1. Introduction

2. Scope

2.1 What is the Purpose of this Policy?

2.2 When does the Policy apply?

2.3 Client Categories

3. Achieving Best Execution

3.1 What does “Best Execution” mean?

3.2 What factors does the Firm consider to achieve Best Execution?

3.3 Third-Party Execution

4. Compliance with Client Instructions

5. Choosing an Execution Venue

6. Order Handling and Execution Arrangements

6.1 Order Receipt and Transmission

6.2 Order Prioritisation

6.3 Aggregation of Orders

6.4 Allocation of Orders

6.5 Timely Execution

6.6 Limit Orders

6.7 Record Keeping

7. Monitoring Execution Quality

8. Updating this Policy

9. Consenting to this Policy

10. Contact Details

1. Introduction

This Policy sets out how Clear Capital Markets Limited (“the Firm”) complies with the Financial Conduct Authority’s (“FCA”) requirements on the execution of client orders (“best execution”), as derived from the Markets in Financial Instruments Directive (MiFID II) and implemented in the FCA Handbook (primarily COBS 11.2A).

The Firm provides investment services including investment advice, the reception and transmission of orders, and execution-only services in relation to equities. The Firm does not typically execute transactions directly on trading venues. Instead, the Firm may agree transactions directly with market makers or transmit client orders for execution via appointed custodians. In all cases, the Firm remains responsible for taking all sufficient steps to obtain the best possible result for its clients, including where orders are transmitted to third parties.

The Firm has also established internal order handling and execution arrangements in accordance with COBS 11.3 to ensure that client orders are handled promptly, fairly and in due turn. These arrangements support the Firm in achieving best execution on a consistent basis.

2. Scope

2.1 Purpose

The Firm recognises the importance of achieving the best possible result when executing trades for its clients and is required to take all sufficient steps to do so. This is important for maintaining and developing our relationship with our clients.

The Firm strives at all times to act fairly and reasonably in dealing with its clients. In certain cases where the Firm is providing order execution services to its clients, it is required under MiFID II and applicable FCA rules to establish and comply with a policy on best execution. The purpose of this Policy is to set out this obligation to the Firm’s clients in a clear and concise manner.

2.2 When does the Policy apply?

This Policy applies where the Firm:

- executes orders on behalf of clients; or

- transmits orders to third parties for execution; or

- places orders following the provision of investment advice.

This includes transactions placed following advice provided by the Firm and transactions placed on an execution-only basis.

Where the Firm follows a client’s specific instructions, it will satisfy its best execution obligations only in respect of the part of the order to which those instructions relate. This Policy will continue to apply to any other aspects of the order not covered by those instructions. This includes where:

a) The Firm follows a client’s specific instructions to execute their order in a particular manner or at a particular price; and

b) The Firm follows a client’s specific instructions to execute a specific part or aspect of an order.

This Policy applies to all transactions the Firm arranges or executes on clients’ behalf, whether arranged or executed through affiliated companies or otherwise. The Policy also applies to the Firm’s internal processes for the receipt, transmission and handling of client orders, including where the Firm relies on third parties for execution.

2.3 Client Categories

This Policy applies to clients categorised under FCA rules as:

- Retail Clients

- Professional Clients

The Firm applies its order handling arrangements consistently across client categories, ensuring that no client is unfairly prioritised over another.

The Firm does not owe best execution obligations when dealing with Eligible Counterparties. However, the Firm will continue to act honestly, fairly and professionally and in accordance with applicable FCA Principles and conflict of interest requirements.

3. Achieving Best Execution

3.1 What does “Best Execution” mean?

“Best execution” means:

a) That the Firm has established this Policy, which is designed to achieve the best possible result (considering all relevant factors described below), across all orders on a consistent basis, for financial instruments covered by MiFID II when placing orders for execution with execution venues identified in this Policy.

b) That the Firm is committed to comply with this Policy.

c) That the Firm takes steps to monitor, review and update this Policy to ensure that it continues to achieve such results.

d) Best execution does not require the Firm to obtain the best possible result for each individual transaction, but rather to apply a consistent process designed to achieve the best possible result on a consistent basis.

For Retail Clients, the Firm will determine the best possible result in terms of the total consideration, which represents the price of the financial instrument and the costs related to execution, including execution venue fees, clearing and settlement fees, and any other fees paid to third parties involved in the execution of the order.

The Firm will prioritise total consideration when executing orders for Retail Clients, unless it can demonstrate that taking other execution factors into account would deliver a better overall result for the client.

For Professional Clients, other execution factors such as speed, likelihood of execution, liquidity and size of the order may be given greater importance where appropriate

3.2 What factors does the Firm consider to achieve Best Execution?

In achieving best execution, the Firm considers several factors (unless otherwise instructed by the client).These include:

a) Price.

b) Costs.

c) Speed.

d) Likelihood of execution and settlement (liquidity).

e) Size.

f) Nature.

g) Type and characteristics of the financial instrument.

h) Characteristics of the possible execution venues.

i) Any other consideration relevant to the execution of the order.

