirming the presence of a mobile gas system and validating the integrity of charge and seal. While the tested gas contained a large component of nitrogen, the CPR highlights extraordinarily high helium and hydrogen concentrations within the gas stream of 9% helium and 11.5% hydrogen.

The CPR further implies that the tested flow rate is not necessarily representative of the asset’s productive potential, reflecting the fact that the well was not optimally positioned within the primary Heavitree target and was drilled as a vertical intersection with limited fracture contact. This underpins the rationale for a horizontal drilling re-entry strategy focused on maximising reservoir exposure.

Fractured basement reservoir potential and development analogues

The presence of productive fractured crystalline basement at Mt Kitty has important implications for development strategy and potential recoverable volumes. While Mt Kitty-1 was a vertical exploration well that intersected naturally-fractured granodiorite over a limited interval, the company's technical team has identified significant scope to enhance reservoir contact and flow rates through horizontal or multi-lateral well designs.

The relevance of fractured basement plays should not be underestimated. The Bach Ho field in the Cuu Long

Basin offshore Vietnam provides a compelling analogue: it produces from fractured granodiorite basement - the same lithology encountered at Mt Kitty - within a similar "buried hill" structural setting. At its peak, Bach Ho delivered approximately 270,000 barrels of oil per day (bopd) and 142 mmcfd of natural gas from a structural closure of only circa 90 km².

By comparison, the aerial closure at Mt Kitty is estimated at approximately 600 km², more than six times larger than Bach Ho. While direct comparisons between oil-prone and gas-prone fractured basement systems require caution, the Bach Ho analogue demonstrates that fractured granodiorite reservoirs can sustain world-class production rates over multi-decade timeframes when effectively contacted.

At Mt Kitty, any field development would likely involve multiple wells, potentially incorporating multi-lateral completions designed to intersect the maximum number of natural fractures. The original vertical well at Mt Kitty-1 would have intersected vertical to sub-vertical fractures at approximately 90-degree angles, providing limited reservoir contact. Horizontal wells drilled parallel to the fracture strike could feasibly intersect significantly more fractures per metre drilled, potentially delivering flow rates materially in excess of simple vertical-to-horizontal scaling ratios.

This underscores the distinction between proving gas presence, which Mt Kitty-1 achieved, and optimizing reservoir contact and deliverability, which remains the focus of the planned re-entry programme. While uncertainty around ultimate recoverable volumes remains high at this stage, the fractured basement play concept is supported by global analogues and represents a credible basis for commercial-scale development if appraisal is successful.

Resources

An independent Competent Person’s Report completed in March 2025 assessed Mt Kitty as hosting 2C contingent resources, reflecting demonstrated gas in place and the expectation of commercial recovery subject to execution of a defined development plan.

On an unrisked basis, Mt Kitty is estimated to contain:

The contingent classification reflects the requirement to demonstrate improved productivity through re-entry and flow optimisation, rather than uncertainty over gas presence or trapping.

Development and re-entry strategy

The forward development plan at Mt Kitty is centred on re-entering the existing Mt Kitty-1 wellbore and drilling a horizontal or deviated section designed to materially increase contact with the fractured basement and/or basal reservoir intervals.

This approach is intended to:

Re-entry leverages existing infrastructure and subsurface knowledge, offering a capital-efficient and lower-risk pathway to appraisal compared with drilling a new exploration well.

Key risks and sensitivities

The principal risks at Mt Kitty are engineering and execution-related, including the ability to achieve sustained fracture connectivity, manage wellbore stability during re-entry and demonstrate repeatable deliverability through extended testing.

These risks differ fundamentally from frontier exploration risk and are considered more controllable through well design, completion techniques and iterative optimisation.

Strategic relevance

Mt Kitty represents the most tangible opportunity for Georgina to demonstrate repeatable helium and hydrogen production, progressing from contingent resources to appraisal and early development and establishing a technical and commercial template that can be applied across the wider Amadeus Basin portfolio.

As such, performance at Mt Kitty is likely to act as a key catalyst for broader portfolio valuation and strategic interest.

Officer Basin flagship with secured drilling funding and upgraded prospective resources

Hussar is located within the Officer Basin under licence EP513 and represents Georgina Energy's principal asset outside the Amadeus Basin. Following the announcement of secured drilling funding from Harlequin Energy on 28 January 2026, Hussar has transitioned from a longer-dated exploration prospect into a near-term execution catalyst, joining Mt Kitty as a core portfolio anchor.

The asset is held at 100% working interest and has been the subject of detailed technical review supported by independent Competent Person's assessment. The prospect provides geographic diversification while retaining exposure to a broadly analogous subsalt geological system to that proven across the Amadeus Basin.

Geological setting and structural framework

Hussar is defined by a very large subsalt structural closure developed above fractured crystalline basement and sealed by regionally extensive evaporite sequences characteristic of the Officer Basin. The geological model mirrors that successfully applied across the Amadeus Basin, with helium and hydrogen interpreted as being generated through radiogenic processes at depth and retained beneath competent salt seals over geological time. The subsalt target zones in the Officer Basin and the Amadeus Basin were both part of the same Centralian Superbasin in Neoproterozoic times.

