Promotion: Capital invested is at risk. Non-Independent Research / Marketing Communication. Attention is drawn to the disclaimers and risk warnings within this document.

BROKER NOTE APPENDIX BY JONATHAN PLANT

30th January 2026

Description and History of Ethereum

Section 1) - What is Ethereum?AP1a

Ethereum is the second-largest cryptocurrency network by market cap, but it’s more than just digital money. It’s a decentralised, open-source blockchain that lets people build and use apps — without needing banks or third parties.

You can think of Ethereum as a global network for digital money and apps. It’s powered by computers (called nodes) around the world, so anyone can build on it and everyone has open, equal access — no permission needed.

2013: Ethereum was proposed by a Canadian, Vitalik Buterin, to expand blockchain use beyond Bitcoin and launched in 2015 with 72 million coins; early financial supporters received most of the initial supply. Ethereum gives developers tools to build and run a variety of applications and layer things like smart contracts onto the blockchain. These apps are called decentralised applications, or dApps. This ushered in a new era of online transactions.

Ethereum, Ether and ETH: what's the difference?

Think of Ethereum like an operating system and ETH as the power source that keeps it running.

Decentralised Governance: Ethereum operates with community consensus, limiting the power of central developers. Ethereum has been built on a platform of transparent transactions from the beginning. There was a central 'body' that created Ethereum and Ether, but they do not hold direct authority over the players who contribute to the global decentralisation of the platform. This means that the collective must agree on new protocols and processes, regardless of what the central bank body believes is best and as we will see it is incentives and good behaviours that dominate progress.

Land of the acronym

DAO – Decentralised Autonomous Organisation; a software running on a blockchain that offers users a built-in model for the collective management of its code. DAOs differ from traditional organizations managed by boards, committees and executives. Rather than being governed by a limited group, DAOs use a set of rules written down in code and enforced by the network of computers running a shared software.

To become a member of a DAO, users need to first join the DAO by buying its cryptocurrency. Holding the asset then generally gives users the power to vote on proposals and updates, proportional to the amount they hold.

Classically, this is what Ethereum represents and ironically it was one such named The Dao, based on Ethereum protocols, that was a Venture Capital token fund which was subject to a hack and had $50 of $70m of tokens stolen. This led to a contentious split in the Ethereum community which has seen a minority remain on the old protocol, proof of work (like BTC is), but with smart contract benefits. Its Ethereum token is ETC – Ethereum Classic, not to be confused with the ETH that we are discussing with regards to Roundhouse.

Protocol changes, also known as hard forks, can be "planned" or "unplanned". A reason for a planned fork may be to adapt the system to manage new needs, introduce security protocols, or streamline the mining/validating process

Hard Forks & Upgrades: Ethereum has undergone several significant hard forks, both planned (e.g., The Merge, Pectra) and unplanned (e.g., DAO hack leading to Ethereum Classic).

ETH 2.0 & Upgrades: Ongoing enhancements like ETH 2.0 and Pectra aim to improve speed, security, and efficiency.

A popular example of an Ethereum protocol change is the Ethereum Pectra upgrade, which took place on 7 May 2025, and is considered one of the most significant Ethereum events when the price was $1835

Changes in Ethereum's protocol keep it running more efficiently and securely. Since the DAO event, there have been seven hard forks:

• Frontier (Genesis): 30 July 2015

• Homestead: 14 March 2016

• DAO Hard Fork (the split into Ethereum and Ethereum Classic): 20 July 2016.

• Byzantium: 25 October 2017.

• The Merge (transition to Proof-of-Stake): 15 September 2022.

• Shapella: 2023.

• Pectra: implemented on May 7, 2025. It combined two updates—the Prague execution layer hard fork and the Electra consensus layer upgrade—to enhance scalability, reduce fees, and improve the user and developer experience. Key changes include increasing the maximum effective balance for stakers, allowing users to pay gas fees with different tokens, and boosting scalability for layer-2 networks by increasing the number of data blobs per blockAP2.

Ethereum 2.0 — from proof of work to proof of stake

Ethereum 2.0, also known as The MergeAP3, was a major upgrade. It switched Ethereum from an older system called proof of work to a new model: proof of stake.

Why did Ethereum need an upgrade?

Proof of work uses huge amounts of electricity. Ethereum needed to become more energy-efficient, scalable, and ready for the future. Switching to proof of stake helped by:

Cutting energy usage by over 99%AP2

Enabling the move toward higher transaction capacity

Laying the foundation for more upgrades

What changed after the merge?

With proof of stake, Ethereum is now secured by people who stake their ETH — instead of by people who solve complex puzzles using lots of electricity.

Validators are randomlyAP4 chosen to confirm transactions and earn rewards. This new system is cheaper, greener and more scalable, as well as more secure since no-one can dominate block validation. It is designed to ensure that validators will see a smoothed achievement of the annual percentage yield APY even if they aren’t immediately selected.

One of the key features of Ethereum is that it allows for both permissioned and permissionless transactions.

• Permissionless transactions allow for any computer on the Ethereum network to confirm the transaction.

• Permissioned transactions are reviewed by only a select group of computers, so all activity does not need to be exposed to all computers as long as it follows the protocols that have been set forth.

How does Ethereum work?AP1a

Ethereum is powered by a decentralised network of computers (called nodes) that maintain a shared database — the blockchain. Every time something happens on Ethereum, every node updates its copy of the ledger to match. Imagine a shared notebook that lives online — everyone can write in it, but no one can erase or change what’s already there. That’s how the Ethereum blockchain works. It’s a global system of computers that all stay in sync, verifying every transaction to keep things secure and transparent.

Blockchain explained

Ethereum’s blockchain is a decentralised database that records every transaction made on the network. Each new transaction is grouped into a 'block' and linked to the one before it, creating a continuous chain of data. Once added, these records can’t be changed or deleted.

This structure means you don’t need a third party to verify a payment or ownership. The blockchain acts as a permanent and transparent source of truth, accessible to anyone.

Because it’s decentralised, no single entity controls the data — making Ethereum both resilient and reliable/trustworthy.

Nodes and the Ethereum Virtual Machine (EVM)

Nodes are individual computers connected to the Ethereum network. They keep full copies of the blockchain and help validate new transactions. This redundancy ensures the network stays operational even if some nodes go offline.

These nodes run the Ethereum Virtual Machine (EVM), a powerful, decentralised computing engine. The EVM is what enables Ethereum to process smart contracts consistently across all nodes, making it possible to run apps securely without a central server.

Smart contracts: these are code-based agreements that automatically execute when their conditions are met. For example:

Automatically sending funds when an event happens (like a crowdfunding goal being met)

In a game, it can ensure you own your digital assets and can trade them securely

These contracts live on the blockchain and are designed to execute as programmed, without relying on a central authority.

Gas fees and transactions

Everything you do on Ethereum, like sending ETH, using apps, or buying NFTs, requires a small transaction fee called a gas fee.

