Promotion: Capital invested is at risk. Non-Independent Research / Marketing Communication. Attention is drawn to the disclaimers and risk warnings within this document.

BROKER NOTE BY JONATHAN PLANT

written 26th March 2026

Sometimes there are businesses where the plan is so in the sweet spot and the management is so focused on the opportunity that they progress at a speed which the market at large confuses with a mixed message.

Medpal AI from inception was always about creating a powerful Telehealth vertical and they spotted the opportunity, and grasped it, to enter into the clinical dispensing layer of the healthcare model with the Universal Pharmacy deal4.

From inception, and reviewing their business at IPO, it was obvious to us that MPAL is at the cutting edge of the AI interface. They are all about disrupting models but with a purpose. Too many devices, apps, fragmented data. Healthcare markets and insurers disjointed, all in an era where information and science have never been so prolific and advanced.

The UK market for health is broken. Speak to most people about the NHS system and trying to access their doctor and the lucky ones will have an appointment in two weeks time. Pharmacies are closing or going out of business (over 1,000 since 202638). Manual dispensing has a 2% error rate and chronic disease management is an after thought. This is why the online pharmacy /Telehealth model is growing so quickly.

The first incarnation of Medpal had already identified the data disconnect problem. 1.4bn people globally using digital health tools40, with over 50% of UK adults owning a wearable device41 but with so few joined options where the data leads you down the chain to healthcare delivery. Medpal would look to solve this with the app that was device and operating system agnostic and partnerships to move you down the vertical to telehealth practitioners.

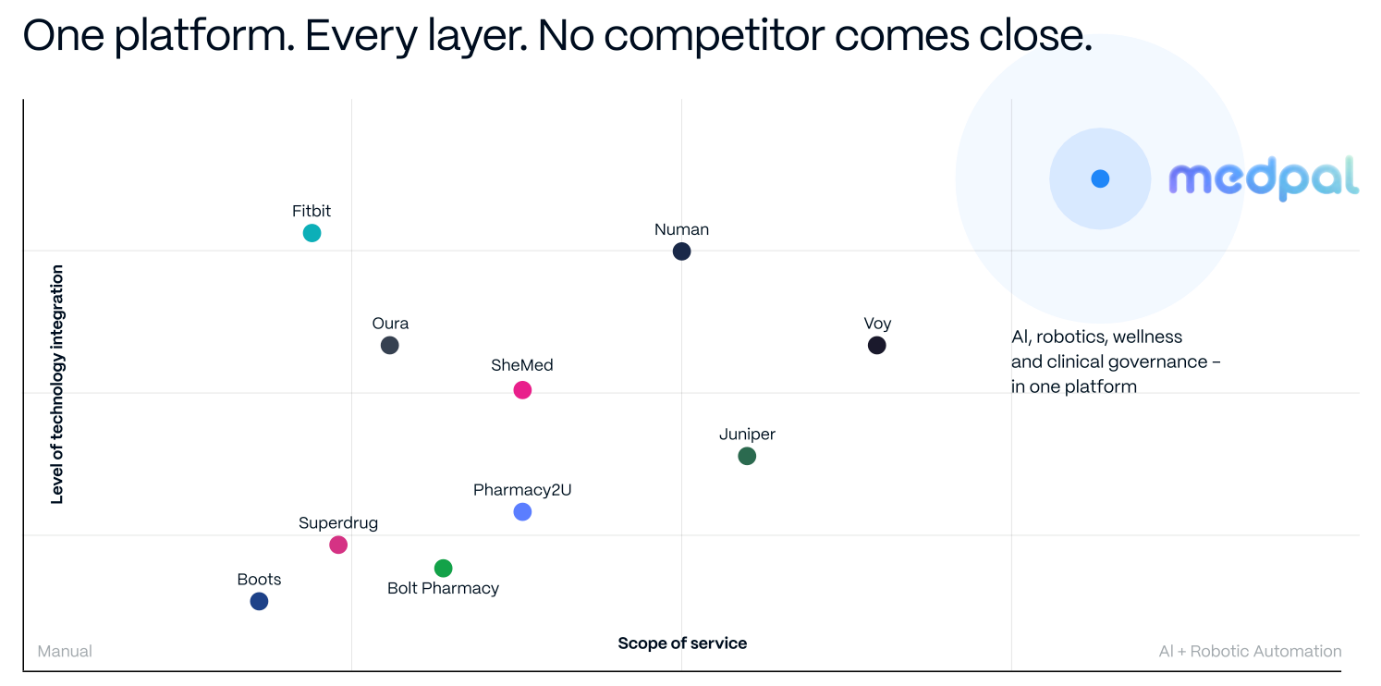

Medpal has evolved significantly in a short space of time. The goal of making wellness and healthcare instantly accessible and affordable for everyone is still the aim and with a focus on rebuilding the UK system. They should be at the front end of this as they have actually moved down the vertical and are focused on patient interaction now. Effectively they are now solving patient healthcare needs and reversing them into health management. The technology platform combined with robotic automation puts Medpal in the upper quadrant of offerings and built to outperform at scale.

The routes to the MedPal ecosystem have expanded beyond the app to medpal.clinic and WhatsApp interaction with a clinician-trained AI.

Focusing data and behaviours into a centralised dispensing model with 24/7 clinical support and delivery nationwide within a day. They have reached incredible scale in a short time without short-cuts in a regulated health market trying its best to remove bad actors whilst improving customer outcomes.

The Latest operational release5 gave a truly exceptional performance for a silo that only started in November 2025.

147,000 items (prescriptions) averaging 35,000 per month,

Total Revenue £1.5m+

15% growth mom in prescriptions39 (which allows for valuations inline with tech sector metrics)

with 111 care homes serviced39

8300 app users39

From an investment perspective you bought into the concept of a one stop hub, rationalising the usage of devices and apps, with a route to individualised advice and referral down the chain to what looked like tele-health partners and ultimate clinician solutions. The November jump into the vertical has not delivered the share price performance that it should have in my opinion.

This is perhaps due to the nature of the AIM market and the increased usage of ATM (At The Market) raise facilities. Whilst these make sense in a lot of situations, particularly in arbitrage situations like Digital Treasury companies (DATCOs) where you are taking advantage of NAV differences between the share price and underlying crypto-currency, for the mainstream you are playing with a more speculative investor. They are perhaps less sticky than the direct placing method where there is a more focused reasoning for the funding and investor evaluation. It would appear that this has materially affected the share price performance than what the fundamentals suggest.

MedPal have not only vertically integrated but they have expanded into a scale opportunity with the use of best-in-class robotics that will allow for operational leverage, quick upscaling and most likely a self-fulfilling scaled benefit upside for users and company alike. They are seen as noisy neighbours in the space but have actually built a very strong moat already. As an investor you need confidence that not only is the concept enduring but that it has a large chance of revenue growth, profits and payouts. Something that can scale large enough to move up through the markets and reach that investment oasis of the main markets and institutional investor interest and funding. They are in a very competitive and highly scrutinised sector in terms of regulation and ethics but appear to be addressing all these concerns systematically and with competitive advantage.

As we have cautioned before though AI solutions are developing at a frightening speed but due to a combination of licencing and clinical scrutiny focus, they have a strong moat around their UK business.

It is our belief that Medpal is materially undervalued at 2.5p, the latest fund-raising price, with the imminent marketing push, scaled operation and expansion into higher value clinic segments should justify at least a 30p price target in the next 18 months. We’ll demonstrate below how that value could still be too conservative.

The Saas-pocalyspe in AI exposed software stocks as illustrated by the IGV chart below will flag as an obvious threat to the model. The carnage caused by Anthropic announcements to software stocks exposed to AI was brutal since Oct/Nov25.

We showed in the previous note how AI businesses were developing so quickly that they were having to re-invent within short timeframes as LLMs infiltrated into areas not previously anticipated. Anthropic has a large footprint in this with seemingly daily updates to Claude’s capabilities. A simple search on Anthropic and telehealth AI reveals6 ...Claude Opus4.5 is building on agentic performance to create Claude for Healthcare. Cue mass panic!!

For MEDPAL, in the UK, this conversely is likely to send traffic into its moat.

OPEN AI receives 250-280m queries per week7 on health-related queries, with 7 out of 10 being made outside clinic hours. Something which MedPal’s clinically trained AI was built for!

UNITED HEALTH CEO death (killer was a star student in AI, moral compass or personal agenda/damage?) Investigators prior to attack had outed them out for a profiteering AI model that was looking to maximise profit over patient outcomes8. This highlights the need for human oversight in the medical vertical which Medpal has to prevent care abuses.