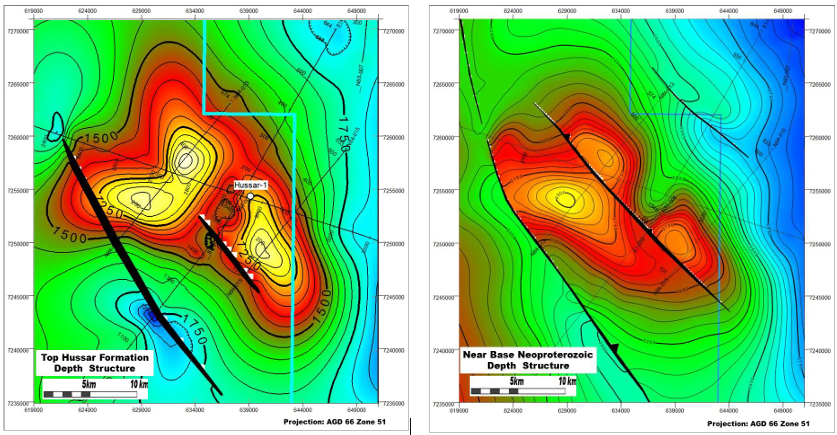

Depth structure maps of Top Hussar Formation (left), and Near Base Neoproterozoic (right)

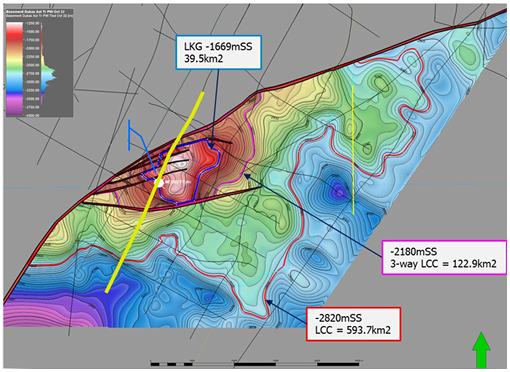

The structure has been mapped using regional 2D seismic acquired in the 1980s and subsequently reprocessed, supplemented by gravity and magnetic data. Seismic interpretation delineates a closure with an aerial extent estimated at approximately 300 km², making it one of the largest mapped subsalt structures across Georgina's portfolio.

The primary reservoir target is the Townsend Quartzite, a basal Neoproterozoic clastic unit that is the stratigraphic equivalent of the Heavitree Formation in the Amadeus Basin. This unit is overlain by the evaporitic Browne Formation, which provides the regional seal. The geological succession at Hussar therefore shares close similarities with the proven helium-bearing systems at Mt Kitty and Magee-1 in the Amadeus Basin, supporting the technical rationale for drilling.

Well control: Hussar-1 and proof of working petroleum system

Unlike many basin-scale exploration prospects, Hussar benefits from legacy well control. The Hussar-1 well was drilled by Eagle Corporation Limited in 1981-1982, reaching a total depth of 2,040m within massive halite of the upper Browne Formation, above the target Townsend Quartzite reservoir.

While Hussar-1 did not reach the primary reservoir objective due to operational constraints, the well encountered significant gas shows throughout the drilled section wherever porosity was present. Key observations from the well completion report include:

These observations confirm an active petroleum system at Hussar and provide direct evidence of mobile gas within the sealing sequence immediately above the target reservoir. The presence of gas shows in supra-salt intervals is particularly encouraging, as it indicates gas charge, migration and trapping mechanisms are operational within the broader Hussar structure. It is pertinent to note the helium and hydrogen were not tested for in 1981-1982 when the well was drilled.

Importantly, subsequent seismic mapping by the Geological Survey of Western Australia (Simeonova and

Lasky, 2005) revised again by an independent Competent Person, concluded that Hussar-1 was not drilled on the structural crest and was potentially located off-structure. This suggests the well may have intersected the flanks of the closure rather than the optimal trapping position, leaving the crestal area - and the primary Townsend Quartzite reservoir - untested.

Prospective resources: upgraded estimates

Following continued technical work and calibration against Amadeus Basin analogues, Georgina announced updated prospective resource estimates for Hussar on 28 January 2026. The revised 2U (P50) estimates on an unrisked basis are:

The upgrades reflect:

These volumes position Hussar as the single largest prospective helium and hydrogen resource within the portfolio, albeit with all volumes remaining unrisked and subject to discovery and appraisal.

Hussar funding breakthrough: US$25m non-dilutive drilling facility

On 28 January 2026, Georgina announced that Harlequin Energy Ltd has confirmed its intention to fund the drilling of the Hussar-2 well through a structured US$25 million offtake funding facility. This facility is non-dilutive for existing shareholders and will cover:

The funding is structured as an offtake-linked facility, contemplating future commercial arrangements for helium, hydrogen and natural gas recovered from the well. While full commercial terms remain subject to final agreement and proof of funds, the commitment from Harlequin validates the commercial attractiveness of the Hussar prospect and provides Georgina with a pathway to drill a major exploration well without immediate equity dilution.

The facility structure aligns with broader industry trends in helium and hydrogen financing, where offtake partners are increasingly willing to provide development capital in exchange for long-term supply arrangements. This model reduces upfront capital requirements for explorers while providing offtakers with exposure to new supply sources in markets characterised by structural scarcity.

Forward drilling programme and objectives

The Hussar-2 well is planned as a re-entry of the Hussar prospect, drilling approximately 1,000-1,200m of new hole to reach the Townsend Quartzite reservoir and penetrate into underlying crystalline basement. The well objectives are to:

Drilling is expected to commence in Q3/2026 subject to rig availability and completion of definitive agreements with Harlequin. Given the secured funding and existing well infrastructure, Hussar-2 represents a near-term drilling catalyst that could materially de-risk the Officer Basin portfolio.

