Promotion: Capital invested is at risk. Non-Independent Research / Marketing Communication. Attention is drawn to the disclaimers and risk warnings within this document.

BROKER NOTE BY JONATHAN PLANT

6th October 2025

.png)

Another attractive Richmond Hill destination in Ontario...

An entry level junior explorer with an interesting, mineralised project, focused on copper, in a Tier 1 jurisdiction in Ontario, Canada.

It has been a transformational journey for Rogue Baron Plc moving from smelling and tasting the benefits of a copper-still, sulphide removal, whiskey making process through the metamorphosis into Richmond Hill Resources (RHR)4a which is hoping to still find sulphides of copper.

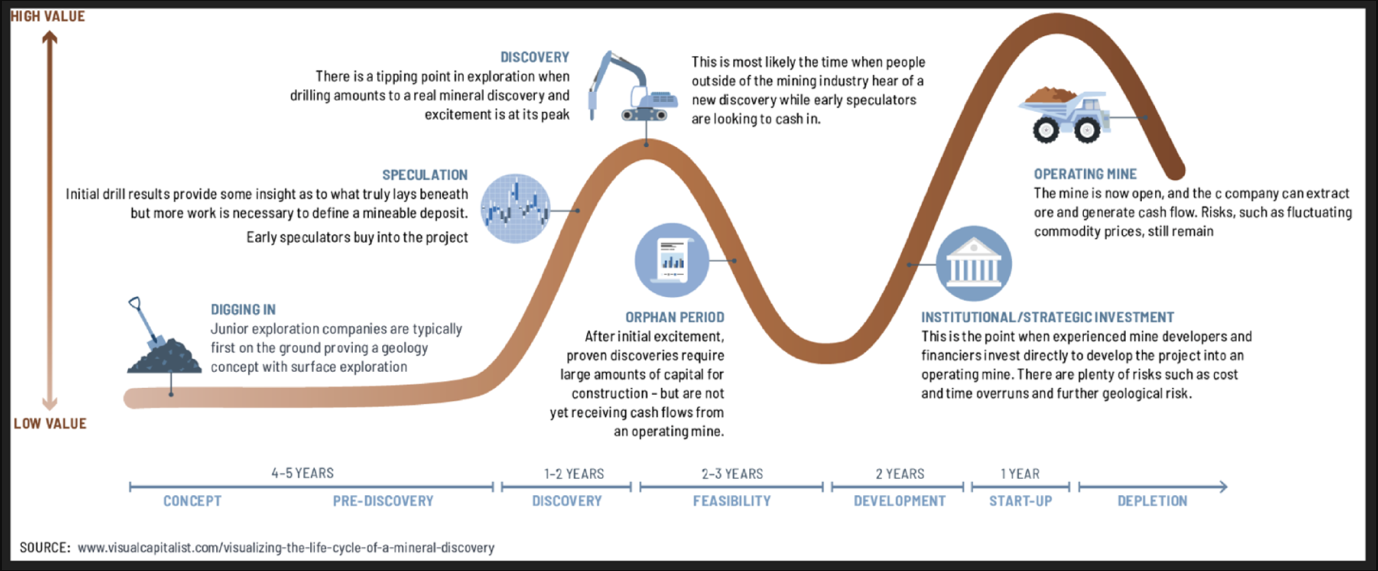

The mining sector is suddenly in vogue again. Gold, silver, platinum, uranium and copper particularly are all benefitting from Supercycle features again. We will look at the macro backdrop and the recent M&A potential into the copper sector which are providing a potential sweet spot backdrop for a copper play. Consideration to where RHR is on the micro-cycle, with a nod to the Lassonde curve, will be given.

RHR has a Strong management1 p18-19, with natural resource focus and a recent history in adding value in the sector and at pre-discovery level. This combination highlights an industry insider knowledge of quality projects at the wrong price, which by itself could lead to value normalisation upside, regardless of success at the exploration stage. Our focus will remain on the anomalous nature of RHR’s project in Quebec and the immediate processes which could push the project along the Company’s aim of resource improvement.

We will review the Saint-Sophie project with an emphasis on its mineralisation highlighting where and how this can move from confirmation of data to improvement of data. RHR doesn’t even need to reach major drilling stage to potentially create shareholder value with a sector rating likely post-listing.

Exploration at surface level and digging in leads to higher certainty of significant mineralisation. These are the early stages of exploration and there can be material uplift in project value as the grade improves and drill holes define where the deposits are and how they are structured. From here you can use techniques to create triangular prisms to estimate tonnage and confirmation of density of the ores measured leads to volume estimates of an inferred nature and a core value of the resources estimated. The steepness of the deposit find will determine drilling requirements and with copper you are hoping for that steepness to indicate how and where the copper-bearing fluids have formed in the sulphide strata. With something like Saint-Sophie where most of the exploration has been at surface level and low depths there is potential for the cheaper low depth mining to provide cash flow for continuing the exploration down to the main deposits if they exist.

The whole speculation stage is about travelling along the resource curve of inferred to indicated to measured before entering into the sphere of proven and probable reserves. All effectively bus stops on the journey. As the resource grows towards a potential mining operation economic feasibility reports will have to consider the infrastructure potential of the plot. Can it support the size of project, does it have water supply, easily accessible roads. Are there any ESG issues relating to sustainability of the environment, cost of cleaning up, permissions required from First Nation in Canada.

As junior companies progress they need funding. That may be debt if the potential early stage cashflows are supportive but mostly will be equity or convertible notes both of which have dilution potential. As we will show in the valuation section this isn’t necessarily a negative. Indeed, there are some recent examples such as White Cliff Minerals of raising money at a premium10a because the finds are so value accretive. A potential investor should be aware of the game going in. You don’t need to reach the mining stage of the curve to potentially make significant returns. Early involvement along the pre-discovery/speculation border can see some of the larger percentage gains relative to the later more mature institutional stage but you must be aware that each stage has higher probability than the previous of success but never quite extinguishing the risk of failure. The reserves may ultimately be too costly to extract for instance. The pace of discovery may be delayed and require extra cash flow funding. This is often where many juniors have received criticism with zealot type managements perceived to be using the investors as a discovery bank. RHR are upfront about their ambitions to be a probabilistic miner. That should extend to them being realistic about future success potential. In the meantime, as we will show below, they have a project which has all the elements in place for early project uplift and any material discoveries could see them valued alongside successful peer metrics.

Two data sources are worthy of our focus. The RNS detailing the reverse takeover and the technical report of IOS Geosciences based on a site visit in Dec24, previous data provided by RHR and an interrogation of the Quebec Government’s online claim management and assessment work databases (GESTIM and SIGEOM, respectively).

Taking the Schedule One document3 first:

The Company entered into an agreement with Ulvestone Limited ("Ulvestone") to acquire the entire issued share capital of Bulawayo CC Ventures Limited ("Bulawayo") for a consideration of £3,300,000 to be satisfied through the issue of 315,000,000 Ordinary Shares and £150,000 in cash.

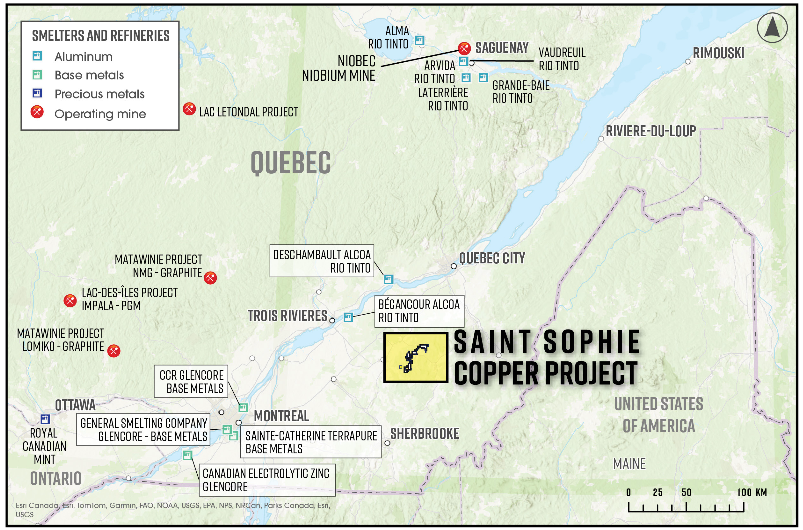

Bulawayo is the owner of the Saint-Sophie project (the "Project") consisting of 145 map designated mineral exploration titles covering a total surface area of approximately 87 km2 (8700 ha) located in the Centre-du-Québec region, approximately 165 km east of Montreal and 80 km southwest of Quebec City in Canada, within a region known for copper mineralisation.

On Admission, Richmond Hill (through Bulawayo) will hold 145 map designated mineral exploration titles covering the Centre-du-Québec region. The region lies within the Appalachian mountain belt, featuring Cambro-Ordovician sedimentary and volcanic rocks (Humber Zone) known to host copper mineralisation. The claims to the titles were acquired by several individuals and companies through map designation and are currently owned by Bulawayo. There is a 1% Net Smelter Return (NSR) on all mineral production from the Project owed to 1426706 BC Ltd.