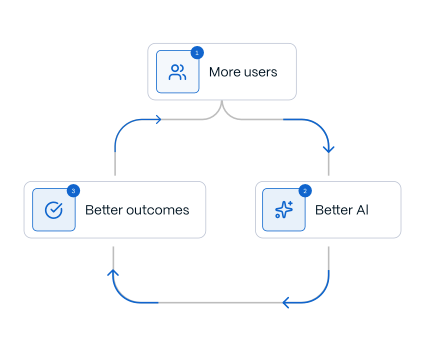

The way the algorithms work is to seek best solutions versus the model given to it, optimising as data improves. Medpal have been marketing light as they ensure their offering is delivery tight for upscale. There is a circular model at work here...

...which should reinforce the Medpal ecosystem at every level. More users create better Ai which creates better outcomes which reinforces user engagement, rinse and repeat

Fulfilling a chronic failure in the UK medical ecosystem by building a scale operation. Two national centres covering 30,000 sq. ft in Swaffham and Runcorn. 130+ years of combined pharmacy experience and national online scaling experience. GPhC-regulated and NHS DSPT compliant. More on this in the regulation section.

Essentially looking to acquire revenue streams form predictable high volume prescription income alongside higher value clinic income with an emphasis on weight loss treatments and other consumer deliverables and chronic disease management solutions.

The idea is repeat customer engagement, winning the customer once and earning repeatedly. Private GP appointments can cost £40+ whereas AI triage can cost pennies relatively. Or you can wait for weeks for your NHS GP. Private health insurance holders may see a virtual GP and elect to use Medpal or Medpal may partner with these insurers going forward, for dispensing.

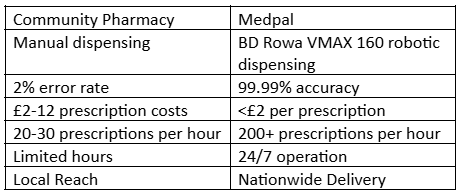

Comparing a Community pharmacy with Medpal’s online dispensing offering highlights a few metrics:

Getting a GLP-1 prescription is relatively easy through private telehealth services if you meet BMI requirements (typically , or with weight-related conditions). However, obtaining it through public systems like the NHS is harder, requiring strict eligibility criteria (e.g., BMI with multiple comorbidities)42

Medpal has a direct supply agreement with Eli Lilly to provide access to GLP-1 medications at scale9

The Medpal offering should appeal to the health-conscious client who wants to improve their lifestyle and stats.

Medium term risks to value proposition as seen by expiry of patents in India10 where copycats of Novo Nordisk are offering Ozempic as low as $14 per treatment. The patent for expiry of semaglutide patent, the molecule in Novo Nordisk's weight-loss drugs Wegovy and Ozempic, is not due until 2031 in the US and UK.

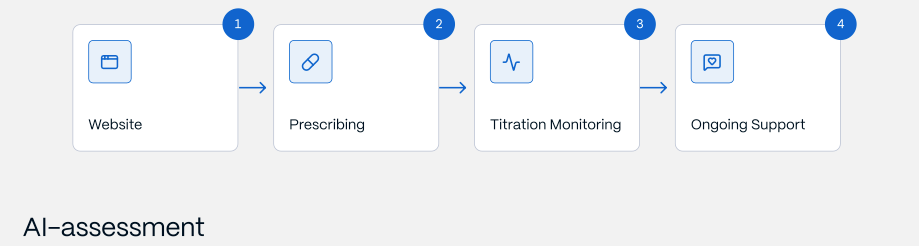

The real power of the offering is the holistic nature of the touch points in the Medpal ecosystem. We know about the app and medpal.clinic is a window into the AI triage. The really interesting driver is the WhatsApp interface – this is relying on Open Claw11 which creates Ai Agents for specific tasks– making apps less relevant and therefore reducing friction between the potential patient and the Medpal ecosystem. Going through the WhatsApp process will see you engage with an agent which is set up to lead you along your most comfortable path. Relevant questions and prompts will be made to you and ultimately you will be able to present your data, BMI for instance via being recorded standing on scales to prove it is your data etc. This is evidence of the AI clinician overlay which develops and learns through the Gemini LLM in the cloud, working and developing in practice.

Athenahealth expands AI-driven patient engagement capabilities12 - Athenahealth will roll out new AI-powered text and voice capabilities by the end of the year that allow patients to self-schedule appointments and fill waitlist slots.

The strategy is to take patients wherever they appear and then migrate them up the value chain. Not everyone will need to have the app. For example, a care-home NHS patient is never going to download the app but they will generate steady, predictable pharmacy income and margin. Medpal’s opportunity is really about the private/clinic engagement.

Take a GLP-1 patient who comes in via medpal.clinic or Google Ads can engage via WhatsApp AI for 24/7 triage and support, and is then encouraged to download the app for ongoing AI-powered health monitoring. The app becomes the retention tool that keeps them in the MedPal ecosystem beyond the initial 12-month GLP-1 treatment window. Repeating and recurring revenue with app engagement and reinforcing data and outcomes for the model.

The clinic site currently pushes toward a 3-month app trial which is the onboarding funnel for the AI wellness proposition. The key insight is that all formats benefit from the AI backbone: WhatsApp uses the same Vertex AI triage engine, the clinic uses it for prescribing decision support, and the app uses it for ongoing monitoring.

It’s going to be difficult to lead a low-margin NHS patient to a paid app subscription. The more realistic play is the reverse-use of the pharmacy infrastructure and NHS credibility as trust signals to attract private patients who then become high-value clinic and app users.

The app is far from obsolete here; It should be positioned as the ongoing care companion that patients receive as part of their clinic subscription. The app AI will identify users with health markers that warrant clinical intervention and route them to medpal.clinic for assessment. Even where the outcome is a GP referral rather than a Medpal prescription, the interaction builds trust and potentially converts them to a dispensing patient. This vertical integration-AI triage to clinical assessment to pharmacy fulfilment is the power of the whole model. All points in the eco-system reinforce the benefits of the ecosystem and vertical to try and maximise revenue collection and data collation.

An app user who engages with the AI wellness tools and identifies a need for weight management becomes a warm lead for the GLP-1 clinic-they’re already in the MedPal ecosystem, they trust the platform, and the conversion path is seamless. Interestingly, because Medpal holds NHS pharmacy contracts and operates as a fully licensed pharmacy, every patient has the option to nominate MedPal as their dispensing pharmacy at sign-up. Once nominated, Medpal automatically supplies all of their prescriptions-both private (GLP-1, clinic services) and NHS-creating a single-provider relationship. This is a powerful bond as a patient who came in for a GLP-1 prescription and nominates Medpal then generates ongoing NHS dispensing revenue from their GP prescriptions at zero incremental acquisition cost. It turns a one-off clinic transaction into a recurring, multi-stream revenue relationship spanning private and NHS, and it’s something the pure-play online prescribers simply cannot offer because they don’t have the pharmacy infrastructure or NHS contracts to fulfil nominations.

The channel opens up the drawbridge... the AI platform and the now closed loop regulated dispensing is the moat below keeping the competition at bay.

Open AI has 250m enquiries per week for health-related queries. MedPal’s AI is trained in the Gemini cloud by clinicians and double checked by human clinicians when the patient solution is revealed. This provides guard-rails against profiteering and bad customer outcomes not to mention regulatory lapse. The industry has a fairly clean history when it comes to licence removal and MPAL has a strong set up to prevent bad behaviours. This should provide confidence to the patient and see real world distribution growth. The Anthropic threats should actually deliver traffic to the most trusted players.

Global digital Health market 2026 -203413

The global digital health market size is projected to grow from USD 491.62 billion in 2026 to USD 2,351.24 billion by 2034, exhibiting a CAGR of 21.60%

UK online pharmacy market – serviceable market14

The UK market alone is expected to more than triple, rising from $12.8 billion in 2024 to $37.6 billion by 2033. Central to this transformation is the rapid expansion of online pharmacies and the increasing use of revolutionary treatments such as Mounjaro — a once-weekly injection now approved for weight management.

As online pharmacy revenues in the UK surge — forecast to grow from $2.73 billion in 2024 to $4.24 billion by 2029, an increase of 55.56% — both the convenience and the complexities of digital healthcare are becoming increasingly evident.