Gas is like fuel. The more complex the action, the more gas it needs. When the network is busy, gas prices go up.

You pay gas in ETH, and part of the fee goes to the validators who help run the network, with the rest being burned to control supply. Gas helps prevent spam and ensures Ethereum runs smoothly.

Ethereum wallets

To interact with the Ethereum network, you’ll need a wallet to store your ETH and other tokens. A wallet has:

A public key: like an address people can send ETH to

A private key: like a password that lets you send or use your ETH

There are two types of wallets:

Custodial wallets (like in the Revolut app): keep your keys secure, so you don’t have to worry about set-up

Non-custodial wallets (like MetaMask): you manage your own keys and take full control of your assets

Ethereum continues to be a fundamental element of the blockchain industry. As businesses continue integrating blockchain solutions, Ethereum's decentralised infrastructure and smart contract capabilities place it at the heart of future digital economies.

The Ethereum community recognised that they needed to address their scalability issues and make the network more flexible, quicker and cheaper on the Layer2 to hold off newer, nimbler competitors. The FusakaAP5 update in Dec25 will address this and build on the Pectra upgrade which it was supposed to be part ofAP6. The Ethereum Fusaka fork (a major upgrade) brings PeerDAS (Peer-to-Peer Data Availability Sampling), making Ethereum nodes verify L2 data by checking small samples instead of full blobs, drastically cutting bandwidth (by ~85%) and storage, boosting scalability for rollups (potentially 8x more data), and lowering L2 fees, all while improving decentralization by making it easier for home stakers to participate, setting the stage for full Danksharding. It's a crucial step towards handling massive L2 transaction volumes, making Ethereum faster and cheaper.

Issues for Ethereum

Sourcenote a16z pdf

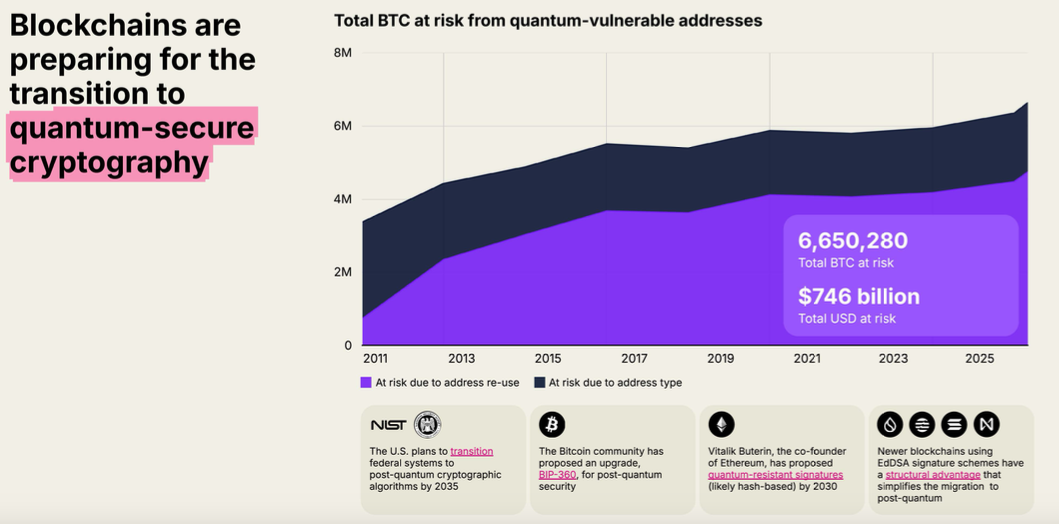

Security remains a key issue for blockchain and crypto in general...AI and Quantum computing require defences against technologies that were not envisaged at inception. In fact, Ethereum cofounder Vitalik Buterin has recently gone on record saying quantum computing is advancing so quickly it could crack “elliptic curve cryptography” (this secures blockchains such as Ethereum and Bitcoin) within three yearAP9, before 2028 and the end of trump’s tenure.

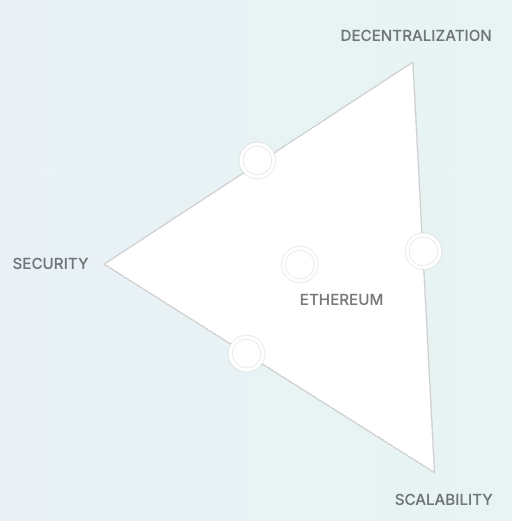

However, it is just part of what is known as The TrilemmaAP1b – can’t have all 3 without compromising 1 of the 3 parts of the triangle below:

Ethereum is now secured via staking, not computing power.

This sustainability boost also brings security benefits - staked ether makes it much more expensive to attack the chain than under proof-of-work, but less expensive to secure it as less new ETH has to be issued to pay validators than miners.

The Trilemma is decentralised and secure means something more rigid with less innovation and reduced scaling. Decentralised and scalable generally has less onerous and tight security, the innovative additions/layers ca be weak points in the system. Scalable security will have a trade-off on control as mass adoption requires more protection. Various rounds of improvements on each leg will see the optimum mix created.

Decentralisation is another issue for ButerinAP8 with his concerns over too much activity focusing around centralised hubs may put off the original users who wanted to escape the system.

To compete with legacy systems of payment processing, blockchain networks must become highly scalable — capable of accommodating an exponentially growing number of users, transactions, and data per second.

Only by adequately incorporating scalability into their structure do blockchain networks stand to supersede other legacy systems. Layer-1 solutions add utility to a native blockchain to optimize its performance like BTC and ETH. Layer-2 solutions are third-party protocols that integrate with an underlying Layer-1 blockchain to increase transactional throughput.

ShardingAP11 is an example of scalability on Layer 1 which breaks the blockchain down into distinct data-sets which can be processed simultaneously rather having all nodes maintain the entire network. The shards provide proofs to the mainchain and interact with each other to maintain consensus. This speeds things up but potentially creates weak points as the Trilemma suggests. Ethereum 2.0 went down this path and is one of the reasons it has maintained popularity. Layer-2ethereum learn attracts the innovation where a lot of the validation work takes place away from the mainchain on Layer1 with that only needed at the end thus allowing faster and cheaper transactions like the OMG Plasma Layer-2 project on top of Layer-1 Ethereum. Scalability with security here but Decentralisation sacrificed which is the cost of growth and mass acceptance.

Roundhouse should be experienced in knowing where to play in this mix of layers and applications; avoiding mistakes the amateur would make.