While total consideration (price and costs) are generally key factors, the overall value to the client of a particular transaction may be affected by the other factors listed above. The Firm may conclude that factors other than price and costs are more important in achieving the best possible result for its client. The relative importance of each of the factors will differ depending on:

a) The client’s categorization as a Retail or Professional client.

b) Any special objectives the client may have in relation to the execution of the order.

c) The characteristics of the client’s order.

d) The characteristics of the financial instruments to which the client’s order relates.

e) The characteristics of the venues (if there are more than one) to which the client’s order may be directed.

The relative importance of the execution factors will vary depending on the specific circumstances of each order. In determining this, the Firm takes into account the criteria set out above, including the characteristics of the client, the order, the financial instrument and the available execution venues.

3.3 Third-Party Execution

The Firm may execute transactions in a number of ways depending on the nature of the instrument and market conditions. In many cases, the Firm will agree transactions directly with market makers or other counterparties. In such cases, the Firm is responsible for selecting the execution counterparty, taking into account the execution factors set out in this Policy. Once agreed, transactions are typically booked and settled via the Firm’s appointed custodian brokers, who provide custody, settlement and operational support. The use of a custodian does not affect the Firm’s responsibility for achieving best execution. In other cases, the Firm may transmit client orders to its appointed custodians for execution on trading venues.

In selecting custodians, market makers and other counterparties, the Firm considers factors including execution arrangements, price, costs, liquidity, operational capability, settlement reliability, regulatory status and financial stability.

The Firm maintains an approved list of the custodians, market makers and other counterparties with whom it transacts. These entities are assessed prior to onboarding and on an ongoing basis. Responsibility for the approval and ongoing oversight of these entities rests with the Board.

4 Compliance with Client Instructions

Where a client provides specific instructions for the execution of an order (for example, relating to the price, timing or execution venue), the Firm will follow those instructions as far as reasonably possible. This may include instructions to execute with a particular counterparty or market maker.

Where the Firm follows a client’s specific instructions, it will meet its best execution obligations only for the parts of the order not covered by those instructions. This Policy will continue to apply to any remaining aspects of the order.

For example:

- if a client instructs the Firm to execute a transaction at a particular price, the Firm will execute the order at that price where possible; and

- if a client instructs the Firm to use a particular execution venue, the Firm will not be responsible for selecting the venue.

Clients should note that where specific instructions are provided, this may limit the Firm’s ability to take the steps set out in this Policy to obtain the best possible result for the execution of the order.

All client instructions are recorded and retained in accordance with the Firm’s record-keeping obligations.

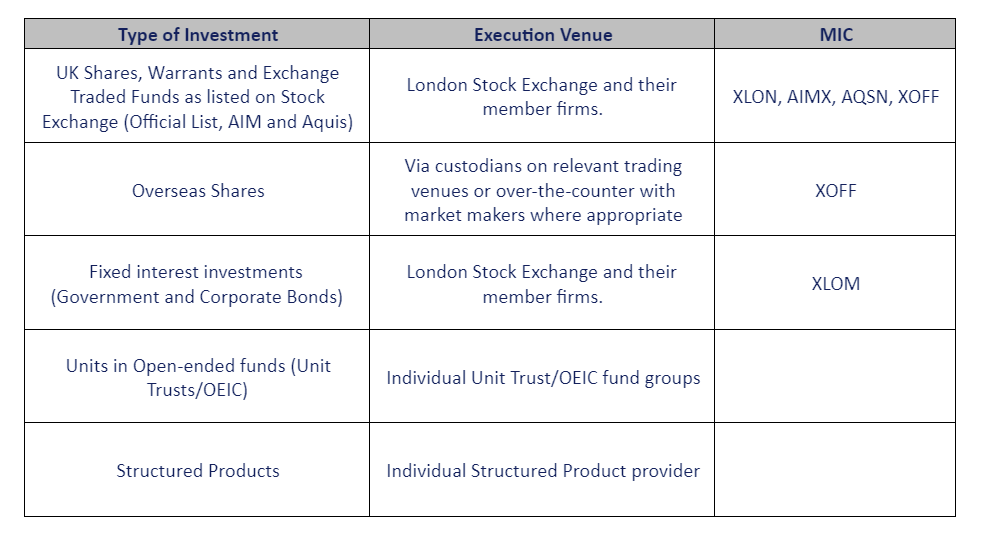

5. Choosing an Execution Venue

The Firm executes transactions either on trading venues or by agreeing transactions directly with market makers. In many cases, particularly for less liquid or over-the-counter instruments, the Firm will select a market maker as execution counterparty.

Where the Firm executes directly with market makers, it selects counterparties based on its assessment of best execution factors, including price competitiveness, liquidity, speed of response, likelihood of execution and settlement, and creditworthiness.

Transactions are typically booked and settled via the Firm’s appointed custodians.

The Firm selects execution venues, custodians and counterparties based on its assessment of which arrangements are most likely to enable it to obtain the best possible result for clients on a consistent basis.