Hussar drilling timetable

Strategic relevance and valuation implications

The combination of secured drilling funding, upgraded prospective resources and legacy well control positions Hussar as a near-term value driver alongside Mt Kitty, albeit with a different risk-reward profile:

From a portfolio perspective, Hussar provides:

The successful execution of the Hussar-2 drilling programme could represent a company-defining catalyst, particularly given the scale of prospective resources and the potential for follow-on development if gas is encountered. While outcomes remain binary at this stage, the risk-reward profile is materially enhanced by the secured funding structure and the upgraded resource base.

Large-scale subsalt helium and hydrogen prospect with material upside

Dukas is located in the southern Amadeus Basin within licence EP112 and represents the largest volumetric opportunity within Georgina Energy’s portfolio. The asset was acquired from Central Petroleum and is supported by an independent Competent Person’s Report completed in March 2025, which classified Dukas as hosting material 2U prospective resources across helium, hydrogen and associated natural gas.

The CPR highlights that Dukas is defined by a very large mapped subsalt closure of approximately 1,000km², which is significant in the context of onshore helium exploration and underpins the scale of the prospective resource assessment.

Geological setting

Dukas is a fault-bounded subsalt anticline developed above fractured crystalline basement and sealed by regionally extensive evaporites. The mapped closure exhibits substantial areal extent and structural relief, supporting the potential for large gas accumulations beneath salt.

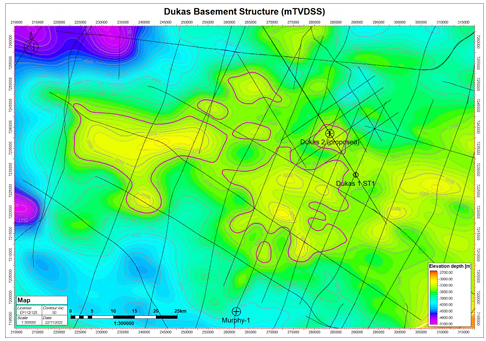

Dukas basement structure inc. Dukas 1 ST-1 and proposed Dukas 2 locations

Reservoir potential is interpreted within fractured basement and basal clastic intervals, with faulting and structural complexity enhancing migration pathways and trap effectiveness. The CPR notes that the size of the closure supports the accumulation of material gas volumes even at modest effective reservoir thickness.

Well control and exploration maturity (Dukas-1 / ST-1)

Unlike pure frontier prospects, Dukas benefits from direct well control. The CPR references the Dukas-1 / ST-1 well, which provides important subsurface calibration for the structure and supports elements of the geological model applied in the prospective resource assessment. Sample analysis while drilling confirmed the presence of helium (2.1%), hydrogen (0.4%), hydrocarbons (29.4%) and other inert gases in the circulating mud system from drilled cuttings, just above the Heavitree Formation target. This confirms an active gas play with unusually high Helium concentrations similar to that encountered at the Mt Kitty-1 well is present at the Dukas Prospect.

While the CPR continues to classify Dukas as prospective (and therefore subject to discovery and appraisal risk), the presence of a historical well provides additional confidence in structural interpretation and stratigraphic understanding relative to undrilled closures.

Resources

The independent CPR assessed Dukas as hosting 2U prospective resources (P50) on an unrisked basis of:

These estimates reflect the large structural closure mapped at Dukas (c1,000km²) and the application of reservoir and charge assumptions consistent with the broader basin model.

Forward strategy and execution considerations

At Dukas, the forward work programme is expected to focus initially on further technical maturation, including seismic refinement and well planning, prior to committing to drilling a second well or re-entry activity. Any future appraisal is likely to leverage learnings from Mt Kitty and other Amadeus Basin operations, particularly in relation to optimal well orientation and fracture targeting.

Given the scale of the structure, Dukas is likely to warrant a phased appraisal strategy, with early wells focused on demonstrating deliverability and gas composition prior to any broader development planning.

Strategic relevance

Dukas provides exposure to material basin-scale upside within the Amadeus Basin, complementing the nearer-term execution focus at Mt Kitty. While earlier stage, the combination of very large mapped closure (c1,000km²) and independently assessed prospective resources positions Dukas as a potential medium-term value driver as technical risk is reduced.

Large-scale fractured basement and basal clastic prospect with independently assessed prospective resources

Mt Winter is located in the southern Amadeus Basin within licence EPA155 and represents one of the largest volumetric opportunities in Georgina Energy’s legacy portfolio. The asset is held at 100% working interest and is supported by an independent Geological Report (IGR) completed in July 2025, which assessed prospective resources across helium, hydrogen and associated natural gas.

Mt Winter has previously been drilled, although the early well(s) did not penetrate the targeted subsalt Heavitree Formation nor the fractured basement target. Drilling did encounter significant hydrocarbon shows within sandstones and siltstones of the Bitter Springs Formation, directly above the Mt Winter Prospect reservoir target. The hydrocarbon shows confirm that an active petroleum system exists within sealing units immediately above the target reservoir. Neither helium nor hydrogen was tested for when the drilling took place in 1981. The prospect also benefits from extensive seismic coverage and a detailed volumetric assessment incorporating fracture porosity within basement and basal reservoir intervals. As such, Mt Winter provides scale-driven upside within the same subsalt geological framework that underpins the Company’s core Amadeus Basin assets.

Geological setting

The IGR describes Mt Winter as a large fault-bounded subsalt structure developed above fractured crystalline basement and overlain by regionally extensive evaporite sequences. The geological model mirrors that applied across the Amadeus Basin, with helium and hydrogen generated at depth and retained beneath salt over geological time.