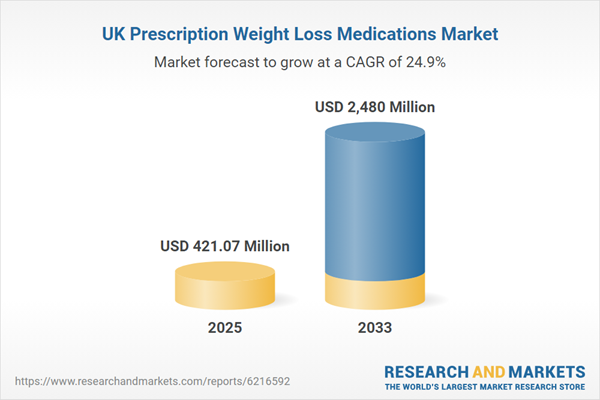

Uk weight management market -The UK prescription weight loss medications market size was estimated at USD 421.07 million in 2025 and is projected to reach USD 2.48 billion by 2033, growing at a CAGR of 24.85% from 2026 to 2033. Growth is driven by rising obesity prevalence, increasing clinical adoption of incretin-based therapies, expanding access through private and digital prescribing channels, and growing patient awareness15

.

The UK prescription weight loss medications market is currently influenced by several key factors. The prevalence of obesity and overweight individuals in the country is a significant driver, as data from March 2025 indicate that approximately 64% of adults in England are classified as overweight or obese, with 29% meeting the criteria for obesity (BMI ≥30 kg/m²).

Growth in NHS GLP-1 prescriptions since 202016

A two-tier system is creating highly unequal access to AOMs based on ability to pay rather than need. IQVIA data show that while approximately 1.4 million people in the UK access GLP-1s every month through private online pharmacies, only an estimated 200,000 are doing so through the NHS, with the majority of these people accessing these drugs for type 2 diabetes, not weight management.

NHS England prescriptions of GLP-1s - which cover only a small share of current usage, with most people accessing the jabs privately - have increased by almost 900% since Autumn 202017.

NHS primary care prescribing spend in 2025 of £11.2bn18

Polypharmacy with older adults on 5 or more medications at once

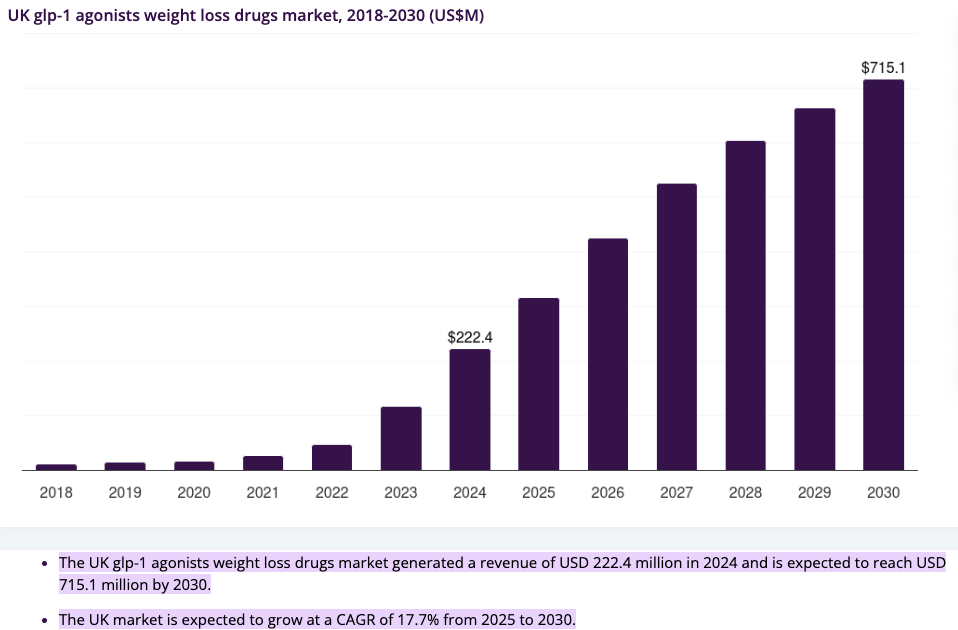

UK GLP-1 market growth to 203019

Although it may feel like weight loss drugs have been around forever, the opportunity is only just going exponential. The Demographic is pre-disposed to obesity and they want to pay to reverse it. Medpal should be able to penetrate into a rising pie and deliver the growth hoped for in the numbers section.

For its online pharmacy, Medpal is regulated by both the General Pharmaceutical Council, which registers and inspects all pharmacies in Great Britain, and NHS England, which enforces the terms for providing NHS services. The company must ensure that it adheres to the terms of its DSP (Distance Selling Pharmacy) licence, with non-compliance potentially leading to suspension or removal from the DSP list. In practice this rarely happens but is now a necessity for Medpal since it has a competitive advantage in holding its DSP. As of 23rd June 2025, the DSP route to establishing a new pharmacy is now closed. The UK pharmacy regulator, the General Pharmaceutical Council, is issuing no new licences. New applications for DSP licences cannot be accepted nor be permitted under amendments made to the NHS (Pharmaceutical and Local Pharmaceutical Services) Regulations 2013. Existing DSPs can continue to operate under the terms of their contracts20.

The DSP pharmacy exemption is being closed for a number of reasons, including the following:

There are approximately 400 DSP pharmacies currently in operation, which should be more than sufficient for England.

While the DSP pharmacy exemption initially helped provide a wider choice for patients, the situation has changed. As many DSP pharmacies are now in place, additional DSP applications are beginning to undermine the integrity of market entry controls – with the establishment of local DSPs established without reference to local patient needs

New ‘local’ DSP pharmacies that establish can undermine the viability of nearby ‘bricks-and-mortar’ pharmacies and threaten their investment in the pharmacy network and the face-to-face provision of (currently Essential) pharmaceutical services they offer to patients.

Concerns over online pharmacies and their ethics have been a recent issue21

Are online pharmacies in the UK legal? There is a fine line between marketing and promoting is a fine one for prescription-only medicines. Data protection is a real risk in health requiring a higher duty of care than retail22

MedPal is a GPhC-registered pharmacy, dispensing only MHRA-approved medications. We follow all UK pharmaceutical regulations to ensure your care is safe and compliant.

We have highlighted the clinical and regulated advantage of the model but these pieces highlight the tricky nature of running too quickly. Medpal has bedded in cleverly.

Still has the potential to proliferate but has stalled as the direct revenue driver for now. It is still fully central to the ecosystem but entering and scaling down the vertical has become the driver of real numbers. Something the AIM market doesn’t often see. Strong metrics, delivering cash flow and a developed, tested ready to scale up structure. You are investing now, and perhaps funding, the firing up of the rockets.

Why has the app stalled? Perhaps there is still a reticence to pay for something that has seemingly adequate substitutes, often provided by the wearable. The ability for the full service offering engaging with Medpal for dispensing and using the app may drive reverse uptake numbers. It is a fine line going down the freemium route and Medpal prefer a trial to show value with payment justified for the level of service. Churn sits at a typical 30% for this model.

Secondly, the reach into the ePassi contract has not been as transparent as it was imagined at outset. Whilst there is a strong relationship with each corporate and gym within their customers the current ePassi direct relationship to the individual doesn’t exist. Having to go gym to gym and to some employee portals has resulted in slow pace of take up. This is being addressed by ePassi as they look to build more portals to access employee groups.

The 8,300 figure represents total registered app users, the vast majority of whom are on the freemium tier. Medpal has not as yet aggressively pushed conversion to paid tiers. Their focus to date has been on building the user base and refining the AI-powered triage and monitoring features. Revenue from app subscriptions, when it comes, will sit within MedPal AI plc. Monthly running costs for the app are modest-primarily Google Cloud Vertex AI inference, hosting, and a small allocation of developer time from the Newsoft partnership, running at approximately £25k/month all in.

ePassi is still an 11m exposure with 2k corporates; there is a profit share on paid subs. These should start to filter through after the initial 12m deal rolls off

UK & Ireland Independent gyms have 2000+ gyms but their deal was a free access for members for 12m trial period also with an eventual 25% commission net of platform fees.

A ramp up of marketing spend is intended and a Director of Marketing impending. These measures could easily see the app spigot turn on.

Universal Pharmacy purchased out of administration for £45k gave Swaffham site in Norfolk which was expanded to 3 warehouses. Wholly-owned by 100% subsidiary Medpal Ltd. There is also a site in Runcorn. Both of which have robot capabilities.

The UK DSP licence (Distance Selling Pharmacy) which allows you to have an NHS pharmacy contract which allows you to have a licence for Rx prescriptions, online and mail order. The main requirements are being legally compliant after assessment and actually performing the business you are licenced for

AI + Robotics allow for 100k+ prescriptions per month (these numbers are discussed as Medpal forecasts in the facilities below).