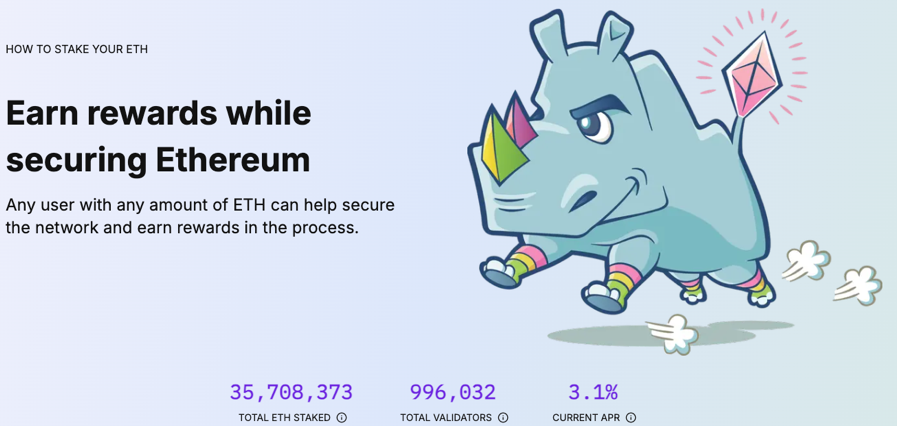

What is staking and how does it work?AP7

The APR of 3.1% in the graphic is what we are looking for...often seen as APY the annual percentage yield. We will explain what staking is and the different ways it can be achieved so that you have a sense of its benefits, risks and understand why it is so crucial to the attractiveness of Ethereum Treasury companies. (NB yields currently 2.8%)

Staking means locking up some of your ETH to help run the Ethereum network and earn rewards in return. It’s one of the key innovations behind Ethereum 2.0 and allows you to participate in maintaining the blockchain. When you stake ETH, you're contributing to transaction validation and the creation of new blocks. In return, you can earn rewards, similar to earning interest — though rewards vary based on network conditions and validator performance.

It’s a bit like earning interest on a savings account — except you’re helping to run a decentralised global network. This is a crucial factor in the benefit of investing in Ethereum Treasury players. Firstly, they will be earning yield here and are professionals at it so risks are low but not zero of losses because bad behaviours can see stakers lose their Ethereum; this acts towards making the network secure and more valuable which should reflect in the ETH value.

There are a number of platforms, ways to access staking but they will have platform-specific fees or commissions. There is a benefit to being able to be totally responsible for your staking but this has logistical requirements that suits being a professional player.

Key factors determining staking yield

Total percentage of tokens staked: Your share of the network's total rewards is proportional to your share of the total amount of tokens staked.

New token issuance: Many networks generate new tokens as staking rewards. If the supply grows faster than demand, the value of your rewards could decrease.

Transaction fees: Transaction fees from network activity contribute to validator rewards, which can be passed on to stakers.

Platform and validator fees: Platforms and validators take a commission on staking rewards, which can lower your effective yield.

Network demand and volatility: The overall demand for the cryptocurrency and its price volatility will affect the real-world value of your rewards.

Staking duration: The amount of time you stake your tokens will affect your total earnings. Some platforms use the annual percentage yield (APY) to show the potential return over a year.

Motivation for staking focuses on earning rewards, gives scale to the network security as higher staking requires more ETH to control a majority of the network; you’d need to control the majority of the validators and their ETH and as you can see from the graphic above that would be a large number. Also, you are part of proof-of-stake networks which requires staking nodes on relatively modest hardware using less energy than the BTC proof of work crypto mining machines require. This itself may allow you to be more comfortable from a green perspective by backing the Ethereum network security solution.

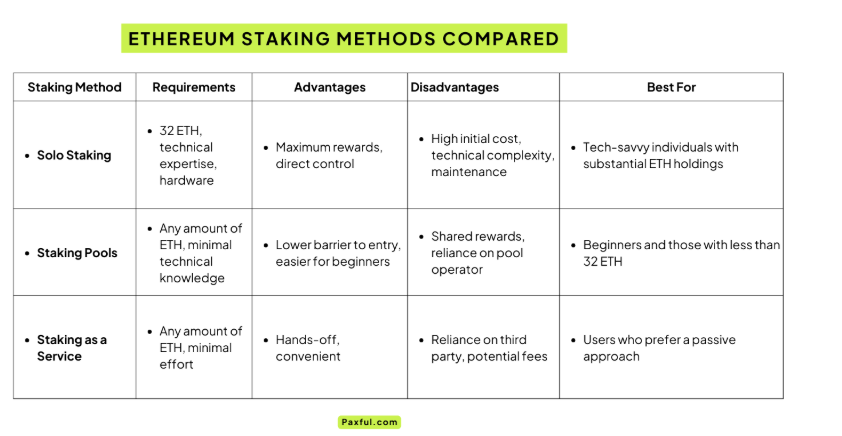

4 main ways of staking:

Home / solo staking

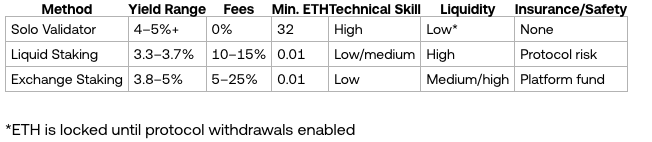

Home staking on Ethereum is the gold standard for staking. It provides full participation rewards, improves the decentralization of the network, and never requires trusting anyone else with your funds.

Home stakers can pool their funds with others, or go solo with at least 32 ETH. Liquid staking token solutions can be used to maintain access to DeFi.

Maximum rewards - receive full rewards directly from the protocol

Rewards for proposing blocks, including unburnt transaction fees, and attesting regularly to the state of the network

Option to mint a liquid staking token against your home node to be used in DeFi

Risks - Your ETH is at stake

There are penalties, which cost ETH, for going offline

Slashing (larger penalties and ejection from the network) for malicious behaviour

Minting a liquid staking token will introduce smart contract risk, but this is entirely optional

Requirements - You must deposit 32 ETH

Maintain hardware that runs both an Ethereum execution client and consensus client while connected to the internet

Staking as a service

Your 32 ETH; Your validator keys; Entrusted node operation

If you don't want or don't feel comfortable dealing with hardware but still want to stake your 32 ETH, staking-as-a-service options allow you to delegate the hard part while you earn native block rewards.

These options usually walk you through creating a set of validator credentials, uploading your signing keys to them, and depositing your 32 ETH. This allows the service to validate on your behalf.

This method of staking requires a certain level of trust in the provider. To limit counter-party risk, the keys to withdrawal your ETH are usually kept in your possession.

Usually involves full protocol rewards minus monthly fee for node operations

Risks - Same risks as solo staking plus counter-party risk of service provider

Use of your signing keys is entrusted to someone else who could behave maliciously

Requirements - Deposit 32 ETH and generate your keys with assistance

Store your keys securely; The rest is taken care of, though specific services will vary

Pooled staking

Stake any amount

Earn rewards; Keep it simple; Popular

Several pooling solutions exist to assist users who do not have or feel comfortable staking 32 ETH.