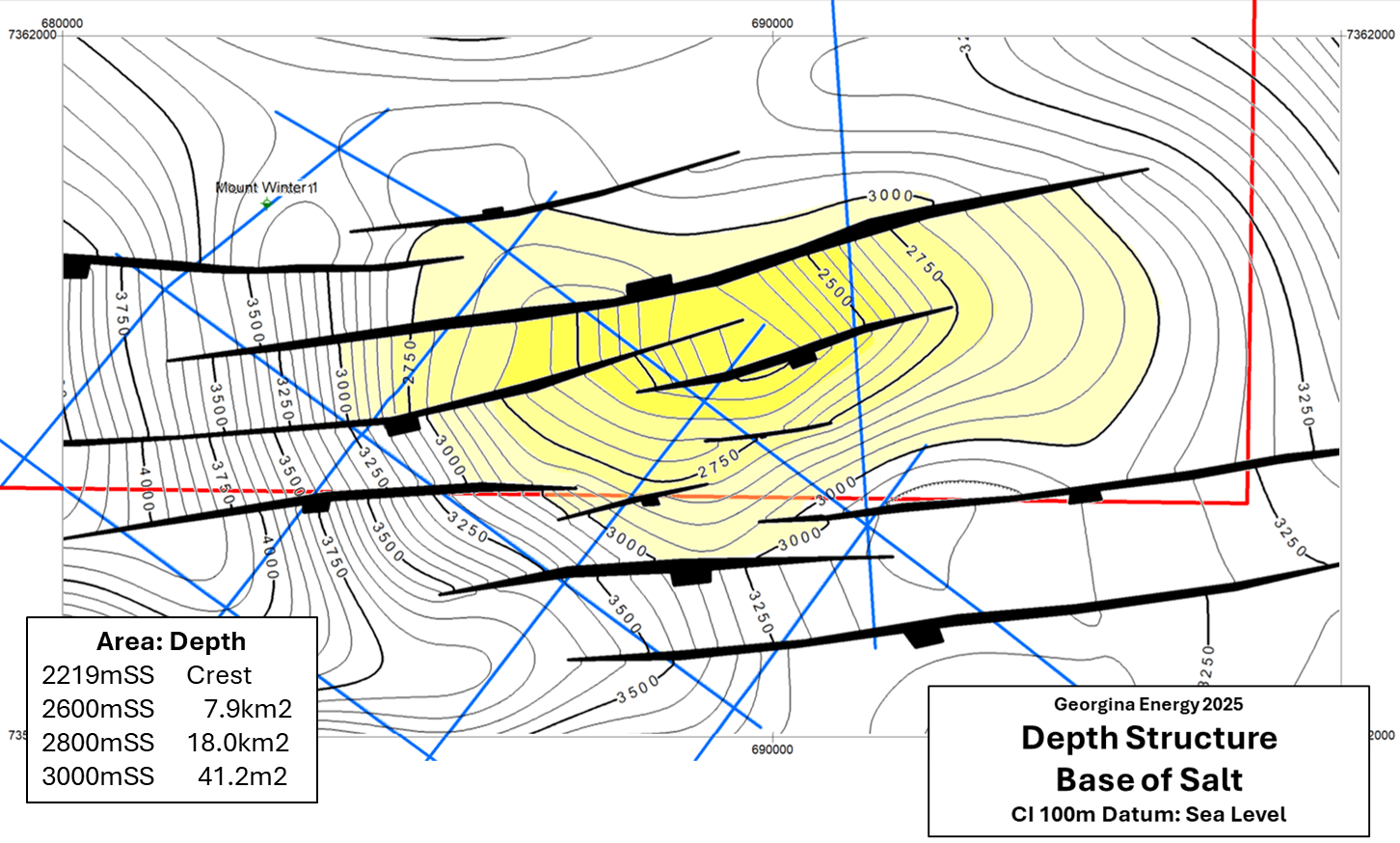

Depth structure map (50m contours) at base of salt across the Mt Winter prospect area

Reservoir potential is interpreted within:

Importantly, the IGR explicitly incorporates fracture porosity into the volumetric assessment, reflecting learnings from analogue wells elsewhere in the basin and enhancing confidence in effective reservoir presence.

Prospect definition and technical work

Mt Winter has been defined through seismic interpretation and structural mapping, with the IGR delineating a large aerial closure with sufficient vertical relief to support material gas accumulations. While the targeted reservoir horizons remain undrilled, the scale of the mapped structure and the incorporation of fracture porosity represent a more advanced level of technical maturity than many early-stage exploration prospects, thus substantiating the planned prospect re-entry.

The IGR notes that the size of the closure supports the accumulation of significant gas volumes even under conservative assumptions for reservoir thickness and porosity.

Resources

The July 2025 IGR assessed Mt Winter as hosting 2U prospective resources (P50) on an unrisked basis of:

These volumes reflect the large structural closure mapped at Mt Winter and the explicit inclusion of fracture porosity within the resource estimation methodology.

Forward strategy and execution considerations

As outlined in the IGR, Mt Winter is expected to be progressed through further technical maturation and selective drilling, with well design likely informed by learnings from Mt Kitty and other Amadeus Basin activity, particularly with respect to fracture targeting and well orientation.

Given its scale, Mt Winter may ultimately support a phased appraisal strategy, with initial wells focused on confirming deliverability and gas composition prior to broader development planning.

Strategic relevance

Mt Winter provides material longer-dated upside within the Amadeus Basin, complementing the near-term re-entry focus at Mt Kitty and the basin-scale optionality at Dukas. The combination of large prospective resources, 100% working interest and CPR-supported fracture porosity assumptions positions Mt Winter as a potentially significant contributor to portfolio value as technical risk is reduced.