From Admission, the Company's strategy is the development of the Project. The Company believes the Project area is anomalous in copper. The copper occurrences located on the Sainte-Sophie property have not yet been explored with modern technologies and work to date has been mostly limited to trenching and soil surveys. Drilling is sparse and has not reached beyond 61 metres in depth. The Sainte-Sophie property remains an interesting area for copper and other commodities such as silver and molybdenum. Furthermore, the Company may invest in and/or acquire further complementary mineral targets and resources.

Ulvestone is a name change/new owner vehicle relative to Three Mile Beach Ltd that was quoted in previous RNS announcements4 but has the same 100% beneficial owner James Ikin.

A NSR of 1% is now present on the property titles which was not known at the time of the report. This is actually a positive since it actually infers that the current holders anticipate upside and is inconsequential for RHR relative to positive movements. In fact, since these NSR agreements usually have a buyback determined it is a future value realisation point for investors to consider should RHR trigger that buyback.

The 1689-2024 Independent Technical report by IOS Geosciences1/1a/1bprovides the backdrop in resume form to the content of the Schedule One above.

The Sainte-Sophie property was visited on December 3rd 2024 by Hugues Longuépée, P.Geo., Ph.D. and Thomas Foulon, G.I.T, M.Sc. Unfortunately, the visit was inconclusive because of fresh snow cover. Time was spent at the Halifax, Megantic Copper and Poulin Option. The report was written on the 25th Feb 2025.

Without recreating the whole report, we will highlight (direct quotes in italics) what the salient parts are and provide inputs for the SWOT analysis shown in the valuation section below.

IOS were engaged by RHR to produce this report, written in line with National Instrument NI 43-101 and CIM guidelines, and obliged to construct an 18month exploration plan. Given the constraints of the weather and the largely historical data there are no resource estimates included so this by definition places us within that pre-discovery part of the Lassonde Curve but one with a decent roadmap of mineralisation.

The admission document1 rns has “extracts” of the full report but not all of the specific maps and graphics we have seen. Since IOS has warned of the scope of their report and how it allows for risks associated with third party data, we are also relying on that but include the extra charts referenced note1a as they give a full and fair view of what some parts of the project look like rather than just those in the admission document1/1b and it is our opinion that gives the potential investor an even clearer and transparent view of the project.

The Appalachian mountains are known for high mineralisation and you can see from the map above the extent of major mining infrastructure.

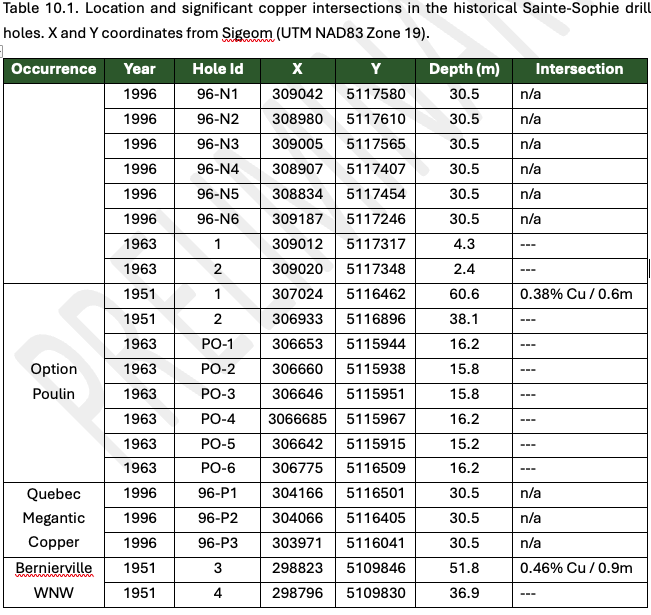

Saint-Sophie itself sits in the Cambro-ordovician Humber zone which is dominated by rift and passive margin sediments with occasional mafic volcanics. The area has been explored since the mid 1800’s and several artisanal mines (without declared resources or reserves) were exploited at the end of the 19th century. Despite its long history, only 26 drill holes, none deeper than 61 metres, are scattered on four of the fifteen copper occurrences found on the property1b p65.

“Copper is often associated with silver, gold, zinc, lead, molybdenum, nickel, chromium and/or manganese depending on how the formation has occurred. Antimony, (which is seen as a critical mineral and is a factor in the China US tensions), is also associated with copper in distant, but similar looking, copper occurrences in the Quebec Appalachians.

Overall, the mineralization type is poorly understood, but the currently accepted model is leaching of copper from volcanics and precipitation of copper sulphides in vein and hosting reactive sedimentary rock. Late supergene enrichment led to local copper concentration up of 32% Cu. “

This is something which RHR can readily address. There is a need to understand what is actually there, and how it has formed, which can then direct resource allocation effectively.

The area used to be a mining hub for asbestos mining until the mid-1980s but little further exploration has occurred since then. Copper is now facing a supply deficit and perhaps was not seen as something worthy of further investigation. There are a number of maple groves around the project and this is a protected industry. You literally cannot see the wood for the listed, individually Identified, trees. This may have put explorers off in the past but is not an insurmountable hurdle.

Despite the historic and limited nature of the studies of the project there is enough encouraging data (summarised in the graphic above) to warrant further exploration1a.

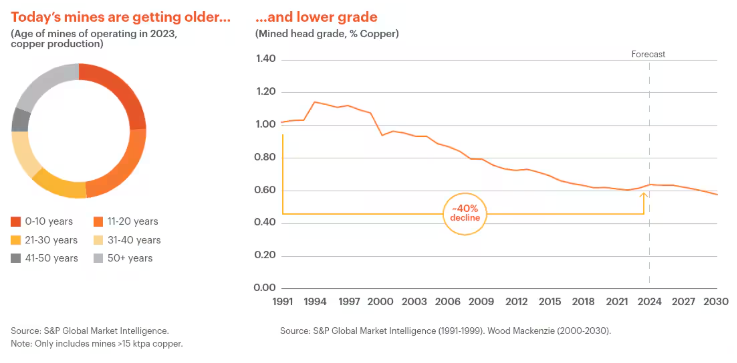

As we move into global copper supply deficit the lack of higher grade is also a factor. Average grades have fallen below 1% Cu and have fallen by 40% since 1991 on average5.

A lot of this is down to improved technology extracting lower grades after exhausting higher grades earlier in the life of the mine. You can also see from the profile of mine life that over 50% are older than 20 years which is dragging the grade available down.

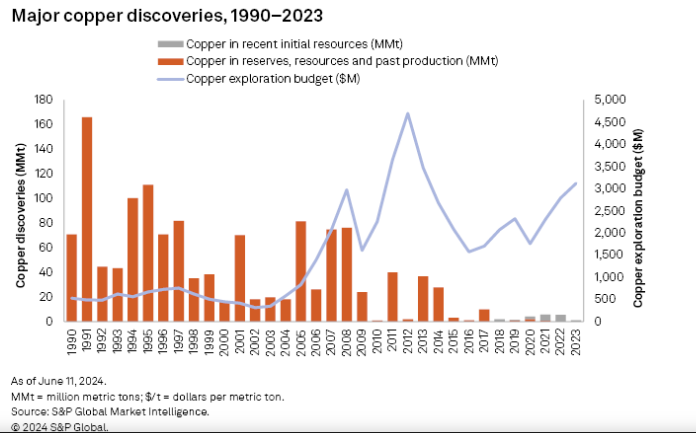

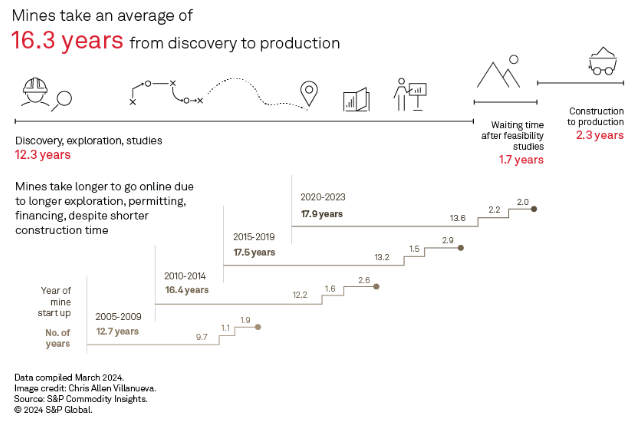

The trend of declining major new copper discoveries continued in 2023. Discoveries from the past decade account for just 14 of the 239 deposits included in the analysis. The contained volume of these discoveries makes up only 46.2 MMt, or 3.5%, of all copper in major discoveries since 1990.6

Even if you discover a significant supply time to market is extending. For mines that started production in the 2020–2023 period, the average lead time jumped to 17.9 years, fuelled by a longer exploration, permitting and studies phase and a longer period between the end of feasibility studies and the start of construction, which can be attributed to time spent obtaining financing and construction permits.6

Have a look at that Saint-Sophie chart above again. A number of potential economically feasible, significant grades (42%, 55%, 59%), to explore even at current small scale known in the reports.

All the 145 titles exist and grant exclusive mineral rights, not surface rights, and are undisputable as long as certain exploration spend is maintained. They are up for renewal in mid 2027. The table below aggregates the fees and exploration spend required, which was $185k at last renewal1b p77.

As mentioned above there were no 3rd party interests when IOS did the report but an NSR is now due; There is a 1% Net Smelter Return (NSR)3 on all mineral production from the Project owed to 1426706 BC Ltd. I reiterate this would be a great result if this comes into play.