The NHS no longer issues any licences which has created a barrier for MPAL and the competition. There is a requirement to be clinically compliant. Medpal has trained their AI with the help of the clinicians so that the Triage stage of assessment can take place in a regulatory compliant way. The Ai is trained to ask the right questions. From either MPAL app, WhatsApp, website to Triage. The right Questions asked in the correct way; symptoms data uploads which could be pictures of you standing on the scales. Incentives to take up the app up to the point where the manual dispense overview takes place, then it is over to the robots...Clinicians are in-house but could potentially be outsourced if there is a business reason to do so.

Clinician Availability - Mon–Fri vs 24/7 is a point of marketing fog in the online space where competitors are unclear about the clinician and potential referral on to your GP before approval may be forthcoming. For Medpal the 24/7 advantage is real: patients can submit consultations and interact with WhatsApp AI triage at any time, and the AI can provide immediate clinical guidance, flag contra-indications, and manage ongoing support queries. What requires human input is the final prescribing sign-off, which currently operates Mon–Fri. Prescriber availability is a pinch point for the healthcare market and it is no different in online pharmacy. Most competitors who claim 24/7 are similarly bottlenecked at the prescribing stage-they just don’t disclose it. The Medpal FAQs are deliberately transparent. And will soon emphasise what IS available 24/7 (AI triage, support, monitoring) and be clear that prescribing sign-off is the only Mon–Fri element. Medpal’s AI support is a key differentiator and if combined with the app will truly give the patient/customer a fully covered experience. This use of virtual agents is at the front of current Health-tech discussions23

That 24/7 engagement combined with GLP-1 patients, who are inherently health-conscious and motivated since they are spending £200+/month on treatment, are actively tracking progress. These are exactly the users who will engage with the app’s AI monitoring, blood test upsells, and ongoing wellness features. The app is designed to be the engagement layer that turns a transactional GLP-1 prescription into a long-term clinical relationship with a much higher LTV. This is why the focus is on growing the GLP-1 cohort aggressively.

The contract with Care UK for 111 care homes benefits from becoming the designated dispenser when the care home GP selects you. Medpal didn’t fully appreciate the benefits of this when they took Universal out of administration. Switching on the existing relationships has been a big driver in the pharmacy items and has allowed for them to test drive the robotic model for scaling up.

A strong barometer of the opportunity is Barchester Healthcare that was bought by Welltower Inc. for £5.2bn in October 2025. A portfolio of 240-60 care homes and hospitals, 60k beds, £40m per month of prescription business previously covered by community pharmacies, who actually find that onerous. Picture the clinicians in a frenzy trying to fulfil these orders. After care is going to be limited never mind intra-day problem solving. If ever a situation lends itself to a robotic-AI solution. Medpal will be looking to aggressively onboard more care homes as they under-estimated the benefit of this and didn’t fully appreciate the efficiency of having large demand portals tied in on a regular basis plus potential data dump for AI

Supplying care homes averages 7.5 items per month per patient with Rx at 33% margin.

The NHS prescription market is £11.2bn18

Being in the NHS system leads to access to eMARS (the Medication Administration Record charts), the CRM for the Care Homes and also The Spine, the NHS PMR (Patient Medical Records) system. The key is being made the dispensing pharmacist...this leads to data and predictable revenue streams. A key breakthrough is being on the NHS weight loss list where there can be a 2-week delay. Fertile ground for MedPal to improve upon.

Both Swaffham and Runcorn have robotic dispensing infrastructure. The model treats them as separate P&L centres with their own cost structures, but operationally they function as a centralised network-prescriptions are routed to whichever hub has capacity and stock, with delivery logistics managed centrally.

Runcorn has the BD Rowa VMAX as the primary automated dispensing system, processing approximately 75% of items automatically (rising to 85% as we scale). Swaffham has a smaller robotic setup. The split in the model reflects the physical reality:

Medpal forecast that their Runcorn facility, which is the larger hub with 73 care homes currently, growing to 213 by FY28/29, handling c.33,000 items/month currently rising to 83,000+, roughly a 2.5x increase from current levels at that site alone. Swaffham starts smaller at 10 homes/300 beds currently but scales from 2,250 items/month to over 12,000 as new homes are onboarded. Both sites run at 7.5 items per bed per month with a £9.62 average item value. Note that these are forecasts and may not be achieved.

Showing that you have site level redundancy is a selling point to the large care home groups.

Swaffham previously handled 35k items at its peak but now has much more scale. Omnicell and Vmax robot. Has reduced costs 70% from the manual dispensing previously. GLP-1s from here and also Mon-Sun packs of meds for Care Homes which is £8.5-9m p.a. at current run rates.

The BD Rowa VMAX24 at Runcorn can handle substantially more throughput than current volumes, up to about 1m items per month now if needed. Prior to Medpal it was handling 125k pm at its peak.

They are currently processing c.33,000 items/month at Runcorn and their model scales this to 83,000+ by FY28/29- The 10x aggregate capacity refers to the combined network including Swaffham.

The forecasts include the necessary scaling within the existing infrastructure: labour adjustments (the dispensing mix moves from 75/25 automated/manual to 85/15 as the robots handle more), modest increases in despatch and warehouse staff, and the associated variable costs. No significant additional capital expenditure on robotics is required to hit the forecast numbers. If Medpal needs to go beyond the forecast’s upper range, the Runcorn facility has physical space for additional robot modules, and could activate Swaffham’s capacity more aggressively.

The BDV Rowa VMAX - pharmacy2u has two, Medpal has one, so they have the capability to scale like the largest player in the UK.

Medpal operates a small fleet of vans, all of which are owned, with some EVs in the fleet. Delivery costs are modelled at 3.5% of NHS prescription revenue, which is a variable cost line that scales with volume. In addition, Medpal uses third-party courier services for broader geographic reach, particularly for clinic/GLP-1 deliveries which go nationwide. The fleet primarily serves the care-home delivery routes in the Runcorn and Swaffham catchment areas.

Scaling is built into the model-as items grow; the delivery cost line grows proportionally. For care-home routes, adding vans is straightforward and incremental. For the clinic/private side, Medpal relies on APC their courier partner, so there’s no fleet constraint. The postage cost per clinic patient is modelled at £6.49 per despatch within the clinic unit economics.

Given the current potential fuel crisis will the delivery cost line be under pressure?

If fuel costs rise, there is scope for optimising routes. The care-home delivery model is inherently efficient: routes are fixed and predictable (same homes, same days), which is ideal for EV range planning. A fuel crisis would be manageable given the short-distance, route-optimised nature of care-home deliveries. For clinic/GLP-1 shipments, Medpal uses Royal Mail and courier partners, so fuel cost pass-through is handled through their pricing.

PharmacyX is a new PMR system that allows for sophisticated inventory tracking25 Access to eMars ensures that chronic meds have a 1month sight in advance. The robot works with the Cambrian Alliance26 for wholesalers to work out a line-by-line inventory need and processes at best price and volume

Inventory & Viral Drug Risk

The care-home pharmacy model is inherently predictable-Medpal knows exactly what each resident takes and can forecast demand with high accuracy through the eMARS system. Stock is replenished on a regular cycle from wholesalers (primarily Alliance Healthcare and AAH), with daily delivery windows available. There is no need to carry excessive safety stock because the demand profile is so stable.

For the clinic/GLP-1 side, this is where the direct supply agreements with Eli Lilly (Mounjaro) and Novo Nordisk (Wegovy) are critical. These give Medpal allocation certainty that competitors relying on wholesale channels don’t have. If a GLP-1 product went “viral” (which is effectively what’s been happening in the market), the direct supply relationships protect them from the stock-out issues that affected many online pharmacies in 2024/25. Inventory refill is not 24/7 but is on a frequent scheduled cycle-typically next-day for standard items and managed on allocation schedules for GLP-1 medications.

Medpal Ai PLC is dual listed:

On AIM: MPAL and on Frankfurt: Z1N (a market purported by Medpal’s advisers to be interested in health-tech investments)

MedPal is undertaking a placing of new shares to raise about GBP527,000 via a bookbuild process at the issue price of 2.5p brokered by Clear Capital Markets with proceeds intended for marketing spend and working cap New 21.08m shares to be issued27

A retail Raise up to 8m shares at 2.5p to be a WRAP Winterfloods’ retail raise on Friday through to Tuesday28

MedPal AI PLC - London-based digital health and AI company - Launches the MedPal weight loss blood test29, marking its entry into the at-home blood testing sector. The kit designed for users of GLP-1 medications. MedPal says the kit adds a third revenue stream alongside its AI wellness app and automated pharmacy operations at MedPal.clinic. Chief Executive Officer Jason Drummond says: "Blood testing is the missing layer in consumer health. By combining wearables, blood biomarkers, AI insights and pharmacy fulfilment in one ecosystem, we can now take users seamlessly from insight to diagnosis to treatment."