Many of these options include what is known as 'liquid staking' which involves an ERC-20 liquidity token that represents your staked ETH.

Liquid staking makes staking and unstaking as simple as a token swap and enables the use of staked capital in DeFi. This option also allows users to hold custody of their assets in their own Ethereum wallet and have it available for further activity.

Pooled staking is not native to the Ethereum network. Third parties are building these solutions, and they carry their own risks.

.

Rewards

Pooled stakers accrue rewards differently, depending on which method of pooled staking is chosen

Many pooled staking services offer one or more liquidity tokens that represents your staked ETH plus your share of the validator rewards

Liquidity tokens can be held in your own wallet, used in DeFi and sold if you decide to exit

Risks vary depending on the method used

In general, risks consist of a combination of counter-party, smart contract and execution risk

Lowest ETH requirements, some projects require as little as 0.01 ETH

Deposit directly from your wallet to different pooled staking platforms or simply trade for one of the staking liquidity tokens

Centralized exchangesAP13

Least impactful; Highest trust assumptions

Many centralized exchanges provide staking services if you are not yet comfortable holding ETH in your own wallet. They can be a fallback to allow you to earn some yield on your ETH holdings with minimal oversight or effort.

The trade-off here is that centralized providers consolidate large pools of ETH to run large numbers of validators. This can be dangerous for the network and its users as it creates a large, centralized target and point of failure, making the network more vulnerable to attack or bugs.

Source OKXAP14

Other methods of earning yield with EthereumAP15

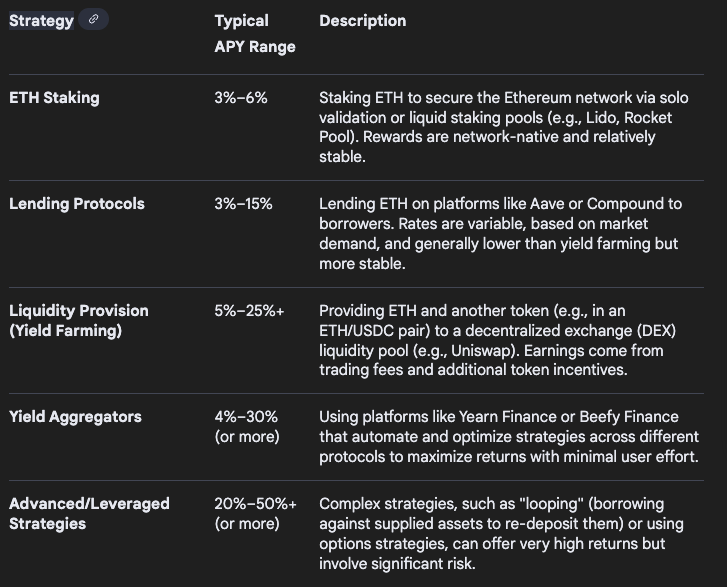

Advanced Yield Strategies & MEV-Boost

Advanced stakers and institutional users utilize more creative methods—like MEV-Boost and multi-chain strategies—to generate extra yield beyond the core APY.

MEV-Boost: By partnering with specialized operators or protocols, validators can extract additional "Maximum Extractable Value" from Ethereum blocks, increasing total staking yield. While complex, some providers (including OKX) incorporate MEV optimization into rewards distribution, automatically adding incremental yield to your payout.

Priority Fees: Some staking pools and exchanges optimize block proposals, claiming extra transaction fees for stakers.

DeFi Yield Layering: With liquid staking tokens like stETH, you can deposit into DeFi protocols (lending, liquidity pools) and stack yield on top of your base staking APY.

Smart contracts aren’t foolproof: DeFi lending runs on smart contracts, which means there’s always a risk of bugs, exploits, or outright hacks.

Lack of regulation: Unlike bank loans, ETH loans are not insured by the government or a central bank. If something goes wrong, lenders could be unable to recover their funds.

Participating in play-to-earn games

Play-to-earn (P2E) games reward players with crypto and NFTs with real-world value.

Axie Infinity – Battle cute creatures (Axies) to earn Smooth Love Potion (SLP), which can be traded for ETH.

The Sandbox – A virtual world where players can build, trade, and monetize digital assets using the SAND token.

There could be entry costs – Some games, like Axie Infinity, require you to buy characters or items upfront.

Earn rewards – Complete quests, battle other players, or create content to earn in-game tokens.

Cash-out – Swap your in-game earnings for ETH or stablecoins on crypto exchanges.

Making real money in these games isn’t instant—you must grind. Leveling up, managing in-game economies, and staying competitive all take time. If you’re just in it for the cash, be prepared for the commitment.

You can lose your gains quickly: The crypto and NFT markets are notoriously volatile. Game popularity, market trends, and outside factors play a role, making it hard to predict long-term value.

Pay to play (before you earn): Some play-to-earn games require an upfront investment, whether buying a character, land, or special items. If the game doesn’t take off, you might have assets worth far less than you paid.

I mention these because of the development background of Roundhouse media, Pioneer and a number of the people in the network. If there is value to be had in this environment, they will be aware of it and be in a place to digitise and monetise it

Developing on Ethereum: The Ethereum blockchain is a platform for building decentralized applications (dApps), non-fungible tokens (NFTs), and smart contracts. If you have technical skills, you can create and monetize these applications or offer consulting services.

Joining a DAO (Decentralized Autonomous Organization)note recap

Pros:

Higher level of security, transparency, and customisability.

Users maintain control over their funds and can tweak settings to maximise profits.

Cons:

Often more complex to use, requiring a higher level of technical expertise.

Typically offer lower interest rates compared to centralised platforms.

Participating in airdrops and community rewards

Trading Ethereum – strategic trading, timing, day to swing trading (longer holds) or Profit Smart with Ethereum Arbitrage BotAP16 arbitrage functions involves recognizing the rapid movements in the crypto market. Suppose Ethereum is trading at $2,500 on Exchange A and $2,550 on Exchange B. A trader can purchase Ethereum on Exchange A while simultaneously selling it on Exchange B. This method ensures that the trader profits from the price gap. The inherent volatility of cryptocurrency markets often results in these fleeting opportunities, prompting traders to act quickly to secure their advantages. A high-speed automated Bot or AI agent increases trading speed, is available 24/7, allows data analysis real-time and efficiently. The good news here is that Pioneer Foundry Ai with KORA AI and Satsuma Technology with AROK AI are all over this space and at the forefront of AI agent development. What might the ETHL AI trading agent be called - ORKA? Designed for ETH whales!!! The base case is for Roundhouse to buy and stake 80% ETH but this is a potential interesting area.

So staking is available and will be a prime source of income for ETHL. As ever the higher the yield the higher the risks and the increased level of competency required. This should be an area where Roundhouse can excel but we will model prudently that they achieve 3.1% base yields for now.