There was some confusion in the report suggesting that since November 29th, 2024, a claim cannot be transferred to another party before the owner spends the required exploration expenditures (Law 63, item 80.1). This means that the current owner must spend CAD156,000 before the claims can be transferred to any interested parties. This has actually occurred as part of the consideration for the deal.

There are no areas within the project that have mining bans in place. Some consideration needs to be given to ESG and directly with the Maple Syrup industry. IOS recommends looking to liaise with locals straightaway to head off any future issues. There is some water on the project but the largest source Lac William has a luxury resort on the shoreline. Other water sources are available outside the project but addressing the use of this Lac may be worth exploring at an early stage. The area is within 2km of major roads and generally free of snow between May and December giving a large window for exploration and particularly straight after IPO. All modern amenities and services are available within driving distance, Thetford Mines was an asbestos mining hub and several industrial services are still available.

There is a real sense that the area has been undermined and had little modern testing applied. “It is unsure when exploration for copper started in the area. Artisanal copper mining in Upton, 100 km southwest of Sainte-Sophie, was reported by the Geological Survey of Canada in 1847 (Gauthier et al., 1989). Harvey Hill, a copper mine from which 450,000t were extracted between 1973 and 1976 and located in a similar geological environment as the Sainte-Sophie project was discovered in 1850.

The Sainte-Sophie property currently hosts fifteen copper occurrences, with more than half discovered by prospecting prior to 1910 (table 6.1). The most recent discovery, the Morrissette occurrence, was found in 1999, also by prospecting.”

A summary of shaft and trenches known to exist shown below, as per the ISO CPR1b p83

The figure above1 shows graphically how the 1970s was the peak in exploration and probably in an era where the need to chase copper finds was far less fervent than it is today. Soil surveys have dominated and most anomalies have been seen in veins and within the surface structure. Some reports attribute higher grades due to weathering (supergening). More modern techniques of geochemistry and geophysics need to be applied to the project and some significant drilling to understand the geology and at depth. There is debate amongst the reports what the source of the mineralisation is and that will dictate future works...” While most copper occurrences suggest the leaching of copper-enriched source, the presence of Mo at Poulin-Lachance, and antimony at other more distal occurrences, points to a porphyry-type system...” Supergene enrichment has occurred regardless of source and this has created some high-grade anomalies...further work required!

Drilling issues...the report highlighted the just 26 occurrences of drilling and these were done pre-GPS so no confidence of positioning and hence can’t be used for resource estimates. The table below highlights the results and also necessitates further work1b p99:

There are 15 mineral occurrences recorded on Saint-Sophie, mainly copper, but other minerals are listed above1b p92.

The overall conclusion by IOS suggests that the anomalous high grade copper occurrences are interesting but the general average grade is 2-5% across the property. That is of interest by itself given the overall average grade declines since the 1990s highlighted in this note.

They suggest: “The Sainte-Sophie property remains an interesting area for copper and other commodities such as silver and molybdenum, and future work should be more systematic and “knowledge-oriented” rather than an additional sampling program on already known occurrences. Expenditures should be devoted to the 5 most promising known occurrences and to follow-up on soil anomalies that are not yet link to mineral occurrences.”

IOS Recommendations:

Acquire the claims that cover the nearby Dussault, Poulin-Lachance and Viger occurrences.

The overall recommendation is to focus on the five most promising occurrences based on reported grades, mineralization or anomaly continuity, potential for growth and logistical complexities such as the nearby presence of houses, roads or powerline. In that regard work should focus on Quebec Megantic Copper, Option Poulin, Bernierville WNW, Wolfestown and Halifax. A short visit of Morrissette and Sainte-Sophie is also recommended. Historical soil data should be reprocessed to validate the anomalous zones.

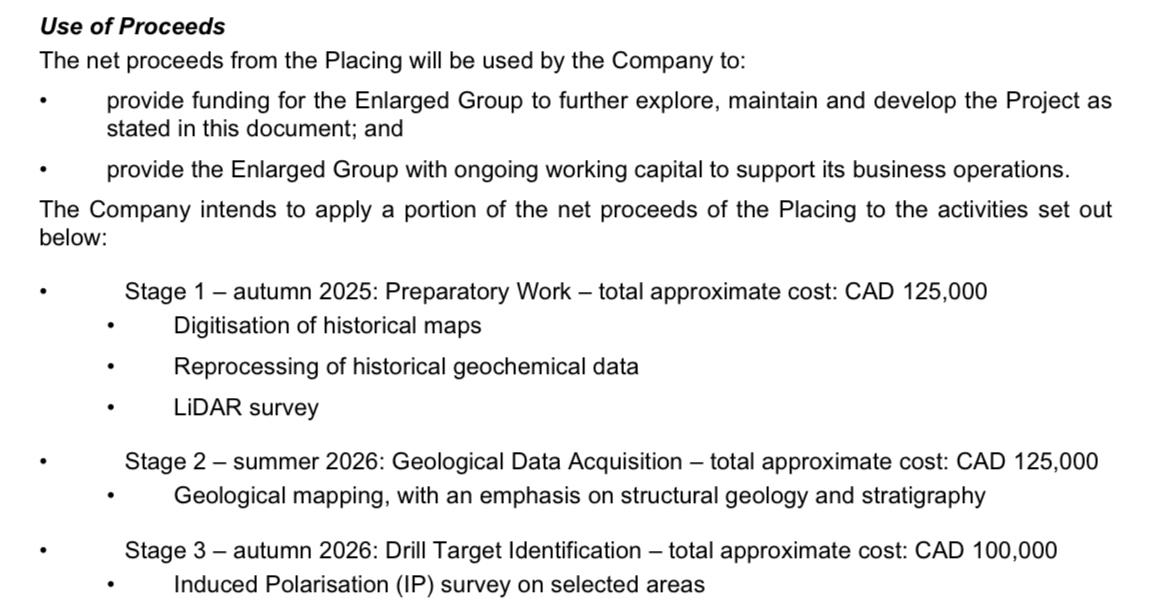

The following schedule is highlighted in the admission document1 p5 based on the recommendations by IOS:

These works total approx. $350,000 CAD or £186,700 at GBPCAD = 1.88 as at 18/9/25 and should easily be covered by the net of fees £760k hoping to be raised by placing at IPO for cashflow1 p3.

Although permitting is not required for the proposed 2025 work, it is highly recommended to contact the municipal authorities and landowners to informed then of upcoming work and Richmond Hill Resources intentions for the coming years. This will help identify possible hurdles and changes target priorities if needed.

A commodity Supercycle is by definition something cyclical which ultimately means there are huge peaks and troughs to manage. Exuberance and rapid growth tend to see over-capacity when demand slows or recessions hit and a period of depressed commodity prices results in under-investment in the supply side when demand sharply rises. This leads to periods of price trending significantly higher than their long-term average. Normal economic cycles average 2-5 years with Supercycles somewhere between 10-20 years.

They are characterised by huge economic expansions such as the 1960-70s but that ended in a high inflation and energy crisis bust. Some of this was attributed to the break-down of the dollar’s fixed exchange standard too. America’s crushing of the inflation bubble by Fed chairman Volcker crushed prices, demand and ultimately large-scale commodity supply. The 1980s through to the 1990s in contrast were known as the “Great Commodities Depression”.

A combination of China industrialising, modernising and becoming a manufacturing powerhouse in the 1990s alongside the www/internet revolution saw a period of strong growth which didn’t see commodity supply keep up after the low-price era. Despite the dot.com crash of the early 2000s the industrial revolution and emergence of the BRICS nations too saw a demand supply deficit emerge and persist. The last Supercycle was generally deemed to be between 2001-to 2011/3. There was a pause during the GFC in 2008/9 when a bout of global deflation peaked out prices. Post-recession recovery boosted by QE and fiscal bailouts globally were enough to attract new capital into mining and also support some mega-sized mergers to make large scale supply more accessible, but not before another peak in copper prices.

The monthly copper future chart above (produced by Jonathan Plant, the author of the note, using TradingView software with real-time pricing but drawn with a 1month timeframe for historical context), readily captures the GFC 2001-11 cycle and suggests the current one still has potential to rally further in the up channel drawn from the 2020 price low and supports Jeff Currie’s prediction below. The up channel identifies a channel of support along the base-line. There is no guarantee this leads to further upside in price but gives the reader/investor a tool to identify potential trends.