Signed an agreement with Pinpoint, a medical marketing agency, which begins in April and will look to position Medpal aggressively into the online dispensing market.

Frankfurt listing due to interest in tech and small cap with studies suggesting a good potential raise venue

Corporate structure Medpal AI plc with subsidiary Medpal Limited 100% owning the pharmacy business

Enhanced vertically integrated healthcare offering with the Universal Pharmacy purchase and licence renewal4

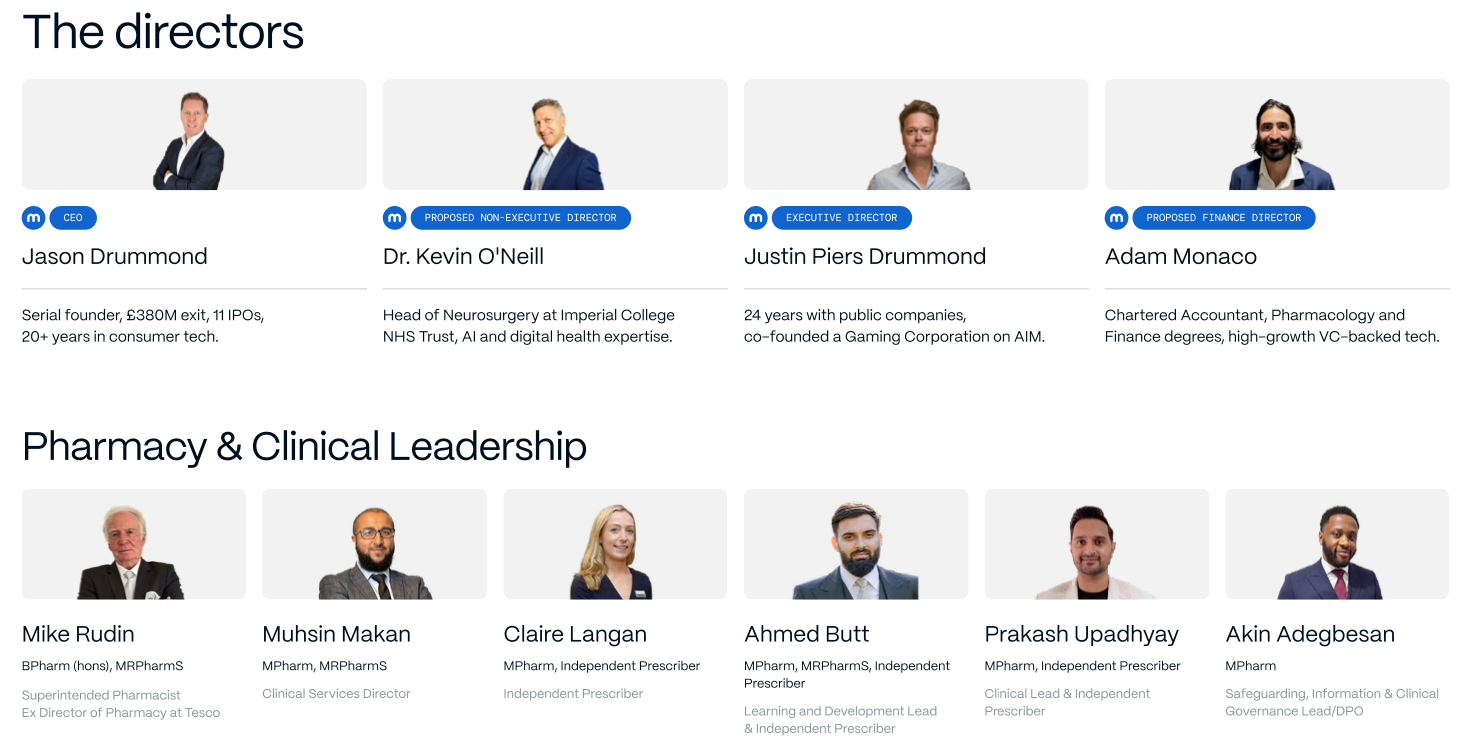

Mike Rudd Director of Pharmacy and has a history with distance selling pharmacy at Tesco.

2 supervisors

3 pharmacists

25 dispensing pharmacists

8 dispatch people

Overall, 90 employees which is representative of an operation ready for scale build-out and able to switch on the national delivery model.

The UK prescription weight loss medications market is currently influenced by several key factors. The prevalence of obesity and overweight individuals in the country is a significant driver, as data from March 2025 indicate that approximately 64% of adults in England are classified as overweight or obese, with 29% meeting the criteria for obesity (BMI ≥30 kg/m²)30.

What is needed for a GLP-1 prescription?31

In the UK, there are several licensed GLP-1 medicines including semaglutide (sold under the brand names Wegovy, Ozempic and Rybelsus), tirzepatide (Mounjaro) and liraglutide (sold under various brand names). “Licensed” means they have been assessed carefully by the UK medicines regulator, the Medicines and Healthcare products Regulatory Agency (MHRA), and approved as safe and effective for certain uses.

Injectables vs pills...temperature requirements, costs vary vs strength of drug...potential for a pill solution to power the next surge in volumes and change in customer profile

Hims/Hers drug issue. There is a work around for when supplies of drugs are in short supply in the US. A dispensing pharmacy can produce a compounded copycat to replace the missing drug. This is designed to be temporary in nature and not designed to negate copyright and patents legislature. Not surprisingly Novo Nordisk sued and the two companies settled with a large supply agreement.

Weight loss is a line that historically has been a loss leader in the first 4-5 months despite being an industry cash cow last year. The first injecting pen is sold at a loss with large discounting being used to entice patients into the subscription. It is already a £2bn market

The move into pill treatments over the injections will be much more efficient with no need for temperature control management and no pens. This should attract a whole new, larger demand from patients who generally lean towards oral medicines.

Source: Company deal deck39...this is an opinion of Medpal in terms of their market positioning. They appear to be the only company referencing AI-trained clinician support and are planning to be 85% robotic in dispensing as they expand as referenced in the facilities section above.

Medpal UK centric for now but rivals may be global by nature if they have the particular licences required.

Medpal mentioned on same page as three online pharmacies cited as being amongst fastest growing tech companies32:

Glasgow-based Phlo ranked 13th on the list, with sales of £23.1m in 2025 and a growth of 180.14% per year.

Norwich company Evaro, which ranked 29th, saw £12.1m in revenue last year and an annual growth of 109.72%.

And HeliosX, which has offices in Leamington Spa and at its US pharmacy in Florida, ranked 42nd. The company’s latest sales stand at £178.4m and its average annual growth was 88.36%...

Pharmacy2u is the UK’s largest online pharmacy serving over 1.8m patients a dispensing over 1.6m items each month33

HimsHers, Juniper, PHLO and Numan major players in (GLP-1s)

An interesting angle is Vulcan Two who recently IPO’d and have a stated objective of creating the UK’s leading regulated ePharmacy through buy-and-build34. Their Directors believe there is a compelling opportunity for growth and consolidation which exists in the fragmented private prescription sector of the regulated UK ePharmacy market, one of the fastest growing and most profitable sectors of the market. They are capitalised at £60m with a number of institutional investors. It will be of interest how they seek to further acquire in this segment but illustrates that Medpal is in a sector which could suddenly see them attract a bid premium or valuation readthrough in the near future. In March 2026 they acquired three UK ePharmacies:

CloudRx, Hyperdrug and Webmed

Competitor Discounting (Numan et al.)

The discount-led competitors like Numan are buying market share at unsustainable margins. A race to the bottom on GLP-1 pricing is a losing game because the drug cost is the drug cost-there’s very little margin to play with when Mounjaro costs c.£199/4 weeks at wholesale. Competitors discounting heavily are either cross-subsidising from other product lines, operating at a loss to build scale, or cutting corners on clinical governance.

Medpal has positioned itself expecting that this market will consolidate around operators who can demonstrate:

(a) sustainable unit economics

(b) genuine clinical credibility (NHS contracts, GPhC premises licences, direct manufacturer supply)

(c) differentiated service beyond just dispensing a prescription.

The competition who are gym-discount bundlers are marketing plays, not genuine healthcare businesses.