Infrastructure and operating environment

Georgina’s projects benefit from onshore locations within established energy basins. In the Amadeus Basin, existing pipelines and processing plants built for conventional gas provide options for tie‑backs or third‑party handling. The Stuart Highway and all‑weather access roads pass close to the principal licences, supporting year‑round operations. Electricity and water supplies are available from nearby communities. In the Officer Basin, the Hussar EP513 lease is remote but traversed by graded tracks and supported by a large airstrip capable of taking Hercules-sized aircraft. It lies within a region targeted for critical‑minerals development, meaning infrastructure upgrades could be co‑funded with other resource developers. Both basins fall under Australian federal and territorial regimes that are supportive of new gas and hydrogen projects, with the Northern Territory’s Critical Minerals Strategy and federal Hydrogen Roadmap signalling a willingness to streamline permitting and co‑invest in downstream infrastructure.

Australian operating infrastructure

Pricing context and commercial considerations

The AKAP Energy import pricing chart presented earlier highlights just how different helium economics are from conventional natural gas. Long‑term contract prices across major regions were typically in the US$350–500 per thousand cubic feet (mcf) range in 2023, with spot transactions occasionally spiking higher in tight markets. Natural gas prices, by comparison, have remained in the single‑digit dollars per mcf. This order‑of‑magnitude gap is the reason Georgina’s projects can potentially be commercialised at relatively modest flow rates and without requiring LNG‑scale infrastructure. The pricing environment is opaque because helium is sold under bilateral contracts; realised prices depend on purity, delivery terms and reliability of supply. Hydrogen pricing is even more project‑specific and policy‑driven: green hydrogen benchmarks are presently higher than grey hydrogen costs, but naturally occurring hydrogen from Georgina’s prospects would likely be priced via bespoke agreements with industrial partners. Detailed pricing assumptions and sensitivities will therefore be addressed in the valuation section, but the headline message is clear: helium’s high unit value means smaller volumes can support attractive economics.

Helium monetisation pathways

Given the pricing backdrop, Georgina’s strategy focuses on modular, scalable development. Key elements include:

Hydrogen as a complementary option

Hydrogen discovered in Georgina’s wells is currently viewed as longer‑dated upside. Naturally occurring hydrogen could be monetised as an industrial feedstock, blended into natural‑gas streams, or upgraded to ammonia depending on future demand and policy incentives. Australia’s hydrogen strategy envisions export hubs and domestic consumption growth, suggesting a pathway for low‑emission hydrogen by the early 2030s. However, until appraisal wells confirm consistent volumes, hydrogen will not drive near‑term capital decisions or valuation.

Partnering and government support

In addition to Halo Capital, Georgina’s assets have historical involvement from Santos and Central Petroleum, both of whom have experience in the Amadeus Basin and may become future partners in appraisal or development. Government initiatives to secure critical minerals and strategic gases, as well as grant programmes for hydrogen projects, offer further avenues for co‑investment in processing and logistics. The company intends to maintain flexibility around funding structures, balancing equity, farm‑ins and offtaker finance to minimise dilution.

Framework and methodology

We value Georgina Energy using a risked net asset value (NAV) approach, reflecting the Company’s pre-development asset base, the absence of production cash flows and the importance of staged technical de-risking. This methodology is standard for pre-development resource companies and allows asset-level value to be adjusted transparently for geological, technical and commercial risk.

The valuation is constructed on a sum-of-the-parts basis, with individual asset NAVs aggregated and adjusted for corporate items including estimated net debt, working capital and overheads.

Asset valuation and scenario analysis

Hussar Project

The Hussar valuation reflects a distinctive commercial structure based on an independent February 2025 scoping study. Under this model, Georgina develops the gas field and sells raw gas at the wellhead to an offtake partner, who constructs and operates the separation facility required to extract helium, hydrogen and LNG from the nitrogen-rich gas stream.

This approach materially reduces Georgina’s capital exposure while maintaining significant economic participation. The Company is responsible for field development costs estimated at US$0.50-$2.00/mcf (all-in basis including wells, gathering infrastructure and production operations), while the offtake partner funds construction of the gas separation plant, estimated at US$1.13 billion for a 40mmcfd facility based on adapted cryogenic nitrogen rejection technology.

Wellhead gas pricing is contracted at US$4.00-$10.00/mcf depending on scenario, reflecting the value of the helium-hydrogen-hydrocarbon mix net of separation costs. This structure is consistent with the non-dilutive US$25 million offtake funding facility announced in January 2026 with Harlequin Energy Ltd, which contemplates similar commercial arrangements for the Hussar-2 well and potential Phase 1 development.