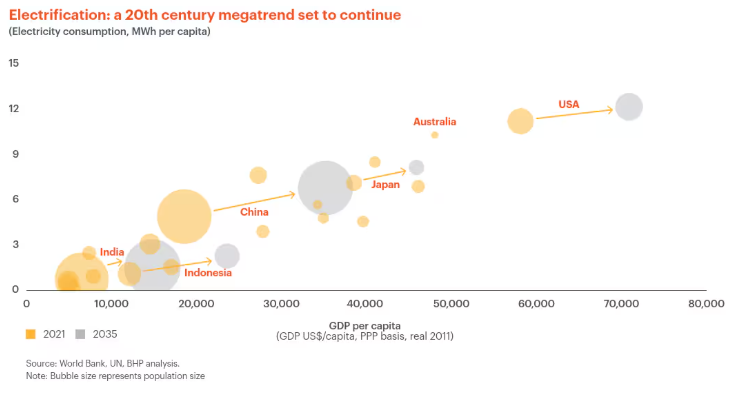

So why are we potentially in another Supercycle? We need something outsized to rhyme with past Supercycles. Often the reasons are in the rearview mirror but the 2020s have been characterised with a few of the past characteristics already. We have had a huge supply chain disruption with a pandemic slamming the brakes on activity, a Ukraine conflict with Russia which saw energy and food spikes in the main, but also a “probably on balance” unwarranted extra QE kicker. Cloud computing and digitalisation was enough for an economic cycle recovery but the acceptance of crypto-currency and bitcoin mining power demand alongside AI has seen the demand for data centre and electrification (see chart below) rise at scale5. The green energy drive for electric vehicles and further clean energy demand is far in excess of supply and even the infrastructure to manage the base load uptick. Copper as a result is in a demand over supply deficit which will be highlighted below versus published global policy demand and known copper supply7.

We have a return to a cold war type political environment which has caused a demand supply deficit in uranium for nuclear reactors alongside a surge of re-armament in response to Russian, and possibly Chinese, Iranian and North Korean threats, which has depleted the use of weapons grade uranium in enriching reactors. The dollar is being challenged as reserve currency and its weakness is aiding the uplift of commodity prices in general. Central Banks have moved to diversify their reserve assets away from the dollar into gold which generally sees a self-fulfilling cycle of dollar weakness and demand-pull gold price surges. A little discussed technical here is that Basle III resulted in gold being classified as a tier 1 reserve asset but requiring 85% physical ownership. This has totally transformed the settlement of gold futures in the West where it was pre-dominantly cash settled and much more frequent dis-locations in the physical markets for borrowing and settlement. China for years has been importing/holding physical gold and adding to supply pressure at the margin.

The Trump tariffs have caused all sorts of commodity peaks and troughs throughout as players struggle to deal with the details of import duties into the US. There have been huge import effects in copper being warehoused within US jurisdictions ahead of cut off dates and the gold debacle where huge amounts were imported into the US to try and avoid duties and also to deliver against large arbitrages in prices. This had the paradoxical effect for Trump since imports are a drag on the GDP calculation, something Trump is overtly trying to reduce (the imports), and the gold import surge showed up in the numbers to plunge GDP into negative territory. Economists everywhere were scrambling to exclude it. Trump then used it as a reason to punish Switzerland for being a huge exporter into the US. The negotiations with China highlighted the real crux here...the lack of supply the West has versus China, in particular, of critical minerals. A lot of these are critical to the semi-conductor industry where the US wants to stay at the front of the AI revolution. So it is interesting that RHR has mention of some potential antimony in the technical report.

Overall, we appear to have a lot of the ingredients in place for the usual outsized driver. Supply constraints appear to exist everywhere. Copper and oil are the classic recession/expansion commodities with tightness of supply often under-estimated. Copper is particularly vulnerable to major mines going offline. Natural disasters7 (p.79-81) can often be a driver like they were following the Cameco mine flood in 2006 for the last Uranium Supercycle7a.

Some8 are arguing that players like Glencore investing heavily into Argentina with a planned 1-2m tonnes pa production of copper in the next 10-15 years is a sign of supply catching up from new sources but by the time it arrives the Supercycle may have topped out.

Others aren’t waiting to find out and Anglo American approaching Teck Resources8a (Canada) is a classic M&A response to a lack of supply with cost efficiencies targeted. BHP and Glencore have been interested in Anglo and Teck respectively, previously, so we could see other deals announced soon. Whatever the rationale it is encouraging to see large scale corporate activity back in the copper space which should hopefully trickle down to at least increased interest in investing in the Junior end of the market.

Super-bull Jeff Currie, formerly of Goldman Sachs, has an interesting take on the Supercycle. There is an “odd lots” with Bloomberg podcast from last year which is worth a listen/read9. Copper is his highest conviction trade ever. He talks about the Supercycle taking 3-4 years for suppliers to start have confidence that prices are going to sustain at breakeven levels for new investment...that sits around $12k/tonne where we hit in the tariffs’ debacle. Currently at $10k/tonne we have doubled from the trough in 2020 which mirrors what happened in the 2000s cycle early years. Currie’s belief is new supply needs confidence the price jump is for real at higher prices before full commitment which has a physical supply lag attached anyway. That is why $15k+ is his target for copper, or $6.8/lb

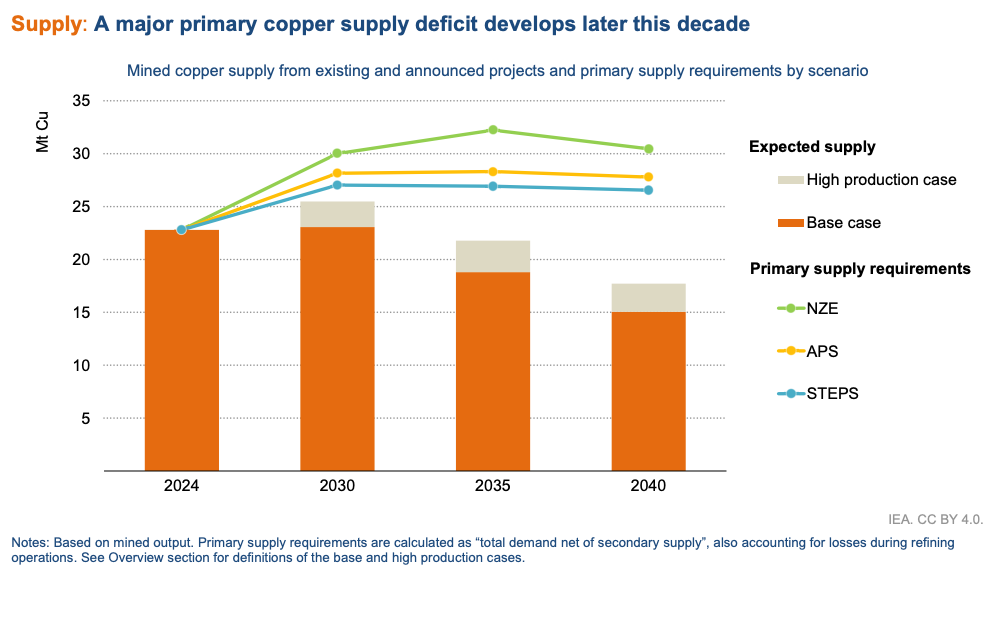

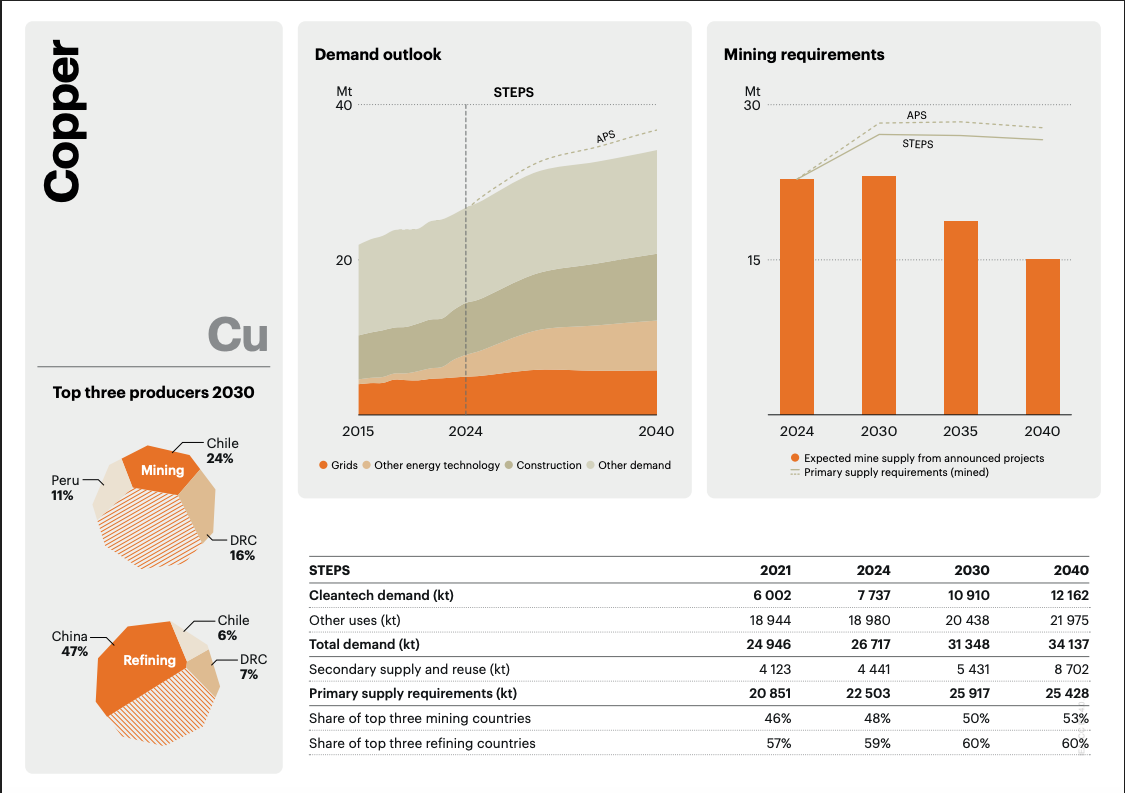

The STEPS/NZE/APS are effectively all the known policy commitments from Stated Policies Scenarios, Announced Pledges Scenarios and Net Zero emissions requirements...there is a clear deficit ahead7 (p.107)

The International Energy Agency (IEA) has warned that demand for copper is set to outstrip supply by 30% within the next decade, with security of supply further threatened by China’s growing dominance of the refining market.7 (p102)

Having established that Saint-Sophie (S-S) is anomalous in copper but as yet undefined resource and likely to have other associated minerals we need to see how it compares to other similar pre-discovery listings. This will mean comparing enterprise values of such companies since inferred resources are unknown. EVs should reflect the prospectiveness of each companies’ assets. On the basis we think that S-S has potential high grades with a well-defined immediate exploration plan, it should sit at valuations inline with the mean if not above. This is something which can adjust as the project is tightened up in definition and move towards the discovery valuations. Recognised in the technical report as an area for copper and other commodities such as silver and molybdenum suggests that improved measurement of such has a prospective chance at least for upgrades. Table 7.2.1 taken from the IOS report also has 9 of the 15 previously identified mineralisation occurrences as including Au (gold). Given this metal is trading at a new all-time high (ATH) of $3785 as of 23/09/25 any upgrade to resource here could attract investor interest in line with the current rally in gold stocks and the demand for gold itself.