Section 2) DATCOs – Digital Asset Treasury Companies

What is a crypto Treasury and why ETH relative to BTC Treasury

The Ethereum treasury model follows a systematic approach that differentiates it from traditional asset holdings. The aim is to capture a difference in valuations between capital structure and the instruments held in the Treasury, crypto assets and also the potential to earn excess income on those assets. Ethereum represents a unique asset class that combines cryptocurrency characteristics with technological infrastructure exposure. By holding ETH, public companies diversify into a novel asset that has potential for capital appreciation while providing exposure to blockchain technology adoption at the forefront of digital transformation.

Ethereum's smart contract capabilities provide treasury holders access to decentralized finance opportunities beyond simple staking.

Some of the Treasury techniques and issues are discussed belowd1:

1. Capital Raising and Acquisition: Companies raise funds through At-The-Market (ATM) sales or Private Investment in Public Equity (PIPE) deals. ATM involves issuing new shares with regulatory (SEC or FCA for instance) clearance and selling them publicly, while PIPE sells newly issued shares to private investors, often at a discount.

ATMs allow companies to issue shares incrementally at prevailing market prices. When a company trades at a premium to NAV, each dollar raised via an ATM buys more crypto per share than it dilutes. ATMs are typically the preferred capital formation vehicle among DATCOs because they scale easily and avoid steep discounts or large issuance events.

PIPEs are negotiated capital raises where large investors purchase newly issued stock at agreed-upon prices, often in illiquid or low-float stocks. While PIPEs allow for rapid capital formation, they typically involve significant dilution and introduce short-term price risks when large supply suddenly hits the market.

2. ETH Acquisition Process: Companies acquire ETH through over-the-counter (OTC) purchases or direct market purchases via partnerships with institutional-grade crypto exchanges. This approach minimizes market impact and ensures better execution for large orders. Improved Treasury logistics can be seen from the recent SATS CLN and efficienciesnotemx SATS through players settling 2/3rds of the transaction in crypto and settling within one hour and 99.99% accurate according to Matt Lodge. Compare this with the fiat portion which took days to settle with large fees and errors. The settling in crypto mitigates future execution risks for the Treasury strategy too.

3. Staking Strategy Selection: Companies choose between different staking approaches, discussed previously, based on their liquidity needs and risk tolerance:

Native Staking: Running validators directly requires 32 ETH per validator and technical infrastructure but offers maximum rewards and control.

Liquid Staking: Using protocols like Liquid Collective or Lido allows companies to stake any amount while receiving liquid tokens (like stETH or LsETH) that can be traded or used in DeFi applications.

Institutional Staking Services: Platforms like Figment provide enterprise-grade staking infrastructure with slashing protection and compliance features but lower yields

4. Yield Generation and Management: Ethereum staking currently offers around 3% annual percentage yield (APY). Liquid staking solutions solve the traditional problem of locked assets by providing tradeable tokens representing staked ETH, enabling companies to maintain liquidity while earning staking rewards. This dual benefit allows treasury managers to generate yield without sacrificing operational flexibility.

5. Liquidity Management: Liquid staking tokens can be instantly traded on decentralized exchanges, re-staked to help secure other networks for additional yield, or used as collateral in DeFi protocols, providing companies with multiple exit strategies. Traditional staking requires a 7-day withdrawal period, but liquid staking eliminates this constraint while still capturing full staking rewards.

6. Revenue Optimization: Staking rewards create a passive income stream that companies can either reinvest to acquire more ETH or use for operational expenses, creating a compounding effect on their treasury holdings. Some companies deploy liquid staking tokens in additional yield-generating strategies, potentially increasing total returns beyond base staking yields.

Passive Income Through Staking Rewards

Real-world results demonstrate the power of ETH staking for corporate treasuries. SharpLink Gaming earned 1,326 ETH through staking since launching its treasury on June 2, 2025—representing over $6 million in passive earnings in just two months.

Current ETH staking yields range around 3% APY, providing predictable cash flow that traditional treasury assets cannot match. With approximately 28% of all ETH now staked, this represents a massive institutional shift toward productive asset management.

Risks Facing Ethereum Treasuriesd1

While Ethereum treasuries offer several financial and technological advantages, they also pose risks and challenges, including:

Slashing and Smart Contract Risks

Ethereum's Proof of Stake mechanism includes penalties called "slashing" for validator misbehaviour. When validators experience extended downtime or commit protocol violations (double voting, proposing conflicting blocks), up to 10% of staked ETH can be permanently lost. We will discuss this further in the market pricing section.

Smart contract interactions amplify risk exposure. Companies using liquid staking protocols, re-staking platforms like EigenLayer, or DeFi yield strategies face additional technical vulnerabilities. Smart contract bugs, oracle manipulations, or protocol exploits could result in partial or total loss of deployed capital.

Liquidity Management Challenges

Native ETH staking creates liquidity constraints through required withdrawal periods. Traditional staking locks assets for up to 7 days during unstaking, potentially creating cash flow challenges during market stress.

Liquid staking solutions like Lido and Liquid Collective address this through tokenized representations (stETH, LsETH) that can be traded freely while earning staking rewards. However, these tokens may trade at slight discounts during market volatility, and the underlying protocols add smart contract risk layers.

Large treasury positions face additional constraints: the current stETH liquidity of approximately $274 million across DEXs may be insufficient for multi-billion dollar treasury exits during times of market stress.

Market Volatility and Regulatory Uncertainty

Ethereum's price volatility exceeds traditional treasury assets like gold and shares, creating balance sheet uncertainty. Mark-to-market accounting requirementsd2 which values assets based on their current market price rather than historical cost, mean ETH holdings directly impact quarterly earnings through unrealized gains and losses.

Currently there are no explicit restrictions on a UK Treasury Company and its crypto holdings but Roundhouse is registered in Singapore and listed in the UK. This should see them lightly regulated on holdings but subject to FCA listing requirements especially if looking to progress from Aquis to the main list. This would involve Corporate Governance Codes and clear investment policies on the purpose of crypto investment, allocations and risk management policiesR14. More on this in Regulation section. ETHL has the intention of being 75/25 split crypto to fiat on Treasury assets and 80% staked within the ETH element.

What's the difference between ETH and Bitcoin treasury strategies?

Ethereum treasuries can generate organic yield through staking, while Bitcoin treasuries rely solely on price appreciation. ETH is considered a "productive asset" versus Bitcoin's "store of value" classification.

Bitcoin Yield: Bitcoin Yield is a key performance indicator that tracks how efficiently a bitcoin treasury company grows BTC per diluted share over time. It reflects the firm’s capital efficiency, or how well it can raise funds and convert them into BTC without heavily diluting shareholders. Higher BTC Yield is correlated with higher equity premiums ad the same applies to ETH.

What are the main risks of ETH treasury strategies?