Most competitors who claim next-day turnaround are measuring from prescribing approval, not from initial consultation. Medpal gives a 3-day end-to-end expectation to be realistic but can execute within that timeline if review is performed quickly.

The timeline breakdown is as follows:

Medpal is almost the only listed UK player with the full chain from app to robotic delivery35

Clinic Income streams all the consumer deliverables that rivals provide

Erectile dysfunction

Hair Loss

Chronic disease management prescriptions

GLP-1s are prescription only. Of which 1.4m were online and 200k via NHS and predominantly diabetes16. The weight loss angle whether pre-diabetes or lifestyle change is likely the key area for growth in Medpal’s numbers. They are generally repeat customers who pay for a long cycle that they may jump off after success but end up returning to. The key going forward is customer retention and repeat orders.

Blood testing kits29– Not only good margin but produces data and app engagement with a captive market source of people who most likely require some medication dispensing in the near future. Provides for ideal AI learning sources. The start of a Bio-marker section...

Blood test kits are not currently modelled within the forecasts-they represent pure upside to the numbers you’re looking at. The plan is to offer them as both an upsell to weight-loss patients (pre-treatment baseline bloods, ongoing monitoring) and as a standalone offering via medpal.clinic for the broader wellness market. The unit economics are attractive; they strengthen the clinical proposition for GLP-1 patients and provide a gateway for app users into paid clinical services. Initial uptake will be driven by existing clinic patients with a broader D2C push once the fulfilment workflow is proven. We will add blood tests as a discrete revenue line in the model once we have 60–90 days of live data, but for now the forecasts are conservative in that they exclude this entirely.” Jason Drummond CEO

The key message is going from launch to scale in 12 months and really that is enhanced by the Universal purchase and build out in November

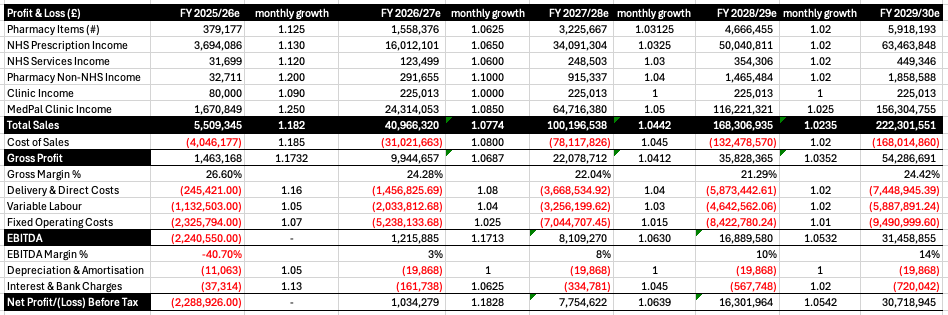

Working with the company on a conservative FY Aug26 forecast given the excellent November to Feb 26 update5. I have then built out based on the monthly growth rates for revenues and costs. There is a stated focus on GLP-1 / Clinic income and that has 25% mom growth rate in FY27. Along with most other lines there is a linear run off into FY Aug30 reflecting the slowing down of still a high revenue growth model. This doesn’t include any app revenues as these sit in the plc and I am forecasting for the Medpal pharmacy business which is in the wholly owned Medpal Ltd subsidiary.

The expectations are for Medpal Clinic revenues to grow significantly in weight-loss but also new consumer care / chronic illness lines as well as the blood Test / bio-marker segments the latter of which is not included in the forecasts but could allow for the detection of treatable diseases which at least results in the numbers forecast. Equally there is no allowance for wholesale discounts which Medpal’s suppliers should provide if they start to hit these forecast numbers, and see a material boost to the gross profit line.

Marketing opportunity in online pharma generally requires 2-5% of revenues per month to optimise. Most of the growth so far has come from onboarding the existing Care Home portfolio and Universal patients which is the low-hanging fruit that provides the stable revenue base.

The next phase is the clinic-led growth, which is where the marketing spend ramps significantly: Medpal forecasts that this rises from £81k (10-15% Revs) in March 2026 to £222k/month (5% avg monthly FY2027 Revs) by August 2026, reaching £269k/month by December 2026 (6% Revs adjusting for revenue scaling). The blended CAC should drop from £242 in the first month to £120–130 as campaigns optimise as volumes take effect. These are forecasts and are subject to Medpal performance in delivering the numbers cited.

Google Ads and paid search campaigns are only just ramping up with the Senior Director of Marketing and a £4M+ 18month marketing budget is primarily performance marketing (Google Ads, Meta) to drive direct patient acquisition, not organic Search-Engine-Optimisation, that will build over time. Medpal have also signed a contract with Pinpoint Media36 a paid media agency to enhance their campaigns.

FY25/26 (year to August 2026) is a bedding-in year. Consolidated revenue for the full FY is modelled at c.£5.6m in discussions with Medpal, of which pharmacy contributes c.£3.7M in NHS Rx income. This reflects the reality that Medpal acquired the Remedi infrastructure, had to complete the change-of-ownership process with GPhC, and needed to stabilise operations before aggressively scaling. GPhC licence applications have taken longer than anticipated.

The sharp ramp in FY26/27 (£40.9M) and FY27/28 (£100.2M) is driven overwhelmingly by the clinic/weight-loss revenue scaling from the cohort model. The pharmacy side grows more steadily with NHS Rx income forecasted to grow from £3.7M to £16M to £34M as care homes are added at 15–20 per month at Runcorn and 2–4 per month at Swaffham.

The outer-year growth rates are ambitious but are built bottom-up from the cohort model: each month’s new patient intake (growing from 333 in March 2026 to c.2,400/month by mid-2027), layered with the retention curve (declining from 100% at Month 1 to 35% by Month 12), drives cumulative active patients to an average of c.7,800 in FY26/27 and c.16,600 in FY27/28. These numbers depend primarily on marketing spend efficiency and ability to convert at the modelled CAC.

Costs not benefiting from scale partner discounts yet

Cashflows as a start up in the wholesale medical market is a challenge as you are paying up front on account but Cashflows are smoothed by the NHS paying on the 10th of the month for that month’s drugs as the CRM systems give you one month of predicted patient drug demand.

Low inventory model with just in time supply control

£10 per Rx prescription at 30% margins...prescription with fixed fee...margin based on fixed drug price paid by NHS and the ability to source from wholesalers

Revenue protection element as medically prescribed drugs cannot be returned

NHS prescription market £11.2bn18

Operational update for 4months from Nov 147k prescription items; £1.5m revenue implying £10 per item and a 33% average gross margin. February was running at 32,637 items5

Handling 35k items per month and have scale for 300-500k per month that makes the forecasted growth numbers realistic without further investment in equipment.

Clinic income also includes NHS Services where MPAL are paid to go into care homes and administer flu jabs or do ear wax removal or other “nice” care home treatments. They make c £30 per visit.

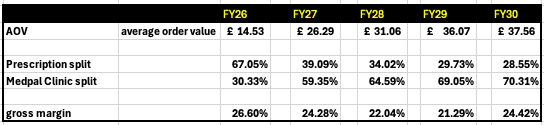

Rx Volume Drives AOV should rise yoy particularly if higher value mix

You can potentially see this modelled in the table above with AOV rising each year as prescription to Medpal Clinic split inverts

High prescription adherence means more predictable, larger basket sizes month over month.

AOV will rise because chronic condition patients order refills consistently.

A focus on capturing 90%+ of the patient’s total medication spend will solve a lot of issues.

Key to knowing your pricing strategy is profitable at its core product level before overheads, drives cash flow available to grow. Higher margin OTC products and other lines like blood testing kits should help the mix later. The key is volume discounts from wholesalers

OTC sales often carry 40% to 60% gross margins; prescriptions are usually lower but still a significant 33%. The clinic revenues are currently at 10-12% margin which needs to grow to bring the gross margin back into the overall 30%+ sweet spot.

You need OTC sales to act as a margin ballast against lower prescription profitability.

The consolidated gross margin moves from c.34% in the actuals period to Feb26 down to c. 26% in FY25/26 and remains depressed in the 21-24% range in the outer years due to a mix effect driven by the rapid growth of the lower-margin GLP-1 weight-loss clinic revenue as a proportion of total sales. There is no deterioration in the pharmacy economics. What pulls the blended margin down is the sheer scale of clinic revenue growth: from £2.4M in FY25/26 to over £103M by FY28/29. As GLP-1 becomes the dominant revenue line, its lower gross margin increasingly drives the consolidated number.