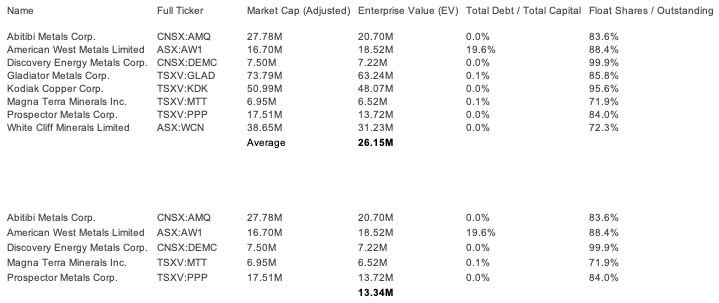

Below is a selection of pre-discovery peers alongside ones who recently achieved significant valuation uplift on project advancement. (Values as of 19th Sep 2025 generated by finbox.com screening tool18).

Company Name

Ticker

Market Cap (£m)

EV (£m)

Project

American West Metals

ASX:AW1

16.70

18.52

Storm Copper, high grade Cu-Zn, surface anomalies guiding exploration, Nunavut

Kodiak Copper

TSXv:KDK

50.99

48.07

MPD Project, BC, 10m mineralised zones approaching resource estimate Cu

Abitibi Metals

CNSx:AMQ

27.78

20.7

B26 deposit Cu-Au-Zn with Phase 3 drilling, similar to nearby Salay mine

Magna Terra Minerals

TSXv:MTT

6.95

6.52

Humber Project, Newfoundland, early-stage exploration Cu-Co

Discovery Energy

CNSx:DEMC

7.50

7.22

Crystal Lake in BC, porphyry Cu, magnetic high and Cu anomaly

White Cliff Minerals

ASX:WCN

38.65

31.23

Coppermine, Nunavat, high grade, large-scale Cu, Au and Uranium

Gladiator Metals Corp

TSXv:GLAD

73.79

63.24

Whitehorse Copper Project, Yukon

Resource ready Cu 1-4% at scale, abandoned mine in 1982 downturn, no modern exploration

Prospector Metals Corp

TSXv:PPP

17.51

13.72

ML Project Yukon $12m historical geological database Au-Cu

Devon, Ontario Cu-Ni, Savant, Ontario Au

These projects share high grade potential with RHR, some are in infrastructure rich areas or previous large hostings. Some are open in multiple directions allowing for growth and some are the result of opportunistic purchasing for building out exploration portfolios and the higher values either have defined resource or have made significant exploration improvements like Gladiator, White Cliffs and Kodiak.

With RHR listing on AIM we have taken values from 19th Sep 2025 in £ terms for comparison. RHR is listing at a market cap of £5.9m and EV of £4.5m (as detailed in the shareholder section below).

We believe this suggests RHR is coming to market at £4.50/£13.34 or at 33.73% of pre-discovery peers’ EV. Such a low rating gives scope for a short term uplift as the market digests that RHR has at least a sector average prospectiveness, if not potential for some high-grade copper discoveries and from a starting point of exploration advanced along the curve. This suggests potential for a quick share price appreciation towards market averages, before entering into the real zone of prospectiveness which hopefully ties in with the recommended exploration timetable of the next year to 18 months, which could deliver material upgrades. A reminder that in this sector failure to produce results can have a similarly negative reaction to share prices.

Should they make significant discoveries along the Kodiak/White Cliffs definition then the pathway to a sector average including those names, and Gladiator, of £26.15m would seem an appropriate bus stop on the exploration curve potential. A more nuanced valuation can be performed once we have resource estimates to play with (hopefully!) and perhaps even a premium to sector averages.

White Cliff Minerals10 WCN is a perfect example of how this pre-discovery curve works.

Listed on the Australian ASX, White Cliff Minerals (ASX: WCN) acquired two expansive and highly prospective copper, uranium, gold, and silver exploration assets in northwestern Canada in 2024. Their 3 projects in aggregate cover Copper, Uranium and Gold (in Australia) assets. Their Coppermine project in Nunavut, Canada, originally had rock samples showing high grades of 30% Cu. A highly prospective project in an area of previously identified high grade discoveries and mined projects. They were confident of further works confirming these high grades and also likely further discoveries with potential for a bonanza find. They enacted a maiden field project and subsequent results from various tests yielded results over a series of news announcements that improved grades to over 50%-60% Cu and with materially enhanced vein systems of significant lateral extent. The company believed they were seeing the highest-ever recorded copper assays from a representative rock chip sample anywhere in the world and, in fact, are approaching the stoichiometric maximum copper can reach in an ore-forming mineral. The period from the study to results of the assay saw a share price uplift of 100% even though this project was only 1/3 of the company’s projects. East Coast Research performed an EV comparison and upgraded their A$23.48m valuation for this project to A$46.66m and gave it a higher premium on the project re-classification to its peers11. This is a story pre-dominantly of assay results and rock chip samples improved followed up with drilling to confirm sulphide mineralisation. Basically, this is where RHR stands with a well-defined programme to quickly concentrate on the most probable positives.

RHR and Saint-Sophie is smaller in acreage but that doesn’t preclude significant occurrences. They also have high grades of copper to investigate, confirm and potentially upgrade. The current drilling samples may only have gone down to 61m but there have been numerous reports of veins and intercepts with copper within shafts and trenches without any real size calculations performed. Some instances have exhausted surface opportunities but not precluded further drilling work finding further occurrence beneath roads etc.

Similar successful results to White Cliff could see material upside for the RHR value, particularly as it is the sole focus of the company. This is an exciting opportunity with numerous obvious areas of exploration. There is an argument that the valuation should move quickly towards that sector average of £26.15m, including the discovery plays, which supports my price target.

In fact, given the potential quality and advancement of RHR’s project, a valuation similar to White Cliff’s is not unlikely and the East Coast post upgrade note suggests they are 50% undervalued at A$0.019 (currently A$0.024 23/09/25). This would move them towards the Kodiak £48m EV and Gladiator £63m EV levels. For RHR then it is not unreasonable to suggest a 10p price target expectation within the 18m of planned exploration works, subject to successful results.

Simple, conceptual valuation metrics for the investor to consider how quickly values can change as news updates are made:

Part of the mystique in mining is all the geological terminology and the ore types which thankfully the geologists can deal with. Even though there isn’t a geological reserve estimate available for any of these it might be instructive to an investor to consider how the deposit structure will be put together.

As a proxy if you have a regular triangular prism, its volume is half of the cuboid it is made from12. That is done by cutting through the diagonal of one of the end faces to produce 2 triangular prisms. So, in the mining context, if we know the triangulation of the deposit, something done in the real world with sophisticated tools to be accurate based on the drill holes etc. and the randomness of how deposits are formed13, then the volume can be calculated approximately. For the average calculation we can take the volume of the cuboid...length x width x height to find the m3.

Let’s look at the Option Poulin occurrence shown above (GM 12781-A). A 6m (20 feet) long quartz vein with malachite and chalcocite yielded a grade of 42% Cu. This vein is 75cm wide and parallel to the foliation / bedding of the host rock, which is weakly mineralized (0.32% Cu) over a thickness of 1.5m.

Purely as an exercise of showing how the simple economics can look:

(0.75m wide x 6m long x 1.5m depth) / 2 for the triangular prism = 3.375m3

Generally, common rock ore density is 2.5g/cm3 or 2500kg/m3 with copper ore twice the density14.

So the mass of this copper ore = 3.375 x 2500 x 2 = 16875kg = 16.875 tonnes

1 tonne = c. 2205 lbs

Therefore mass = 16.875 x 2205 = 37203 lbs

Copper future price HG = $4.6130 / lb as of 17/09/25

Copper grade

lbs

Value $

20xL and 10xD in $

1% Cu

372

1,716

343,200

42% Cu

15,625

72,079

14,415,800

So, you can see the valuation of an ore body that expands by just a few metres in length and depth...The reason why copper supply is in deficit to demand is that the larger finds are ever deeper in the ground, starting at depths materially below the furthest drilled in Saint-Sophie. Reserve valuation will be materially hit by mining costs and will require porphyry or veins of significant size to make it economically viable. The larger copper mines spread over kms not just metres

This is why excitement surrounds extension to any of the 3-D dimensions with obviously all 3 increasing most valuable. The purpose of this calculation is to give investors a sense of why incremental news flow can be so material to valuations.