Key risks include market volatility, smart contract vulnerabilities, slashing penalties, liquidity constraints, and potential regulatory classification issues under the Investment Company Act in the US.

The fundamental difference lies in Ethereum's ability to generate organic yield. While Bitcoin treasury pioneer Strategy's approach focuses on buy-and-hold value appreciation, Ethereum treasuries can earn consistent returns through protocol participation, making ETH a productive asset versus Bitcoin's store-of-value proposition.

The GENIUS Act's regulatory clarity for stablecoins particularly benefits Ethereum treasuries. Since most stablecoins operate on Ethereum, increased stablecoin adoption drives transaction fees to the network, directly benefiting ETH holders through increased network value and potential fee burning mechanisms which stabilise inflationary supply issues.

Ethereum treasuries represent a paradigm shift from passive to productive treasury management. While Bitcoin treasuries offer inflation hedging, Ethereum strategies provide both hedge capabilities and yield generation through staking rewards. This fundamental difference explains why institutional wallets are creating unprecedented capital flow between traditional finance and cryptocurrency markets.

As Standard Chartered predicts that treasury companies could eventually own 10% of all Ethereumd3.

Understanding Ethereum treasury fundamentals becomes crucial for investors evaluating companies pursuing this strategy, as it represents a new category of corporate financial management that could reshape how institutions approach treasury operations in the digital age. The following segment considers some of the developments in the crypto Treasury space.

DATCOs YT interviewd4 with Jeff Park and my interpretation parsing below:

This is generally an ecosystem of liquidity and leverage between the Nav (net asset values of the crypto assets) vs the market cap of the DATCo.

MSTR – Strategy run by Michael Saylor – is seen as best in class but even they had to pay interest on early Convertible raises. Now they utilise a number of avenues to market:

At-the-market ATMs where the company has advanced permission to issue shares and employs an agent to take advantage of liquidity and price when it is above NAV. Olivia Edwards at ASTR/CEL AI and ETHL shareholder, currently has this in placem2 with the express request to sell up to 575m shares patiently and deal when the conditions are in favour. So, the strategy is familiar to the Roundhouse group. This avoids costly set-up fees and delays in being able to transact when the ratios are hot.

Convertible Loan notes such as the strategic holding SATS have done which can be interest free and/or low strikes to encourage cheap financing or as MSTR have mastered interest free Zero Coupon Bonds for their CLNs with laddered strike prices for equity conversions which guarantees a positive mNAV and a self-fulfilling flywheel in a bull market for Bitcoin. So far MSTR has avoided being forced to have to put covenants on the CLNs forcing him to liquidate BTC in a downturn but for now the market is still growing and DATCOs are still a minority of the pie.

Also Preferred shares. MSTR has a whole stack of different instruments at their disposal but these are interesting. These are not much better than common shares but they aren’t credit either. Historically they have been used as a buffer financing when large companies have tapped out their normal credit lines...airlines often use it when they need extra capex for new planes. Normally retired once their usefulness is used up. These come with a coupon and some question whether this would be the instrument that suffers in a bear market. Failing to pay on a preferred stock would not be ideal but it won’t affect the debt instruments which retain a higher claim and ironically would probably save the common stock (not paying the coupon saves cash) but isn’t something you really want to see happen when trying to gain mainstream confidence in the model.

Institutional credibility for the model has been strong from insurance companies, hedge funds and legitimate investing institutions looking to diversify into DATCOs and benefit from the diversification of clever managements that can sweat the crypto set up. This is particularly relevant for ETHereum Treasuries as there is a natural infrastructure as we explained above for creating substantial yields. Debt to equity levels of about 8-10% are ideal but will come with potential dilution concerns early in the journey.

Convertibles are really an arbitrage on mis-priced volatility so tended to compete with debt yields but here we have asset backed volatility. The CLN market makers want the cycle of accretive dilution but at strikes that will encourage conversion. If they are long gamma hedging they will be buyers of stock as it dilutes the share price. As long as there aren’t too many CLNs relatively then volatility will remain high enough to keep the cycle turning.

Crypto investing has changed In the late 2010s there was a blindspot where sceptics couldn’t see the cashflow. Bitcoin is not productive, doesn’t yield, nothing more than a belief system they said. With a DATCO the product is the balance sheet strategy. Competition will be determined by innovation and product placement within the blockchain. What you want is a management team that has an operating company within the digital and crytpo asset ecosystem that also knows how to sweat the yield. The competition from ETFs is limited really because they have retail constraints particularly with the threat of redemptions. A DATCO that is really like a Permanent Capital Vehicle will own assets and can do things that a regulated ETF probably can’t in terms of staking and defi. By doing things that benefit the network will maximise yields too. Look to invest in an operating company with edge in the crypto game. Perpetually producing up to a 6% yield on a growing asset base is a valuable thing. DATCOs become like an asset manager.

Ironically volatility remains cryptos friend.

Investment Banks see growth in the Investment Bank machine...the more volatility there is you then see the options market and leveraged products arrive for hedging or speculation. Ultimately that needs a borrowing and lending market too. Multi-million issues attract large fees. High volatility, high volume stocks are the order of the day. Whoever would have thought we would have heard Jamie Dimon of JPM pushing both gold and crypto given his hatred over the years.

This is a global game. The US is leading followed by the UAE and Asia because these regions have adopted regulations quicker. The UK needs to catch up and there a few DATCOs but you want to concentrate on those that can layer instruments and partners within the ecosystem. There are some different strategies around. Take METAPLANET in Japan which cannot issue ATMs so they have innovation in their CLN strikes. For US investors there is the YEN carry trade incentive to back the METAPLANET game and its association with risk on markets. Cheap credit markets that even MSTR probably can’t access.

For the retail clients it is spotting when they are the one holding the ball. We seem to be in an era where the long-term crypto HODLs are selling or looking to sell into a market which has historically collapsed in the face of large token offerings. Insider transactions and liquidity events can often see low volume price swings just because the big players are prevented from trading. What is happening is blocks of crypto being exchanged for stock or CLNs to avoid the crypto selling volatility and exposure to amore mature exit system in the Trad-fi environment and feed the retail demand for DATCO. This dynamic in itself should support returns for the DATCOs short term.

Lean into the utility of ETH and find a pro like ETHL that has the time to generate yield and crucially not lose it. Defi specialists. ETH looks like Digital Oil rather than Digital BTC/Gold...there is a need to use it rather than sit looking at the barrels. There is a cost of carry to cover.

Much is made of the Doom Loop if crypto falls and MNAV spirals below 1. This is where the DATCO should be nimble in options markets to hedge. If there is a PIPE expiring which may be about to flood the market with stock the Treasury needs to be smart and either consider a buyback or sale of crypto particularly if the ROE on the operating Co > ETH yield...again you need to judge who you are investing with...will they have the tools?