The Hussar project valuation is based on a 20-year Phase 1 development targeting the Townsend Quartzite reservoir and underlying fractured basement. Key operational assumptions include:

Wellhead pricing reflects the value split between field operator (Georgina) and plant operator (offtake partner), with three scenarios capturing the range of potential commercial outcomes:

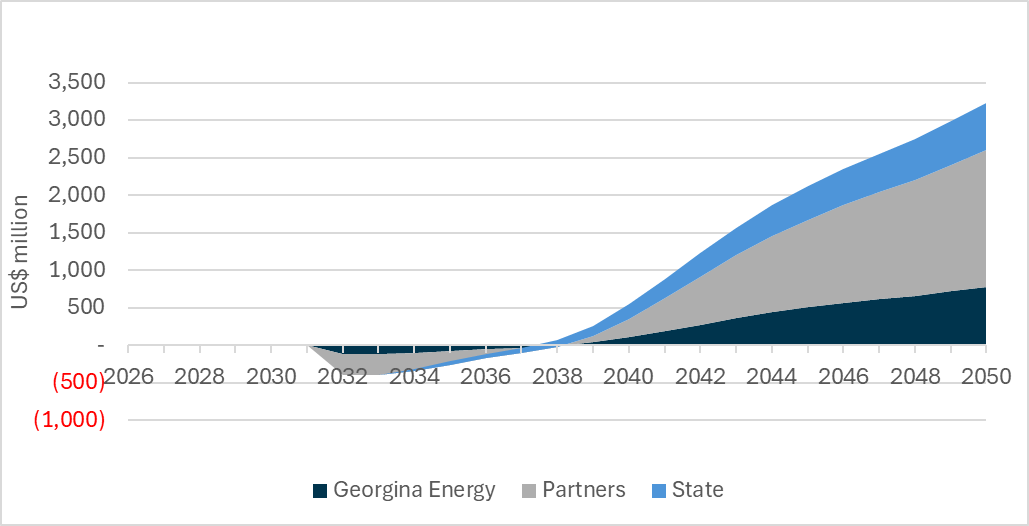

The base case demonstrates field-level economics generating $1.8 billion in cumulative 20-year EBITDA on $221m of field capex, with the offtake partner separately funding the $1.13bn gas separation plant. Under base case assumptions, the project (excluding the separation plant) generates a pre and post-tax NPV10 of $292m and $154m, and pre and post-tax IRRs of 27.3% and 20.9% net to GEX. Even the low-price scenario maintains economic viability with $1.0bn cumulative EBITDA, providing downside protection.

Hussar project NPV sensitivities ($m)

Hussar project cumulative undiscounted cashflow ($m)

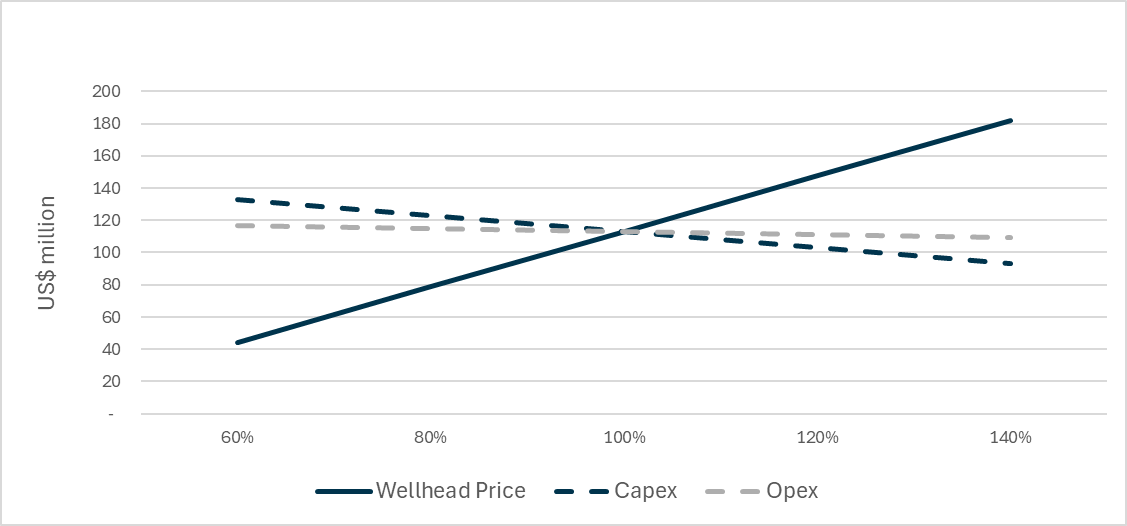

Mt Kitty Project

The Mt Kitty valuation adopts an integrated development model where Georgina retains both upstream field development and midstream processing operations. The project targets 2C contingent resources of 93 bcf (comprising 21 bcf helium, 27 bcf hydrogen, and 45 bcf natural gas) through a 25-year horizontal well development programme.

This contrasts with Hussar’s wellhead sale model. At Mt Kitty, Georgina funds and operates on-site Pressure Swing Adsorption (PSA) processing to separate and purify helium, hydrogen and LNG for sale. While this increases gross capital requirements to $400m ($120m net to GEX’s 30% interest), it captures the full value chain and generates materially higher returns per unit of gas produced.

The development is de-risked by the Mt Kitty-1 well (2014), which successfully flowed 500mcfd of gas with 9% helium and 11.5% hydrogen concentrations from only 155m of fractured basement penetration. The horizontal well programme is designed to intersect naturally fractured systems more effectively, with 500m laterals targeting multiple vertical fracture sets. Key base case assumptions include:

The valuation assumes conservative helium pricing at $350/mcf (significantly below the $700/mcf used in the Hussar scoping study and recent market prices exceeding $900/mcf), hydrogen at $9.44/mcf, and natural gas at $5.00/mcf. Revenue is dominated by helium sales (c94% of total), with hydrogen and LNG providing modest uplift.