Importantly, the model is deliberately conservative on clinic margin. The drug cost of sales is based on the current buy price/patient/4 weeks for Mounjaro and Wegovy which sees a clinic gross margin of only 12–13% for Month 1 patients, settling around 18–20% as the cohort matures. As Medpal builds volume the direct supply agreements with Eli Lilly and Novo Nordisk should see better terms. Any improvement in the drug buy price drops straight to gross profit and would materially lift the blended group margin. This is deliberate conservatism in the model-the margin upside from volume-based procurement is entirely unmodelled.

Medpal suggest their income is £1,519 per patient per annum figure which comes directly from the clinic unit economics model-it’s the weighted revenue per active weight-loss patient per year, based on the retention curve (average 6.97 weighted months of activity across a 12-month cohort) at an average revenue per active patient of £128–260/month depending on tenure and Mounjaro/Wegovy mix. After cost of sales (£1,305) this provides for a CLV of £214

CAC is Customer Acquisition cost and is the total money spent on marketing and sales to bring in one new customer and you want it low relative to Lifetime Value which itself depends on Repeat Customer Rate. Bundling opportunities and incentives help. High service levels and AI engagement should drive the RCR and avoid bad word of mouth outcomes.

The blended CAC in the model starts at £242 and drops to c.£121 as campaigns mature. So, the economics are: spend £121–242 to acquire a patient. Which gives a CLV/CAC range of 0.88 – 1.77...Ideally this needs to move up to 3:1 or above so needs total spend to increase and/or repeat months to go up too. This should happen as scale occurs

Medpal EV/Revenue multiple of between 6-8x for the 1Y forward period37

“Dominance of AI and Digital Health: AI is the single biggest driver of valuation premiums. Investors and strategic buyers are focusing on companies with proprietary AI algorithms for diagnostics, drug discovery, or patient care. They are particularly interested in solutions that have been clinically validated and are deeply integrated into existing clinical workflows, creating "workflow lock-in."” Nelson Advisers

Medpal are expected to be breakeven to net profitable around FY27 if our forecasts are met. The table below is supportive for our price target, using the multiple ranges referenced above, but assumes the forecasts are forthcoming. There is no guarantee these numbers will be hit, as these are considerable marketing execution risks, but given the company has budgeted for £4m of marketing budget for the next 18 months they should be pretty close.

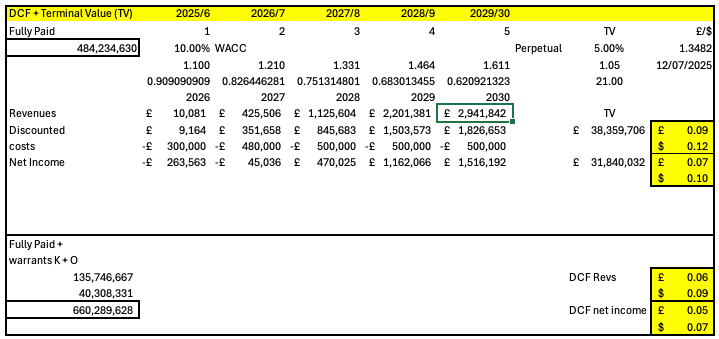

Alternatively, we can look at a DCF which includes very conservative app revenues and costs of £25k per month marketing costs which grow to £30k+ as most of the spend will be on promoting the medpal.clinic and WhatsApp routes which will by definition look to direct downloads of the app anyway.

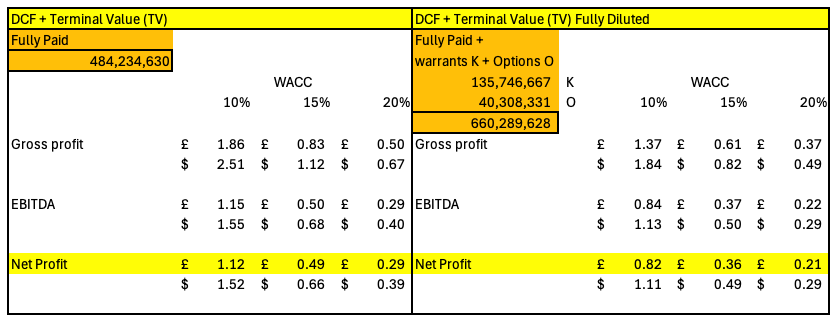

The value of the potential app revenues after costs on a fully diluted basis could be worth up to 5p of value at a 10% wacc. However, we need to be probabilistic over online AI and the risks of GLP-1 type earnings. The table below shows the plc combined app and online pharmacy DCF values for Gross profit, EBITDA and Net Profit for WACC rates of 10,15 and 20% on both a fully paid and a fully diluted basis.

That provides for a range of value from 21p to 112p on a net profit basis. The effective wacc rate should de-risk over time as Medpal becomes cash generative and reaches its scaling milestones. I believe it is fair to consider an 18-month price target to allow for the full effects of the marketing spend at a conservative level of 30p. This is considerable upside from the current pricing and placing levels with significant further upside should the metrics de-risk and even outperform.

Medpal suggest they are doing for medicine what Amazon did for retail39. They have converted their warehouses from manual to high end robotics with a 99.99% accuracy rate39 . If you look at the efficiency of the process you could say they are doing it better. The logistic engine required to provide tens of thousands of critical meds, with almost zero % error rate and processed within a 24/7 schedule, is very sophisticated.

They have moved from promise to practice and are not hanging around.

The USP versus the pure-play online GLP-1 providers is the vertically integrated clinical model:

(1) Medpal is a real pharmacy with NHS contracts, robotic dispensing infrastructure, and GPhC premises licences, not a prescribing platform that outsources fulfilment.

(2) AI-powered 24/7 clinical triage via WhatsApp providing genuine ongoing support, not just a prescription mill.

(3) direct supply agreements with Eli Lilly and Novo Nordisk giving stock certainty.

(4) the app-based monitoring and blood-test ecosystem that turns a 12-month prescription into a long-term health relationship. The holistic model is the differentiator-competitors are either cheap and transactional or expensive and clinical. Medpal sits in the middle with technology-enabled scale at a clinical-grade service level.

The counter to AI disruption is the barrier to entry...AI is not clinically regulated the human clinician is, and in the UK MEDPAL has one of the last licences for online selling.

We have valued Medpal AI PLC on a sophisticated digital AI player basis. Their business moat and tech should demand a premium rating. The DCF models allow for deep discounting and for a range as the wacc de-risks to towards 10% to give you a feel for how the current metrics could provide material upside value.

Medpal are holding back on including app revenues and blood testing for now in their forecasts and are not factoring in bulk pricing discounts until, if and when, they are secured. Whilst there is risk that the GLP-1 penetration doesn’t occur at the forecast speed they are set up to scale and quickly. There is enough low hanging fruit in the care home segment and marketing is set to explode from a low base. The weight loss market in the UK is still under patent and new drugs may enter at a lower value point. Given that it is a lower margin product currently this could change with a volume surge at better margin and still remain relatively high value revenues within the model.

Cross selling within the ecosystem and maximising recurring, repeat patients will be key to improving their KPIs and really re-rating

Medpal is about to become noisy with a marketing push; they have quietly scaled for a large and quick build out particularly in care homes and weight loss; the sector is already consolidating with institutional investment eyes on it and committing capital. Medpal is trading at its lowest valuation post IPO and appears to have been oversold rather than reflecting its fundamentals. It would seem likely that Medpal could begin to make some material share price progress as the market digests that it is actually delivering real growth and revenues and is in the upper quadrant for its Ai and robotic mix versus competition.

New entrants to UK ePharmacy will have to go the Vulcan route...a famous one would probably say “it is not logical to ignore Medpal...live long and prosper!”

Note 1 MedPal.AI Company website https://www.medpal.ai/

Note 2 medpal.clinic Medpal clinic web portal and WhatsApp link https://medpal.clinic/

Note 3 medpalplc.com investor website https://www.medpalplc.com/

Note 4 https://www.londonstockexchange.com/news-article/MPAL/completion-of-acquisition/17461785

londonstockexchange.com news-article MPAL completion of acquisition 16th Feb 2026

Note 5 https://www.londonstockexchange.com/news-article/MPAL/pharmacy-operational-update/17504651

londonstockexchange.com news-article MPAL pharmacy-operational-update 16th March 2025

Note 6 https://www.anthropic.com/news/healthcare-life-sciences

Anthropic.com news healthcare-life-sciences 11th Jan 2026

Note 7 https://www.healthcaredive.com/news/40-million-use-chatgpt-health-questions-openai/808861/

Healthcaredive.com / news / 40 million use chatgpt health questions openai / 808861 6th Jan 2026

Note 8 https://www.bbc.co.uk/programmes/m002r9c3

Bbc.co.uk / programmes / m002r9c3 or search The assassin and the algorithm??