It won’t take much to see the whole mNAV arbitrage suddenly breakout again...a sudden stabilisation in ETH and BTC and there will be a large rush to fund crypto purchase

Slashing: The Power of Deterrencemf2

The data is clear: slashing in proof-of-stake systems is remarkably rare, affecting a tiny fraction of validators and an even smaller percentage of staked assets. When it does occur, it's almost always due to technical errors rather than attacks.

In traditional systems, addressing such cases often requires reactive governance proposals or manual rollbacks — a time-consuming and contentious process. Symbiotic’s design introduces a more structured alternative: features like Resolvers and Veto Slashing allow for slashing events triggered by technical errors to be intercepted and reviewed before they take effect on-chain, enabling faster and more reliable remediation without compromising the deterrent effect. This is precisely how deterrence should work. The mere possibility of significant financial loss effectively prevents malicious behaviour, while the actual frequency of punishment remains low. By making attacks economically irrational, slashing ensures that rational participants will always choose to follow the rules.

Immediate Penalty: A portion of the validator's staked ETH (an immediate initial penalty of around 1 ETH for an isolated incident) is automatically deducted from their balance and destroyed by the protocol. This removes the supply from circulation.

Whistleblower Reward: A small amount of ETH (around 0.0625 ETH) from the initial penalty goes to the "whistleblower" – the other honest validator who first reported the slashable offense. The remainder is burned.

Correlation Penalty: An additional penalty is applied depending on the number of other validators slashed around the same time. This is designed to make coordinated attacks prohibitively expensive. The more validators involved in correlated misbehaviour, the greater the burn and the total loss for each offender, which can amount to their entire 32 ETH stake in extreme cases.

Forced Exit: The slashed validator is also immediately and permanently removed from the active validator set and cannot participate in further validation or earn rewards.

In essence, the slashed ETH is not redistributed to the remaining honest validators (except for the small whistleblower reward) or sent to a treasury; it is removed from the total supply of Ethereum, increasing the scarcity of the remaining ETH for all network participants.

Slashing is Rare

Despite the fear it generates, slashing remains exceedingly rare in practice:

Ethereum: Only about 0.04% of validators have ever been slashed - 472 out of more than 1,200,000 validators

Cosmos Hub: In its entire history since 2019, there have been only 5 slashing events for double-signing (a severe offense), underscoring just how rare such incidents are.

Polkadot: Outside of one notable mass-slashing incident in its early days, Polkadot's slashing rate has been minimal

Even more revealing is how often blocks contain slashing events:

On Ethereum, approximately 0.0033% of blocks include a slashing - roughly 1 in 30,000 blocks

For Cosmos Hub and Polkadot, this figure is even lower, with slashing events appearing in less than 0.002% of the blocks

In financial terms, the impact is similarly minuscule. Across major PoS networks, the total percentage of stake ever slashed is well below 0.05% of all staked assets. For Ethereum specifically, it's around 0.001%.

Technical Issues, Not Attacks

What's particularly revealing is that virtually all slashing events result from technical errors rather than malicious attempts to attack networks. The most common causes include:

Redundancy misconfigurations and key misuse: Running backup nodes without proper safeguards or reusing validator keys across machines, both of which can lead to accidental double-signing

Client software bugs: Issues in validator clients causing inadvertent rule violations

Infrastructure outages: Correlated failures during cloud provider downtimes

Ethereum's Approach

Ethereum uses a correlation-aware slashing mechanism. An isolated mistake might cost a validator around 1 ETH (about 3-4% of their 32 ETH stake), but if many validators misbehave simultaneously, each loses a larger percentage. This design assumes correlated failures are more likely to be attacks than isolated ones.

Slashed ETH is permanently burned, and the slashing action cannot be reversed by governance - it's entirely algorithmic and automatic.

https://www.bitget.com/news/detail/12560605102260

Proof of Stake Paradox

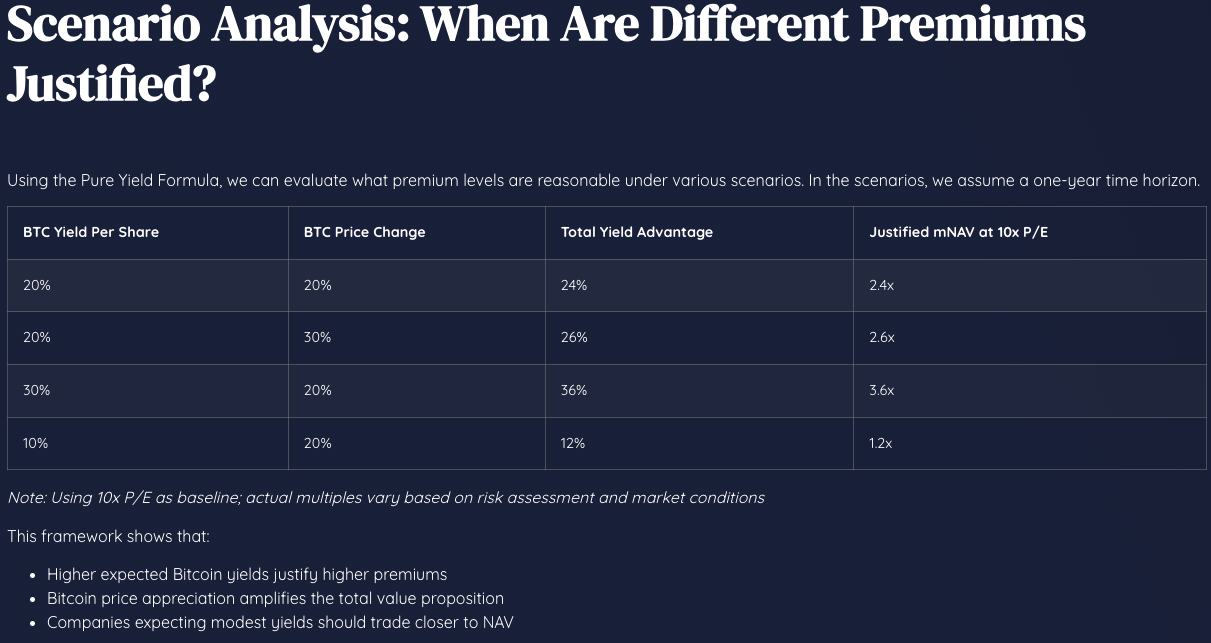

Why Premiums Exist: The Forward-Looking Value Proposition

Premiums exist because investors expect growth in crypto per share, similar to equity investors valuing future cash flows.

The Pure Yield Formula

ETH Yield (%)=(ETH per UnitEndETH per UnitStart-1)×100%

Each successful accretive raise boosts the ETHer per share (ETH/share) metric, often termed Ethereum yield.

The total value proposition combines two elementsv1:

Companies that can sustainably deliver Bitcoin yields above the total return from direct Bitcoin ownership will likely continue to show positive mNAV values. Those that cannot will see their valuations converge toward NAV, or below it if their execution consistently disappoints and the leading Treasury companies may acquire them.