Unlike Hussar’s pricing-focused scenarios, Mt Kitty scenarios address well productivity and reservoir performance risk, reflecting the critical uncertainty in horizontal well EUR and the number of wells required to develop the 2C resources:

The base case assumes 32 horizontal wells across three phases of drilling, each delivering 7.5bcf EUR, consistent with fractured basement analogs. The conservative case reflects higher decline rates and lower fracture connectivity, requiring 47 wells for full field development. The upside case assumes superior fracture intersection and productivity, reducing well count to 28. Under the base case, the project generates a pre-tax NPV10 of $983m at the project level ($295m net to GEX’s 30% working interest) with a pre-tax IRR of 35.8%. Post-tax NPV10 and IRR are $475m ($142m net to GEX) and 24.3%, respectively.

Mt Kitty project NPV sensitivities ($m)

Mt Kitty project cumulative undiscounted cashflow ($m)

Target price methodology

Our target price is set at Core NAV of 46p / £76.5m (risked), representing approximately 5x current market levels. This valuation framework deliberately excludes £407m of risked exploration NAV, providing a conservative base case that captures only near-term, lower-risk development assets while preserving substantial optionality for exploration success.

The Core NAV of £76.5m comprises:

Importantly, Core NAV assumes helium pricing of $350/mcf - less than half the $700/mcf in the Hussar scoping study and well below recent spot prices exceeding $900/mcf. This conservative pricing provides significant embedded upside without requiring helium market tightness.

Excluded exploration upside (£407.4m risked):

The exclusion of the exploration upside from the target price reflects a conservative approach focused on derisked near-term catalysts and lower geological uncertainty. However, successful execution at Mt Kitty (Q1-Q2 2026 re-entry) and Hussar (H2 2026 drilling) would validate the subsalt play concept basin-wide, supporting progressive re-rating toward the £484m full portfolio NAV—representing over 40x current market levels (c30x share price when incorporating dilution).

Key re-rating catalysts within target price framework:

By anchoring the target price to Core NAV only, we adopt a framework requiring no exploration success beyond funded/significantly derisked assets, conservative helium pricing, and probability weightings reflecting current stage rather than optimistic assumptions. This provides downside protection through a narrowly defined value base while preserving asymmetric upside through multiple re-rating catalysts over 12-24 months. The 5x upside to Core NAV represents compelling value for a portfolio transitioning from frontier exploration toward funded appraisal and near-term development.

Sensitivity analysis

The two projects demonstrate fundamentally different risk-return profiles, reflected in their distinct scenario frameworks and economic outcomes. The economic outcomes demonstrate Mt Kitty’s superior returns per dollar invested, reflecting its integrated structure and high helium concentration, offset by higher absolute capital requirements and execution complexity (although it should be noted that the Hussar project will be exposed to similar complexity and overall higher capital costs borne by the offtaker).

Mt Kitty demonstrates significantly higher IRRs (35.8% pre-tax vs 27.3% for Hussar base case) and NPV per dollar invested (2.47x vs 1.33x), reflecting the value captured through integrated processing despite the company holding only 30% working interest. The $983m project-level pre-tax NPV10 translates to $295m net to Georgina, compared with $292m for Hussar (100% WI).

However, Mt Kitty’s superior returns come with materially higher execution risk. The integrated model requires Georgina to fund and operate PSA processing infrastructure ($160m capex), exposes the company to helium price volatility across the full production stream, and depends on achieving horizontal well productivity targets (7.5 bcf EUR per well). By contrast, Hussar’s wellhead sale structure transfers processing risk to the offtake partner and provides a more predictable revenue stream, albeit at lower absolute returns.

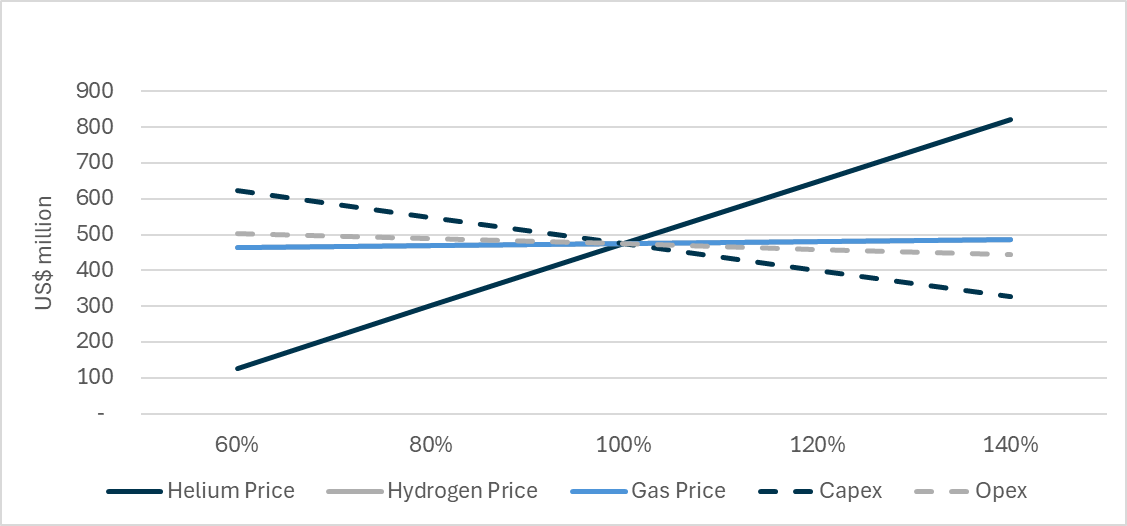

The scenario analysis highlights the critical sensitivities for each project: Hussar success depends primarily on securing favourable wellhead pricing ($7-10/mcf range), while Mt Kitty success depends on well performance and helium pricing. Notably, Mt Kitty’s base case valuation assumes conservative helium pricing at $350/mcf — less than half the $700/mcf used in the Hussar scoping study and well below recent spot market prices exceeding $900/mcf. This provides substantial upside optionality if helium markets tighten or if the company secures premium contract terms.