As the change in direction suggested in the RNS15 RHR has considerable experience in the natural resources sector.

Hamish Hill is also executive chairman of Gunsynd16 who invest in Canadian mining projects looking for upscale.

Gunsynd has made recent upgrading success17 after buying copper and uranium projects in Canada; they updated on Falcon Lake (Cu) and Merlin (Uranium) within a couple of months re rock chip samples containing 15% and 19% Cu and proceeded to a program of works. They have assets proximate to Future Fuels which have made recent uranium discoveries in Nunavut and are close to the White Cliff Minerals project we have identified as a case study for copper discoveries. This should give investors in RHR confidence that the management team are in the mix for choosing projects with good chances of upgrade.

The working number for the EV is an anticipated £5.9m market cap less the IPO cash injection of £1.4m placing proceeds hence the £4.5m we are using.

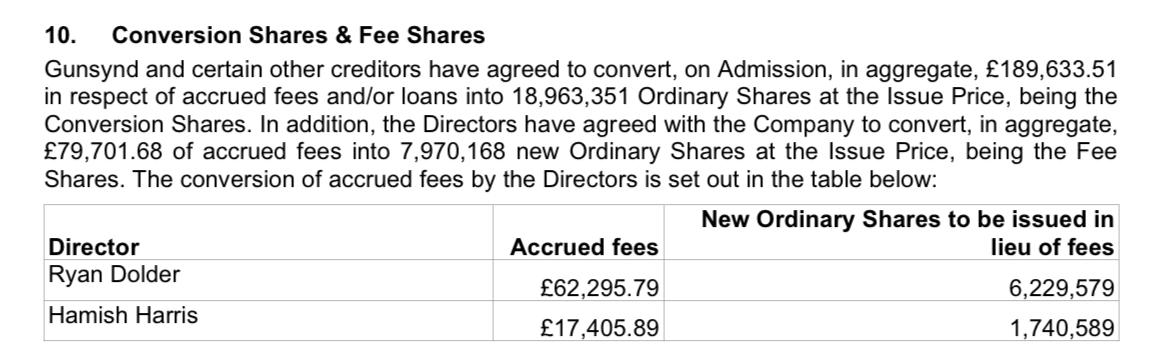

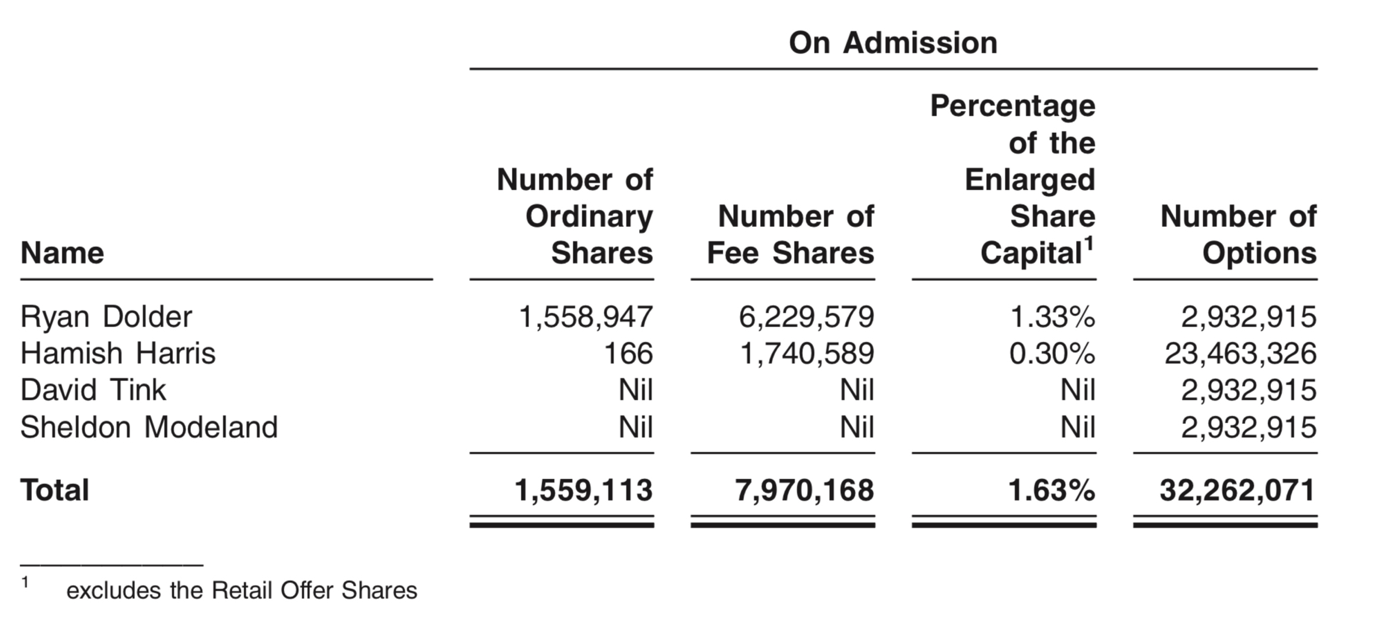

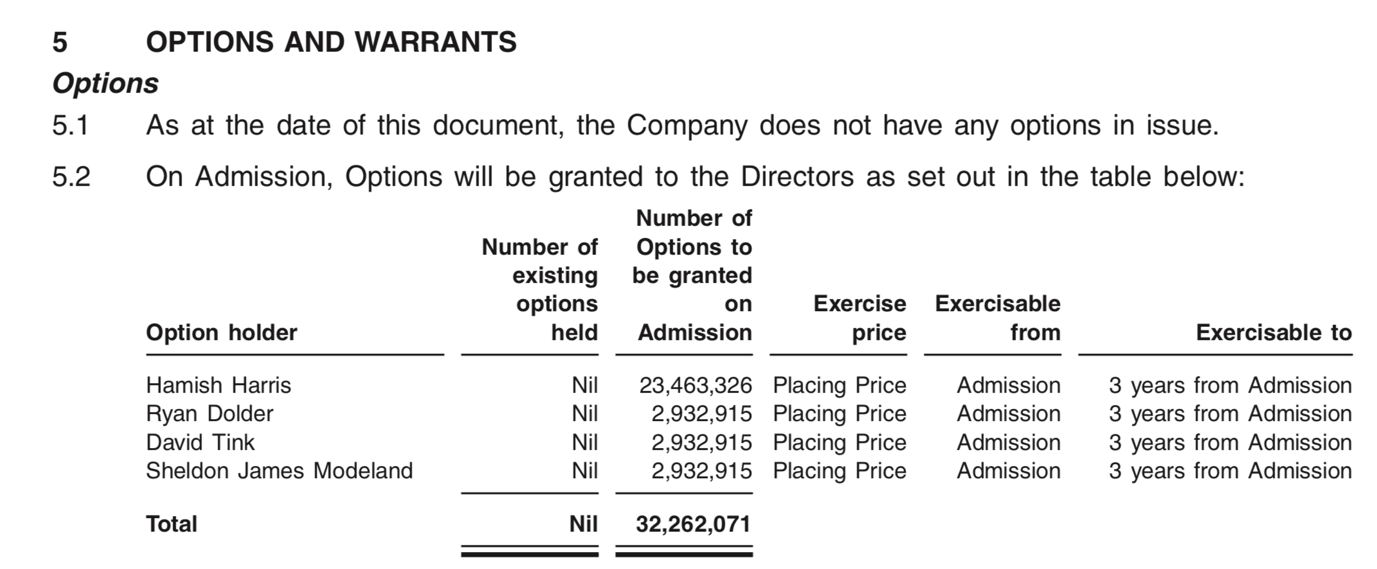

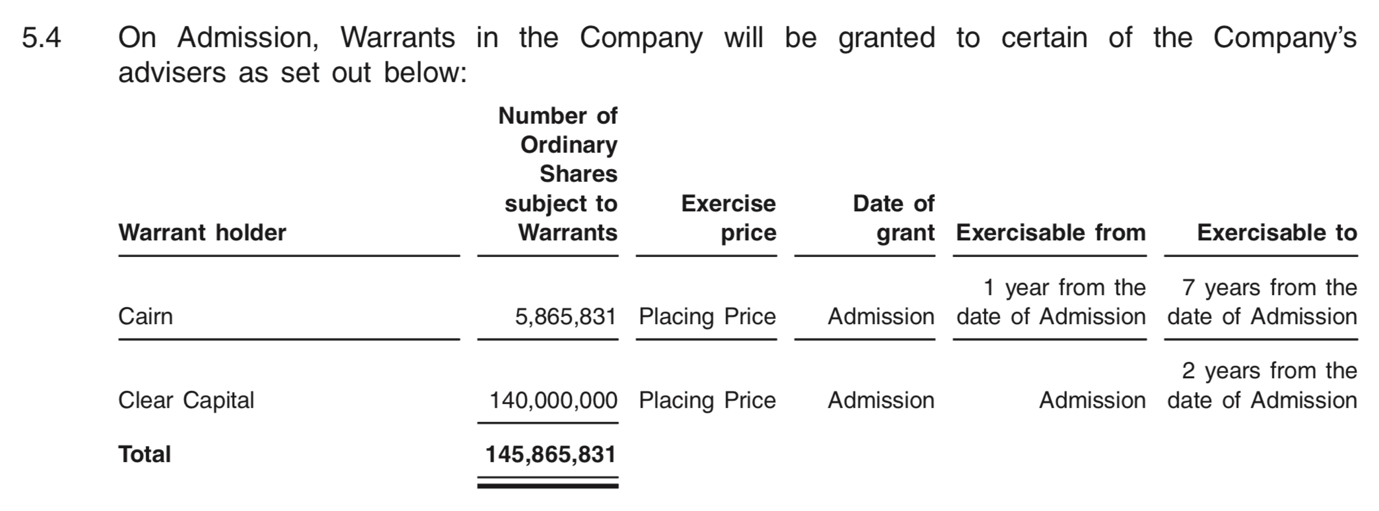

Gunsynd owns 3.59m of the 106m in issue pre the Reverse TakeOver (RTO). They also have a loan of £144,259 outstanding including interest19. This is dealt with in the admission document:

Further tidying up of the share structure and balance sheet has been dealt with in section 10 p17 shown below:

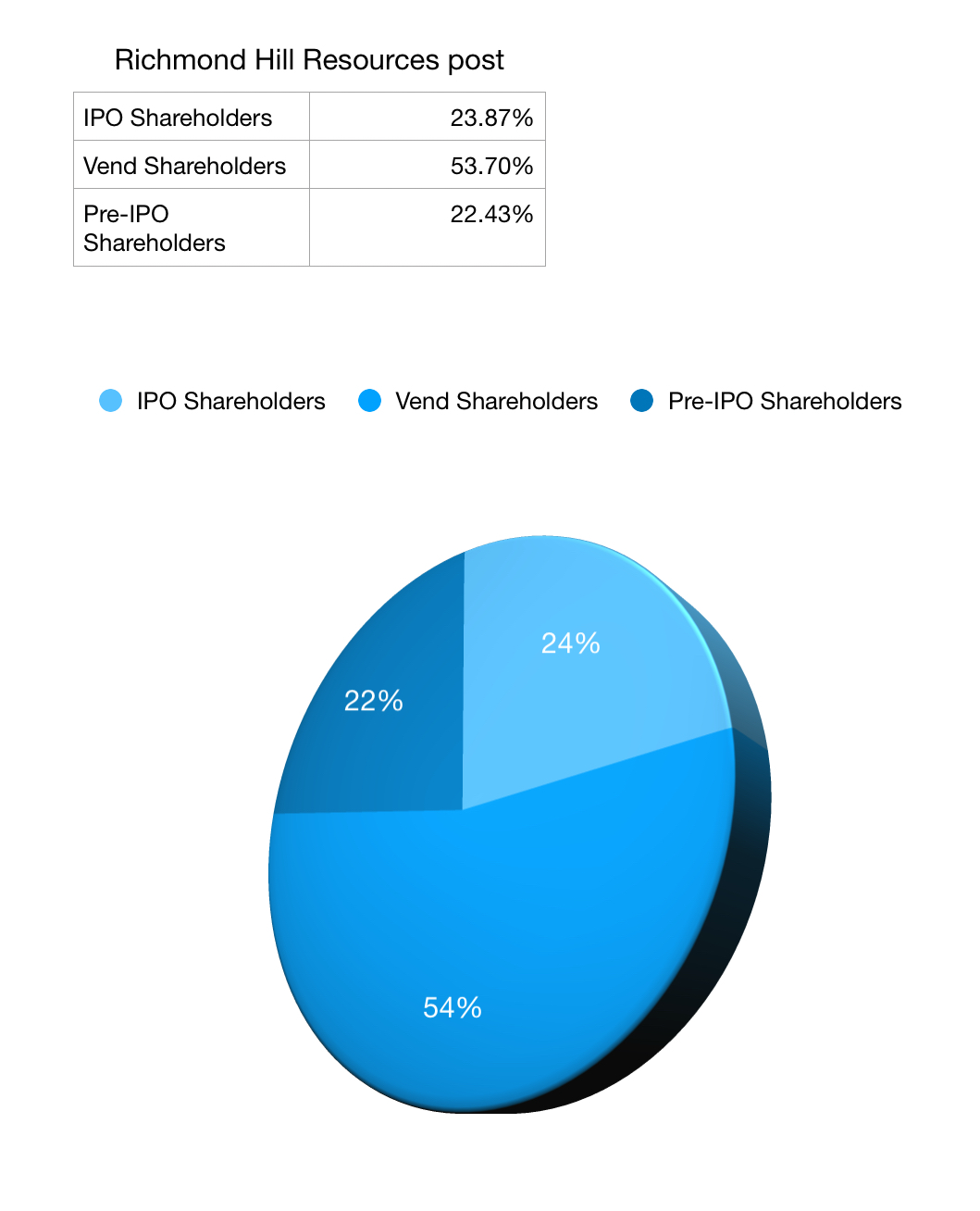

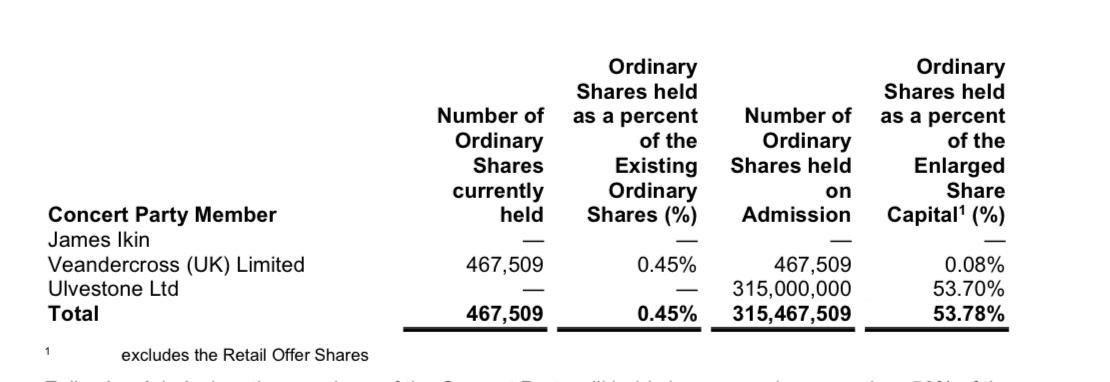

The original RNS4 was with Three Mile Beach Ltd., a wholly owned company of James Ikin registered in the British Virgin Islands. Ulvestone, also 100% owned by James Ikin, is now the beneficiary of the vend for the Bulawayo assets and will hold 56% of the market cap on AIM admission. He has a lock in of 12 months and an orderly disposal requirement of 6 months thereafter. This should ease selling pressure into any significant discovery announcements.

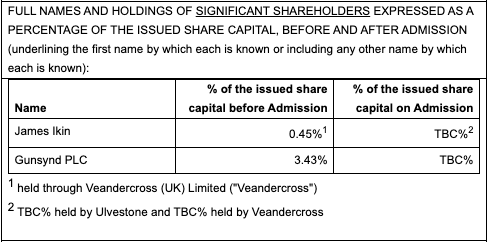

The graphic above shows the concert party of ownership from page 23 of the admission document section 24. In aggregate working in concert they can increase holdings without having to make an offer for the company but cannot act alone without permission from the Takeover Panel.

The long-stop date was postponed to October 15 from June 30 due to administrative delays in Canada whilst Richmond Hill’s shares remained temporarily suspended on Aquis.

As of Tuesday 30th, trading of its shares has resumed, and Richmond Hill expects the enlarged company’s shares to move to AIM on October 15 with the last quote at 1p on Aquis reflecting the placing price.

It has also proposed a £1.4 million placing priced at 1 pence per share, alongside the subdivision and reorganisation of its shares, subject to voting approval at a meeting on October 13 with the intention being for dealings in the Company’s shares to begin on Wednesday, October 15th.

There is also an intention to offer a retail placing1b p147 with expectations of raising up to £250,000 additional funding. This would be c.25m further £0.01 ordinary shares or a further 4% issuance. The company states in the use of proceeds section the need to raise significant finance to advance the project into future production and to pay the £150,000 consideration part of the project purchase price. These proceeds from the retail offer could at least satisfy the vend element.

The company has split the existing shareholders into ordinary and deferred shares1 p17 of 104,649,639 ordinary shares of £0.001 each and the same number of deferred £0.005 shares. The ordinaries retain the same rights as the existing ordinary shares. The purpose of deferred shares is often to provide for the implementation of an employee incentive plan such as the admission document highlights on page21 with the intention being to not exceed 10% of the issued share capital.

Strengths

Tier 1 jurisdiction

High Grade surface anomalies

Large historic data sets

Kind climate conditions May-Dec

Previous mining infrastructures

AIM listing gives access to more capital

Experienced Natural Resources focused Board

NI 43-101 standards in Canada are higher than JORC estimates and require a technical report to support them

Will be cashflow positive from IPO

Weakness

No defined resource estimates as yet makes the project highly speculative.