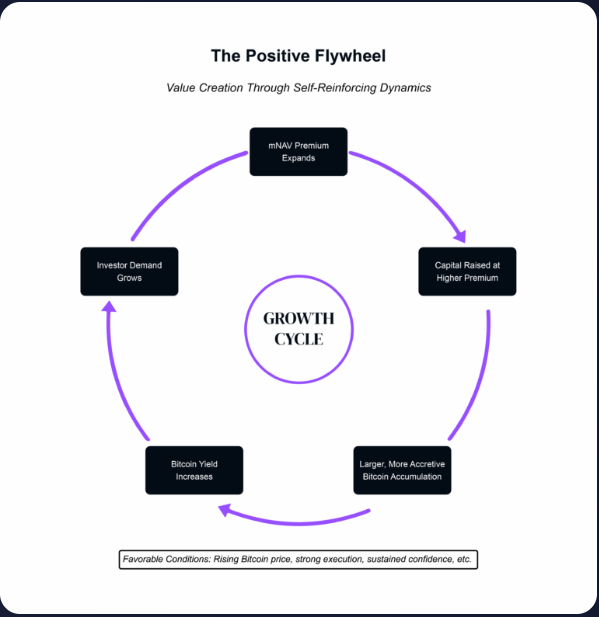

If a company trading at 2× mNAV raises $100 million, it adds $100 million in Bitcoin to the treasury while diluting shareholders by only $50 million in underlying value. The result is an increase in Bitcoin per share—the foundation of the flywheel.

This mechanism depends entirely on market confidence and premium preservation. Once the company trades at or below NAV, accretive issuance becomes impossible, halting the flywheel’s rotation.

3. Attracting New Investors

Strong Bitcoin yield and consistent performance tend to attract diverse investor classes:

Regulated Institutions seeking Bitcoin exposure without direct custody risk.

Retail Investors desiring amplified Bitcoin exposure through equity.

Funds Restricted by Mandate from holding Bitcoin directly.

However, the flywheel’s acceleration depends on actually attracting this broad investor base.

The result: more demand → higher premiums → stronger flywheel acceleration as institutional credibility increases..

Rising investor demand tends to drive higher mNAV premiums. These premiums serve as a real-time indicator of market confidence in the management’s ability to execute.

Higher premiums can reinforce future accretive raises—creating a self-fulfilling growth signal.

A company at 3× mNAV can issue new equity far more efficiently than one at 1.2×, making premium management an active strategic objective, not just a market by-product.

In theory, the flywheel’s power lies in its compounding nature—each successful capital raise improves metrics that can make the next raise easier and more profitable. But the devil is usually in the details.

As companies scale, diminishing returns tend to emerge:

A small company with $10 million in Bitcoin may raise another $5 million (+50%) relatively easily.

A large company with $10 billion must raise $5 billion for the same relative impact at the same mNAV—an order-of-magnitude challenge.

At higher scales, market absorption capacity, regulatory friction, and investor fatigue can slow the rotation speed. The flywheel does not stop—it simply slows under the weight of its own success.

But this same power creates proportional risks when conditions reverse.

Companies that manage flywheel dynamics well—balancing momentum during good phases with preparation for reversals—are better able to sustain long-term competitive advantage. Those chasing unsustainable growth or neglecting risk may struggle to navigate full cycles, especially downturns.

Companies should plan early particularly if mNAV is at a premium. Strong policy ideas below:

• announce plans to pause ATM issuance at mNAV <1 for a defined period say 1-2 weeks

• reverse the dynamic if crypto rises but stock falls...announce a buyback etc

• launch a strategic review if a NAV discount persists; look for mergers, spinoffs or change crypto strategy

• make sure compensation reflects NAV per share growth not the absolute crypto position or total share count. This is a Note ASTR ATM only when above NAV

Appendix (Apx)

Ethereum Notes

Section 1)

Note AP1a https://ethereum.org/what-is-ethereum/

Ethereum.org what is ethereum

Note AP1b https://www.theblock.co/learn/249536/what-is-the-blockchain-trilemma

theblock.co learn what is the blockchain trilemma Sep 19th 2023

Note AP2 https://consensys.io/ethereum-pectra-upgrade

consensys.io Ethereum pectra upgrade

Note AP3 https://ethereum.org/roadmap/merge/

Ethereum.org roadmap merge

Note AP4 https://consensys.io/blog/your-guide-to-ethereum-validator-staking-rewards

consensys.io blog your guide to Ethereum validator staking rewards

Note AP5 https://www.coingecko.com/learn/what-is-ethereum-fusaka-upgrade

Coingecko.com learn what is ethereum fusaka upgrade

Note AP6 https://cointelegraph.com/news/ethereum-fusaka-fork-final-testnet-debut-before-mainnet

Cointelegraph.com news ethereum fusaka fork final testnet debut before mainnet Oct 29th 2025

Note AP7 https://ethereum.org/staking/ Ethereum.org staking (has live APY%)

Note AP8 VB founder worries over Blackrock Vitalik Buterin "If institutions like BlackRock gain influence, Ethereum could go in the wrong direction" https://bloomingbit.io/en/feed/news/101065

bloomingbit.io news 101065 (or the quoted title above)

Note AP9 https://en.cryptonomist.ch/2025/11/19/ethereum-quantum-deadline-2028/

En.cryptonomist.ch ethereum quantum deadline 2028 Nov 19th 2025

Note AP10 https://finance.yahoo.com/news/scam-alert-defi-protocol-balancer-114506495.html balancer hack Nov 25 finance.yahoo.com news scam alert defi protocol Balancer hack Nov 25

Note AP11 https://www.gemini.com/en-GB/cryptopedia/blockchain-layer-2-network-layer-1-network

gemini.com cryptopedia blockchain layer 2 network layer 1 network

Note AP12 https://ethereum.org/layer-2/learn/

Ethereum.org layer-2 learn

Note AP13 https://recap.io/blog/how-to-make-money-with-ethereum

recap.io blog how to make money with ethereum

Note AP14 https://www.okx.com/en-gb/learn/ethereum-staking-apy

okx.com learn Ethereum staking apy

Note AP15 https://omni.app/learn/how-to-make-money-with-ethereum

Omni.app learn how to make money with ethereum

Sirjohna2015.ca crypto mev bot and Ethereum arbitrage

Section 2)

Note AP17 https://melanion.digital/bitcoin-treasury-flywheel-value-creation/

Melanion.digital bitcoin treasury flywheel value creation

Note AP18 https://melanion.digital/corporate-bitcoin-strategy-guide/

melanion.digital corporate bitcoin strategy guide

We will reach out for a quick introductory fact find to see how we can best serve your specific needs and arrange a convenient time for a consultation with a member of the appropriate specialist team.

An Advisory Broker will contact you for a deeper fact find and share information on how we can best enhance your portfolio.

We will process your application in accordance with FCA regulations to ensure that your appropriate risk profile is set. You will then have access to an extensive suite of investments, supported by your dedicated Advisory Broker.