Core NAV sensitivity to helium price and Hussar wellhead sales

The tables above and below show the sensitivity of our Core NAV and RENAV to helium price and Hussar wellhead sales price, being the two most important assumptions behind our valuation.

Risking methodology

All asset values are explicitly risked to reflect stage of development:

Risking is applied at the asset level rather than through aggressive pricing or cost assumptions, maintaining transparency and conservatism in the valuation framework. The relative risk weightings reflect the interplay between geological certainty (higher at Mt Kitty due to Mt Kitty-1 well results) and commercial/execution risk (higher at Mt Kitty due to integrated processing model).

The investment case is underpinned by a clearly defined sequence of near- and medium-term technical and commercial catalysts, increasingly weighted toward execution and appraisal rather than frontier exploration. Importantly, the recent Hussar funding announcement introduces a second, fully funded drilling programme alongside Mt Kitty, materially strengthening near-term news flow.

Timings below are indicative and subject to regulatory approvals, operational execution and partner alignment.

Near-term catalysts (Q1–Q2 2026)

Mt Kitty re-entry and appraisal programme (Q1–Q2 2026)

Re-entry of the Mt Kitty-1 well and drilling of a horizontal or deviated section designed to materially increase contact with fractured basement and/or basal reservoirs. This is the Company’s lowest geological-risk technical catalyst.

Initial flow testing and gas composition confirmation at Mt Kitty (Q2 2026)

Early flow testing under optimised well design, including confirmation of sustained flow rates and helium and hydrogen concentrations. Results will be critical in validating the transition from geological proof-of-concept to engineering execution.

Finalisation of Hussar-2 well planning and long-lead items (Q1–Q2 2026)

Progression of detailed well design, procurement of long-lead items and final permitting ahead of drilling, following confirmation of non-dilutive funding.

Medium-term catalysts (H2 2026)

Extended flow testing and appraisal results at Mt Kitty (H2 2026)

Longer-duration flow testing to assess deliverability, pressure behaviour and operational stability, supporting potential resource re-classification and commercial discussions.

Potential resource upgrades at Mt Kitty (H2 2026)

Subject to successful appraisal, independent reassessment of contingent resources and potential progression toward reserves.

Commencement of Hussar-2 drilling (Q3 2026)

Drilling of the Hussar-2 well targeting the subsalt Townsend Quartzite reservoir and underlying fractured basement, fully funded via the Harlequin offtake-linked facility. This represents a high-impact exploration and appraisal catalyst given the scale of prospective resources.

Medium- to longer-term catalysts (2027 onwards)

Hussar-2 well results and appraisal outcomes (2027)

Evaluation of gas presence, helium and hydrogen concentrations and reservoir deliverability at Hussar, with outcomes likely to be company-defining given the scale of the prospect.

Progression of offtake and commercial structures (2026–2027)

Advancement of binding offtake, processing or pre-payment arrangements under the Halo Capital framework and other potential counterparties, informed by appraisal results.

Portfolio progression across Amadeus Basin assets (2027+)

Selective appraisal or drilling at Dukas and Mahler, incorporating learnings from Mt Kitty and Hussar and prioritising capital-efficient, re-entry-led opportunities.

Summary

The catalyst profile is now anchored by two parallel execution tracks: a lower-risk re-entry and appraisal programme at Mt Kitty and a fully funded, large-scale drilling campaign at Hussar. Together, these provide multiple opportunities for value inflection through 2026–27, with outcomes driven increasingly by execution and deliverability rather than binary frontier exploration risk.

Investment in Georgina Energy is subject to a range of risks typical of early-stage resource companies. The most material risks are outlined below.

Technical and execution risk

While Mt Kitty benefits from an existing well and demonstrated gas flows, the success of the re-entry and appraisal programme is not assured. Achieving sustained commercial flow rates will depend on effective reservoir contact, fracture connectivity and wellbore stability. Poor execution, mechanical issues during re-entry or sub-optimal completion design could result in lower-than-expected flow performance or delays.

Although these risks are fundamentally different from frontier exploration risk, they remain material and could impact the timing or viability of development.

Resource and appraisal risk

Resource estimates are based on independent CPRs and geological reports but remain subject to uncertainty. At Mt Kitty, contingent resources require successful appraisal to confirm commercial deliverability. At Dukas, Mahler, Mt Winter and Hussar, prospective resources are inherently higher risk and dependent on future drilling success.

There is no guarantee that resources will be converted to reserves, or that estimated volumes will be recovered on commercially viable terms.

Commercialisation and offtake risk

Helium markets are opaque and contract-based, with pricing and terms negotiated bilaterally. While this can support premium pricing, it also introduces uncertainty around realised prices, contract duration and counterparty commitment.

Memoranda of understanding, including the Halo Capital framework, are non-binding and may not result in definitive agreements. Failure to secure suitable offtake or processing arrangements could delay development or require alternative funding structures. That said, the non-exclusive MOU with Harlequin Energy for hydrogen (and potentially helium and LNG) offtake from both Hussar and Mt Winter, combined with Harlequin's confirmed commitment to fund the Hussar-2 well, provides a degree of commercial validation and suggests offtake interest is advancing beyond early-stage engagement.

Funding and dilution risk

Georgina Energy does not currently generate operating cash flow and will require funding to progress appraisal and development activity. This may involve equity issuance, asset-level farm-outs or partner funding, any of which could be dilutive to existing shareholders.