Note 9 https://www.londonstockexchange.com/news-article/MPAL/eli-lilly-supply-agreement/17433632

londonstockexchange.com news-article MPAL / eli-lilly supply agreement / 17433632 28th Jan 2026

Note 10 https://www.pharmacy.biz/semaglutide-patent-expiry-india-generics/

Pharmacy.biz / semaglutide patenet expiry india generics 20th March 2026

Note 11 https://openclaw.ai/

Openclaw.ai website

Techtarget.com / searchhealthit / news/ 366639165 / Athenahealthexpands Ai driven patient engagement capabilities 18th Feb 2026

Note 13 https://www.fortunebusinessinsights.com/industry-reports/digital-health-market-100227

Fortunebusinessinsights.com / industry reports / digital health market 100227 9th March 2026

Bmmagazine.co.uk / business / digital health expansion online pharmacies and the rise of mounjaro

May 26th 2025

Researchandmarkets.com / reports / 6216592 / uk prescription weight loss medications market

December 2025

Institute.global / insights / public services / anti-obesity medications faster broader access can drive health and wealth in the uk 20th May 2025

nesta.org.uk/data-visualisation-and-interactive/silver-bullet-or-sticking-plaster-weight-loss-drugs-and-the-uks-obesity-crisis/ 8th October 2025

Note 18 https://www.rehabmypatient.com/medications/how-the-nhs-prescription-budget-changed-over-the-last-decade-2015-2025 2nd July 2025

grandviewresearch.com/horizon/outlook/glp-1-agonists-weight-loss-drugs-market/uk 2026

Note 20 https://cpe.org.uk/our-news/contract-changes-dsp-regulatory-faqs/

cpe.org.uk/our-news/contract-changes-dsp-regulatory-faqs/ 4th April 2025

Note 21 https://pmc.ncbi.nlm.nih.gov/articles/PMC11934860/

pmc.ncbi.nlm.nih.gov/articles/PMC11934860/ 24th Feb 2025

Note 22 https://sprintlaw.co.uk/articles/are-online-pharmacies-legal/

sprintlaw.co.uk/articles/are-online-pharmacies-legal/ 18th Dec 2025

Note 23 https://www.healthcare-brew.com/stories/how-healthcare-uses-virtual-agents-and-chatbots

healthcare-brew.com/stories/how-healthcare-uses-virtual-agents-and-chatbots 25th Feb 2026

Note 24 https://www.youtube.com/watch?v=ejn5jINmBUw

youtube.com/watch?v=ejn5jINmBUw BD Rowa Vmax 160 Función Dispensar 3 years ago

Note 25 https://pharmacyx.com/ pharmacyx.com website

Note 26 https://cambrianalliance.co.uk/ cambrianalliance.co.uk website

Note 27 https://www.londonstockexchange.com/news-article/MPAL/placing-and-wrap-retail-offer/17513581

londonstockexchange.com news-article MPAL / placing and wrap retail offer / 17513581 20th Mar 2026

Note 28 https://www.londonstockexchange.com/news-article/MPAL/wrap-retail-offer/17513630

londonstockexchange.com news-article MPAL / wrap retail offer / 17513630 20th Mar 2026

londonstockexchange.com news-article MPAL / medpal enters at home blood testing market / 17512539

20th Mar 2026

grandviewresearch.com/industry-analysis/uk-prescription-weight-loss-medications-market-report 2026

gov.uk/government/publications/glp-1-medicines-for-weight-loss-and-diabetes-what-you-need-to-know/glp-1-medicines-for-weight-loss-and-diabetes-what-you-need-to-know website

Note 32 https://www.chemistanddruggist.co.uk/news/business/online-pharmacies-among-uks-fastest-growing-tech-companies-L46SCB7FMRBHJPIMRBYUR4W3F4/#:~:text=Glasgow%2Dbased%20Phlo%20ranked%2013th,an%20annual%20growth%20of%20109.72%25 chemistanddruggist.co.uk/news/business/online-pharmacies-among-uks-fastest-growing-tech-companies-L46SCB7FMRBHJPIMRBYUR4W3F4 21st Jan 2026

Note 33 https://www.pharmacy2u.co.uk/about pharmacy2u.co.uk/about website

Note 34 https://vulcantwo.com/about-us vulcantwo.com/about-us website

Note 35 https://www.londonstockexchange.com/news-article/MPAL/medpal-app-ai-integration-with-medpal-clinic/17403755 londonstockexchange.com news-article MPAL / medpal-app-ai-integration-with-medpal-clinic/17403755 8th Jan 2026

Note 36 https://pinpoint-media.global/ pinpoint-media.global website

Note 37 https://nelsonadvisors.co.uk/blog/european-medtech-valuation-multiples---september-2025

nelsonadvisors.co.uk/blog/european-medtech-valuation-multiples---september-2025

16th September 2025

Note 38 https://www.healthcare-management.uk/pharmacies-lost-decade

healthcare-management.uk / pharmacies lost decade 22nd April 2025

Note 39 https://www.medpalplc.com/research

Note 40 https://www.statista.com/topics/2409/digital-health/

Statista.com / topics / 2409 / digital-health 17th Dec 2025

Note 41 https://themodems.com/tech/wearable-tech-is-the-uks-biggest-wellness-trend/

Themodems.com / tech / wearable tech is the uks biggest wellness trend 16th Feb 2025

Note 42 https://onlinedoctor.asda.com/uk/nhs-weight-loss-injections.html

Onlinedoctor.asda.com / uk / nhs weight loss injections 23rd June 2025

Nothing in the above article should be considered investment advice.

Small Cap or Aquis listed companies can be highly illiquid making them difficult to sell at the quoted price, and in some cases, it may be difficult to sell them at any price. Small Cap or Aquis listed companies can have a large bid / offer spread which means there could be a large difference between the buying and selling price. Companies listed on the Aquis market can be highly volatile and are considered high risk speculative investments. The value of your investment can go down as well as up, your Capital is at risk you may not get back the amount invested. Past performance is no guarantee of future performance. Investments in IPO’s & RTO’s involve a high degree of risk and are not suitable for all investors. All investments made into an IPO, RTO in a secondary issue should always be made solely based on the information provided in the relevant prospectus and any other supplementary documentation. Please ensure that you fully understand the risks involved. If in any doubt, please seek independent financial advice. This document is published by Clear Capital Markets and does not constitute a solicitation or personal recommendation for the purchase or sale of investment. The investments referred to may not be suitable for all investors. Any data or views given should not be construed as investment advice. Every effort is made to ensure the accuracy of the information, but no assurance or warranties are given. Clear Capital Markets Limited is authorised and regulated by the Financial Conduct Authority FRN 706689.

Clear Capital Markets Corporate Broking acts as a Corporate Broker to MedPal AI Plc and holds warrants and shares in the company. Employees and/or directors of Clear Capital Markets may deal in shares of MedPal AI Plc for their own personal accounts. These scenarios may give rise to a conflict of interest where Clear Capital Markets also provides clients with an advisory service for transactions involving MedPal AI Plc. The firm has established Conflicts of Interest (“COI”) and Personal Account Dealing (“PAD”) policies to mitigate the risk of a conflict causing damage to the interests of its clients. The measures taken include (i) enforcing minimum holding or ‘lock-in’ periods; and (ii) requiring internal review and approval from the compliance department for employees or directors entering into personal transactions involving MedPal AI Plc. The COI and PAD policies are available upon request. Before Clear Capital Markets proceeds with a placing, a number of factors are considered including: liquidity of stock, company diversification, market capitalisation and potential news flow. Only once minimum criteria are satisfied would we elect to proceed. Any remuneration payable to Clear Capital Markets has no bearing on whether it proceeds with a placing. These administrative controls mitigate the risk of a conflict causing damage to the interest of a client, but the inherent risks of this business model cannot be eliminated. Accordingly, Clear Capital Markets is required to disclose this conflict to help clients to assess the service that they are being offered in light of Clear Capital’s own interests, and to decide on the extent (if at all) to which they will rely on, or proceed with, the service.

We will reach out for a quick introductory fact find to see how we can best serve your specific needs and arrange a convenient time for a consultation with a member of the appropriate specialist team.

An Advisory Broker will contact you for a deeper fact find and share information on how we can best enhance your portfolio.

We will process your application in accordance with FCA regulations to ensure that your appropriate risk profile is set. You will then have access to an extensive suite of investments, supported by your dedicated Advisory Broker.