Few drill holes and not GPS accurate prevents resource estimates for now.

Pre-Discovery/Pre-revenue could require further capital raisings.

Opportunities

Potential for quick confirmation and upgrade of mineralisation.

Geology not well understood provides for potential re-grading.

Low hurdle for project advancement.

Modern exploration techniques hardly used historically.

Clear Pathway to project development and drill targets.

May have other critical mineral deposits such as Antimony and Gold.

Macro support from widely agreed demand-supply deficit in copper.

Large Cap M&A could lead to purchasing of well-defined resources.

Successful project development could lead to investor trust in developing a portfolio of assets

Threats

Global recession threats and Tariff effects may increase volatility of copper price, 1effecting economic viability of mining.

Fragile nature of junior stock markets although has been improving of late with a rebound in mining stocks alongside the recent commodity uplifts.

RHR has high grade Copper anomalies in a relatively large area, with good infrastructure, in a friendly Tier 1 zone. (Communication of any interactions with local fraternity during exploration works will be indicative of future costs down the curve).

Management is producing similar uplift on comparable projects. Defined project programme with weather advantages for potential early news flow should be a short-term valuation catalyst.

Copper price backdrop is a medium-term support as is renewed large scale M&A in the copper sector.

Potential for critical minerals (antinomy, silver and gold?) and geographical proximity to US adds interest.

No new drilling has been done and the existing activity has been inadequate and shallow.

Many measurement inconsistencies through history with copper not always a key resource at times of previous exploration, perhaps leading to lack of follow through on the site.

RHR represents an opportunity to invest in a prospective copper project with already identified anomalies and potential for at least tighter definition of the existing project, for a working capital outlay of c.£500k in the first instance.

Listing on the UK’s AIM market at an EV sitting at a substantial discount to comparable peers.

Investors should consider RHR as a speculative addition. When seen in the context of successful peers and enhancing the project upwards, the market will generally reward this progress, and should recognise RHR’s strong project starting point at an early juncture. Junior Mining is literally prospective in nature and future success may require further funding. For now, it is a great opportunity at the base of that Lassonde Curve upside with a 10x upside possible within the exploration timetable and a 3x uplift highly likely in the near term.

Note 1 Admission document including relevant CPR/IOS Geosciences technical report

Richmondhillresources.com investors announcements 29th Sep 2025

2025-09-25-Publication-of-Admission-document-RNS

Note 1a Section 4 shows specific extracts from the CPR competent person’s report. Section 28 refers to relying on information contained in other publicly available data. We have included some tables from the report not included by the Company in their admission document as this provides the potential investor with a clearer summary of the project, where and what its previous occurrences of copper were. These additional extracts are labelled 1a.

Note 1b richmondhillresources.com investors (scroll down) admission document

Note 2 elements.visualcapitalist.com Dec 12th 2020

Visualising-the-life-cycle-of-a-mineral-discovery

https://elements.visualcapitalist.com/visualizing-the-life-cycle-of-a-mineral-discovery/

Note 3 londonstockexchange.com Schedule-one-richmond-hill-resource-plc

Sep 8th 2025

Note 4 original deal with Three Mile Beach Ltd April 10th 2025

Richmondhillresources.com RNS-binding-term-sheet-RTO-Quebec-copper-MA-002.pdf

Note 4a aquis.eu/stock-exchange 24th Feb 2025

Result of General Meeting, Strategy and Name Change

https://www.aquis.eu/stock-exchange/announcements/5051339

Note 5 bhp.com how-copper-will-shape-our-future Sep 30th 2024

https://www.bhp.com/news/bhp-insights/2024/09/how-copper-will-shape-our-future

Note 6 spglobal.com July 4th 2024

new-major-copper-discoveries-sparse-amid-shift-away-from-early-stage-exploration

Note 7 IEA.blob.core.windows.net GlobalCriticalMineralsOutlook2025 June 25

Note 7a investingnews.com highest-price-for-uranium 4th April 2024

Highlighted section references the CAMECO Cigar Lake flooding as major supply shock for uranium

Note 8 mining.com August 21st 2025

glencore-targets-1mt-of-copper-in-argentina-over-coming-decade

https://www.mining.com/web/glencore-targets-1mt-of-copper-in-argentina-over-coming-decade/

Note 8a mining.com Sep 10th 2025

anglos-go-to-banker-drives-teck-deal-after-seeing-off-bhp

https://www.mining.com/web/anglos-go-to-banker-drives-teck-deal-after-seeing-off-bhp/

Note 9 omny.fm May17th 2024

jeff-currie-on-why-copper-is-his-highest-convictio

https://omny.fm/shows/odd-lots/jeff-currie-on-why-copper-is-his-highest-convictio

Note 10 relait.wcmminerals.com.au/announcement-detail/

Large scale copper discovery confirmed Oct 4th 2024

Note 10a relait.wcmminerals.com.au/announcement-detail/

John Hancock Cornerstones $5m Raising at Premium to Market 8th Oct 2024

Note 11 relait.wcminerals.com.au/research

(click on each header for East Coast Research reports)

https://relait.wcminerals.com.au/research

Note 12 bbc.co.uk rectangular cuboids https://www.bbc.co.uk/bitesize/guides/zqjhy4j/revision/4#:~:text=If%20a%20rectangular%20loaf%20of,Cuboids

Note 13 slideshare.net

the-mineral-reserves-amp-reserves-estimation-using-triangular-methods/141394254

Note 14 thoughtco.com April 30th 2025

densities-of-common-rocks-and-minerals-1439119

https://www.thoughtco.com/densities-of-common-rocks-and-minerals-1439119

Note 15 richmondhillresources.com RNS-Feb-03-2025-vs-6.pdf

https://www.richmondhillresources.com/wp-content/uploads/2025/02/RNS-Feb-03-2025-vs-6.pdf change of strategy

Note 16 gunsynd.com company website

Note 17 youtube.com Vox Markets interview with Hamish Harris 10th Oct 2024

https://www.youtube.com/watch?v=4oG1vPGeHnQ

Note 18 finbox.com/screener

website with free trial for users to create comparisons in real-time

Note 19 gunsynd.com/aim-rule-26/investments scroll to RHR values

https://www.gunsynd.com/aim-rule-26/investments/

Nothing in the above article should be considered investment advice.

Small Cap or Aquis listed companies can be highly illiquid making them difficult to sell at the quoted price, and in some cases, it may be difficult to sell them at any price. Small Cap or Aquis listed companies can have a large bid / offer spread which means there could be a large difference between the buying and selling price. Companies listed on the Aquis market can be highly volatile and are considered high risk speculative investments. The value of your investment can go down as well as up, your Capital is at risk you may not get back the amount invested. Past performance is no guarantee of future performance. Investments in IPO’s & RTO’s involve a high degree of risk and are not suitable for all investors. All investments made into an IPO, RTO in a secondary issue should always be made solely based on the information provided in the relevant prospectus and any other supplementary documentation. Please ensure that you fully understand the risks involved. If in any doubt, please seek independent financial advice. This document is published by Clear Capital Markets and does not constitute a solicitation or personal recommendation for the purchase or sale of investment. The investments referred to may not be suitable for all investors. Any data or views given should not be construed as investment advice. Every effort is made to ensure the accuracy of the information, but no assurance or warranties are given. Clear Capital Markets Limited is authorised and regulated by the Financial Conduct Authority FRN 706689.

Clear Capital Markets Corporate Broking acts as a Corporate Broker to Richmond Hill Resources PLC and holds warrants and shares in the company. Employees and/or directors of Clear Capital Markets may deal in shares of Richmond Hill Resources PLC for their own personal accounts. These scenarios may give rise to a conflict of interest where Clear Capital Markets also provides clients with an advisory service for transactions involving Richmond Hill Resources PLC. The firm has established Conflicts of Interest (“COI”) and Personal Account Dealing (“PAD”) policies to mitigate the risk of a conflict causing damage to the interests of its clients. The measures taken include (i) enforcing minimum holding or ‘lock-in’ periods; and (ii) requiring internal review and approval from the compliance department for employees or directors entering into personal transactions involving Richmond Hill Resources PLC. The COI and PAD policies are available upon request. Before Clear Capital Markets proceeds with a placing, a number of factors are considered including liquidity of stock, company diversification, market capitalisation and potential news flow. Only once minimum criteria are satisfied would we elect to proceed. Any remuneration payable to Clear Capital Markets has no bearing on whether it proceeds with a placing. These administrative controls mitigate the risk of a conflict causing damage to the interests of a client, but the inherent risks of this business model cannot be eliminated. Accordingly, Clear Capital Markets is required to disclose this conflict to help clients assess the service being offered in light of Clear Capital’s own interests, and to decide on the extent (if at all) to which they will rely on, or proceed with, the service.

We will reach out for a quick introductory fact find to see how we can best serve your specific needs and arrange a convenient time for a consultation with a member of the appropriate specialist team.

An Advisory Broker will contact you for a deeper fact find and share information on how we can best enhance your portfolio.

We will process your application in accordance with FCA regulations to ensure that your appropriate risk profile is set. You will then have access to an extensive suite of investments, supported by your dedicated Advisory Broker.