The Firm considers a range of factors when selecting execution venues, custodians and counterparties, including:

a) Prices available in the market;

b) Depth of liquidity;

c) Speed of execution;

d) Cost of execution;

e) Likelihood of execution and settlement;

f) Market conditions, including volatility;

g) Creditworthiness of counterparties or central counterparties; and

h) Quality and cost of clearing and settlement.

In some markets, price volatility may mean that timeliness of execution is a priority. In other markets with limited liquidity, the ability to execute an order may itself constitute best execution. In certain cases, the Firm’s choice of execution venue may be limited due to the nature of the financial instrument or client requirements.

The Firm maintains and reviews a list of execution venues, custodians and, where applicable, market makers and counterparties it uses. This list is reviewed at least annually, or more frequently where necessary, to ensure that the selected venues continue to provide appropriate outcomes for client orders.

The Firm takes all reasonable steps to identify and manage conflicts of interest in relation to the selection of execution venues, custodians and counterparties.

The Firm does not structure or charge its commissions or fees in a way that would unfairly discriminate between execution venues, nor does it receive any remuneration, discount or non-monetary benefit for routing client orders to a particular venue that would conflict with its duty to obtain best execution.

In certain circumstances, transactions may be executed outside a regulated market, multilateral trading facility (MTF) or organised trading facility (OTF). Where this occurs, the Firm will obtain the client’s prior express consent in accordance with applicable regulatory requirements.

6. Order Handling and Execution Arrangements

6.1 Order Receipt and Transmission

The Firm records all client orders promptly upon receipt, including the time of receipt and relevant order details. Orders are transmitted to custodians or agreed directly with market makers and subsequently booked for settlement, as appropriate, as soon as reasonably practicable.

6.2 Order Prioritisation

The Firm executes comparable client orders sequentially and promptly in the order in which they are received, unless:

- the characteristics of the order or prevailing market conditions make this impracticable; or

- the interests of the client require otherwise.

6.3 Aggregation of Orders

The Firm may aggregate client orders where it reasonably believes that aggregation will not disadvantage any client. Aggregated orders are allocated fairly and in accordance with the Firm’s allocation procedures.

6.4 Allocation of Orders

Where orders are aggregated, the Firm allocates transactions promptly and fairly. Allocation is carried out in a manner that ensures that no client is systematically disadvantaged.

6.5 Timely Execution

The Firm takes all reasonable steps to ensure that client orders are executed promptly and accurately recorded and allocated.

6.6 Limit Orders

Where a client places a limit order in respect of shares admitted to trading on a regulated market which is not immediately executed, the Firm will, where applicable, transmit the order to a custodian or appropriate execution venue for handling in accordance with applicable regulatory requirements, unless the client expressly instructs otherwise.

6.7 Record Keeping

The Firm maintains records of client orders and execution decisions in accordance with applicable regulatory requirements.

7. Monitoring Execution Quality

The Firm periodically reviews the effectiveness of its order execution arrangements and this Policy, including the quality of execution obtained from custodians and market makers or other counterparties, and whether the execution venues and counterparties used continue to provide appropriate outcomes for client orders. Such reviews are carried out on a regular basis.

Where the Firm agrees transactions directly with market makers, it monitors pricing, spreads, responsiveness and execution outcomes to ensure that best execution is achieved.

The Firm monitors execution quality using a range of metrics, which may include:

- price achieved versus market benchmarks

- execution speed

- rates of failed or rejected trades

- settlement performance of intermediaries

Where deficiencies are identified, the Firm will take appropriate remedial action, which may include changing execution venues or intermediaries.

The Firm retains records of its monitoring and review activities in accordance with regulatory requirements.

8. Updating this Policy

The Firm will update this at least annually and whenever a material change occurs that affects the Firm’s ability to obtain the best possible result for clients. Where material changes are made, the Firm will notify clients where appropriate. A material change includes any significant change that affects the Firm’s ability to obtain the best possible result for clients on a consistent basis.

The Firm expects to post the most recent version of this Policy on its website. If a client would like to receive a copy of the most recent Policy, however, please contact the Firm in the manner described in section 10 below.

9. Consenting to this Policy

The Firm obtains client consent to this Policy through the account opening process. Where applicable, the Firm also obtains specific prior express consent to execute orders outside a regulated market, multilateral trading facility (MTF) or organised trading facility (OTF), in accordance with applicable regulatory requirements.

10. Contact Details

If a client has queries about the Policy, they should contact the individual specified below:

Head of Compliance: Mr. Daniel Pellard

Phone: +44 (0) 203 869 6080

Email: enquiries@clear-cm.co.uk

We will reach out for a quick introductory fact find to see how we can best serve your specific needs and arrange a convenient time for a consultation with a member of the appropriate specialist team.

An Advisory Broker will contact you for a deeper fact find and share information on how we can best enhance your portfolio.

We will process your application in accordance with FCA regulations to ensure that your appropriate risk profile is set. You will then have access to an extensive suite of investments, supported by your dedicated Advisory Broker.